Investors Still Aren't Entirely Convinced By CIMC Vehicles (Group) Co., Ltd.'s (SZSE:301039) Earnings Despite 27% Price Jump

CIMC Vehicles (Group) Co., Ltd. (SZSE:301039) shareholders have had their patience rewarded with a 27% share price jump in the last month. The bad news is that even after the stocks recovery in the last 30 days, shareholders are still underwater by about 7.9% over the last year.

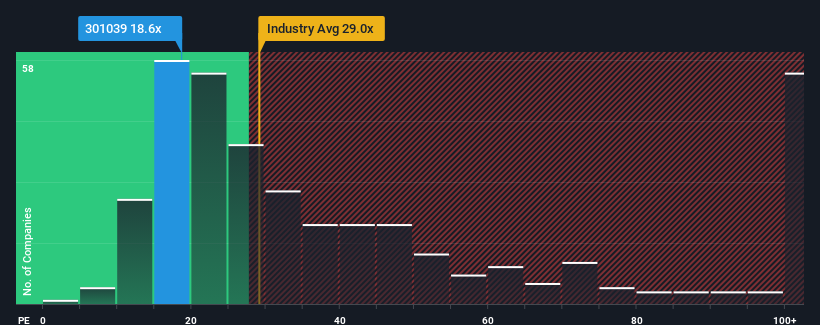

Although its price has surged higher, CIMC Vehicles (Group)'s price-to-earnings (or "P/E") ratio of 18.6x might still make it look like a buy right now compared to the market in China, where around half of the companies have P/E ratios above 30x and even P/E's above 58x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

CIMC Vehicles (Group) has been struggling lately as its earnings have declined faster than most other companies. It seems that many are expecting the dismal earnings performance to persist, which has repressed the P/E. You'd much rather the company wasn't bleeding earnings if you still believe in the business. If not, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Check out our latest analysis for CIMC Vehicles (Group)

How Is CIMC Vehicles (Group)'s Growth Trending?

There's an inherent assumption that a company should underperform the market for P/E ratios like CIMC Vehicles (Group)'s to be considered reasonable.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 57%. This means it has also seen a slide in earnings over the longer-term as EPS is down 11% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Turning to the outlook, the next three years should generate growth of 22% each year as estimated by the five analysts watching the company. With the market only predicted to deliver 19% each year, the company is positioned for a stronger earnings result.

With this information, we find it odd that CIMC Vehicles (Group) is trading at a P/E lower than the market. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

What We Can Learn From CIMC Vehicles (Group)'s P/E?

CIMC Vehicles (Group)'s stock might have been given a solid boost, but its P/E certainly hasn't reached any great heights. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of CIMC Vehicles (Group)'s analyst forecasts revealed that its superior earnings outlook isn't contributing to its P/E anywhere near as much as we would have predicted. There could be some major unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. At least price risks look to be very low, but investors seem to think future earnings could see a lot of volatility.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with CIMC Vehicles (Group), and understanding these should be part of your investment process.

You might be able to find a better investment than CIMC Vehicles (Group). If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

If you're looking to trade CIMC Vehicles (Group), open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:301039

CIMC Vehicles (Group)

Designs, develops, produces, and sells specialty vehicles, semi-trailers, spare parts, and related technical services in China.

Very undervalued with flawless balance sheet.

Similar Companies

Market Insights

Community Narratives