Changchun Zhiyuan New Energy Equipment Co., Ltd's (SZSE:300985) Shares Lagging The Industry But So Is The Business

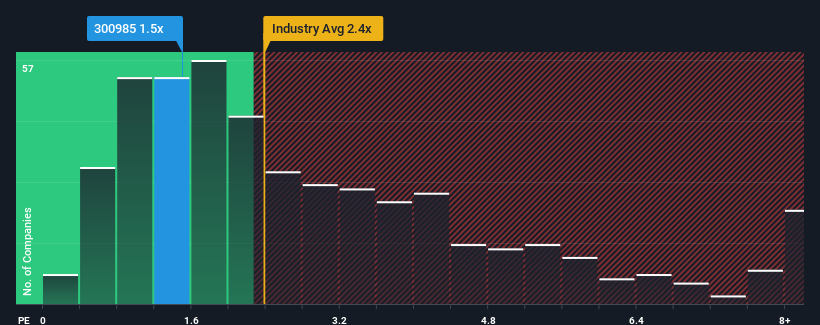

With a price-to-sales (or "P/S") ratio of 1.5x Changchun Zhiyuan New Energy Equipment Co., Ltd (SZSE:300985) may be sending bullish signals at the moment, given that almost half of all the Machinery companies in China have P/S ratios greater than 2.4x and even P/S higher than 5x are not unusual. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for Changchun Zhiyuan New Energy Equipment

How Has Changchun Zhiyuan New Energy Equipment Performed Recently?

With revenue growth that's exceedingly strong of late, Changchun Zhiyuan New Energy Equipment has been doing very well. One possibility is that the P/S ratio is low because investors think this strong revenue growth might actually underperform the broader industry in the near future. If that doesn't eventuate, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Changchun Zhiyuan New Energy Equipment's earnings, revenue and cash flow.How Is Changchun Zhiyuan New Energy Equipment's Revenue Growth Trending?

Changchun Zhiyuan New Energy Equipment's P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

If we review the last year of revenue growth, we see the company's revenues grew exponentially. Pleasingly, revenue has also lifted 54% in aggregate from three years ago, thanks to the last 12 months of explosive growth. So we can start by confirming that the company has done a great job of growing revenue over that time.

Comparing the recent medium-term revenue trends against the industry's one-year growth forecast of 24% shows it's noticeably less attractive.

With this in consideration, it's easy to understand why Changchun Zhiyuan New Energy Equipment's P/S falls short of the mark set by its industry peers. Apparently many shareholders weren't comfortable holding on to something they believe will continue to trail the wider industry.

The Bottom Line On Changchun Zhiyuan New Energy Equipment's P/S

Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our examination of Changchun Zhiyuan New Energy Equipment confirms that the company's revenue trends over the past three-year years are a key factor in its low price-to-sales ratio, as we suspected, given they fall short of current industry expectations. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

You need to take note of risks, for example - Changchun Zhiyuan New Energy Equipment has 2 warning signs (and 1 which is potentially serious) we think you should know about.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

If you're looking to trade Changchun Zhiyuan New Energy Equipment, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300985

Changchun Zhiyuan New Energy Equipment

Research and development, production, and sale of vehicle-mounted liquefied natural gas (LNG) gas supply systems and marine LNG fuel gas supply systems in China and internationally.

Adequate balance sheet slight.

Market Insights

Community Narratives