Advertisement

Gemac Engineering Machinery Co., Ltd. (SZSE:301048) Shares Fly 51% But Investors Aren't Buying For Growth

Gemac Engineering Machinery Co., Ltd. (SZSE:301048) shareholders would be excited to see that the share price has had a great month, posting a 51% gain and recovering from prior weakness. But the gains over the last month weren't enough to make shareholders whole, as the share price is still down 2.9% in the last twelve months.

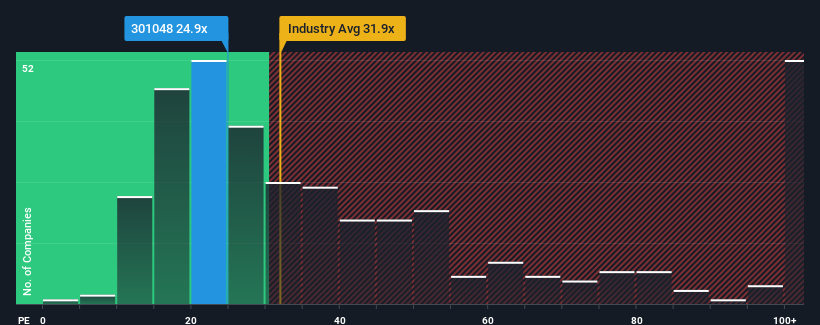

Although its price has surged higher, Gemac Engineering Machinery may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 24.9x, since almost half of all companies in China have P/E ratios greater than 34x and even P/E's higher than 64x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

As an illustration, earnings have deteriorated at Gemac Engineering Machinery over the last year, which is not ideal at all. One possibility is that the P/E is low because investors think the company won't do enough to avoid underperforming the broader market in the near future. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Gemac Engineering Machinery

What Are Growth Metrics Telling Us About The Low P/E?

Gemac Engineering Machinery's P/E ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the market.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 22%. The last three years don't look nice either as the company has shrunk EPS by 16% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Comparing that to the market, which is predicted to deliver 37% growth in the next 12 months, the company's downward momentum based on recent medium-term earnings results is a sobering picture.

In light of this, it's understandable that Gemac Engineering Machinery's P/E would sit below the majority of other companies. Nonetheless, there's no guarantee the P/E has reached a floor yet with earnings going in reverse. Even just maintaining these prices could be difficult to achieve as recent earnings trends are already weighing down the shares.

The Key Takeaway

Despite Gemac Engineering Machinery's shares building up a head of steam, its P/E still lags most other companies. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Gemac Engineering Machinery revealed its shrinking earnings over the medium-term are contributing to its low P/E, given the market is set to grow. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

You always need to take note of risks, for example - Gemac Engineering Machinery has 1 warning sign we think you should be aware of.

If you're unsure about the strength of Gemac Engineering Machinery's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:301048

Gemac Engineering Machinery

Engages in the research, development, production, sale, and maintenance of rail engineering equipment in China.

Flawless balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor