As December 2024 unfolds, global markets are navigating a landscape marked by interest rate adjustments and mixed performances across major indices. While large-cap stocks have shown resilience, small-cap stocks have faced challenges, as evidenced by the Russell 2000's recent underperformance compared to the S&P 500. In this environment, discovering hidden opportunities requires identifying stocks with strong fundamentals and growth potential that can withstand broader market pressures.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Sugar Terminals | NA | 3.14% | 3.53% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Citra Tubindo | NA | 11.06% | 31.01% | ★★★★★★ |

| Prima Andalan Mandiri | 0.94% | 20.24% | 15.28% | ★★★★★★ |

| Cardig Aero Services | NA | 6.60% | 69.79% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| CTCI Advanced Systems | 30.56% | 24.10% | 29.97% | ★★★★★☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Chongqing Machinery & Electric | 27.77% | 8.82% | 11.12% | ★★★★☆☆ |

| Bank MNC Internasional | 18.72% | 4.80% | 43.63% | ★★★★☆☆ |

Let's review some notable picks from our screened stocks.

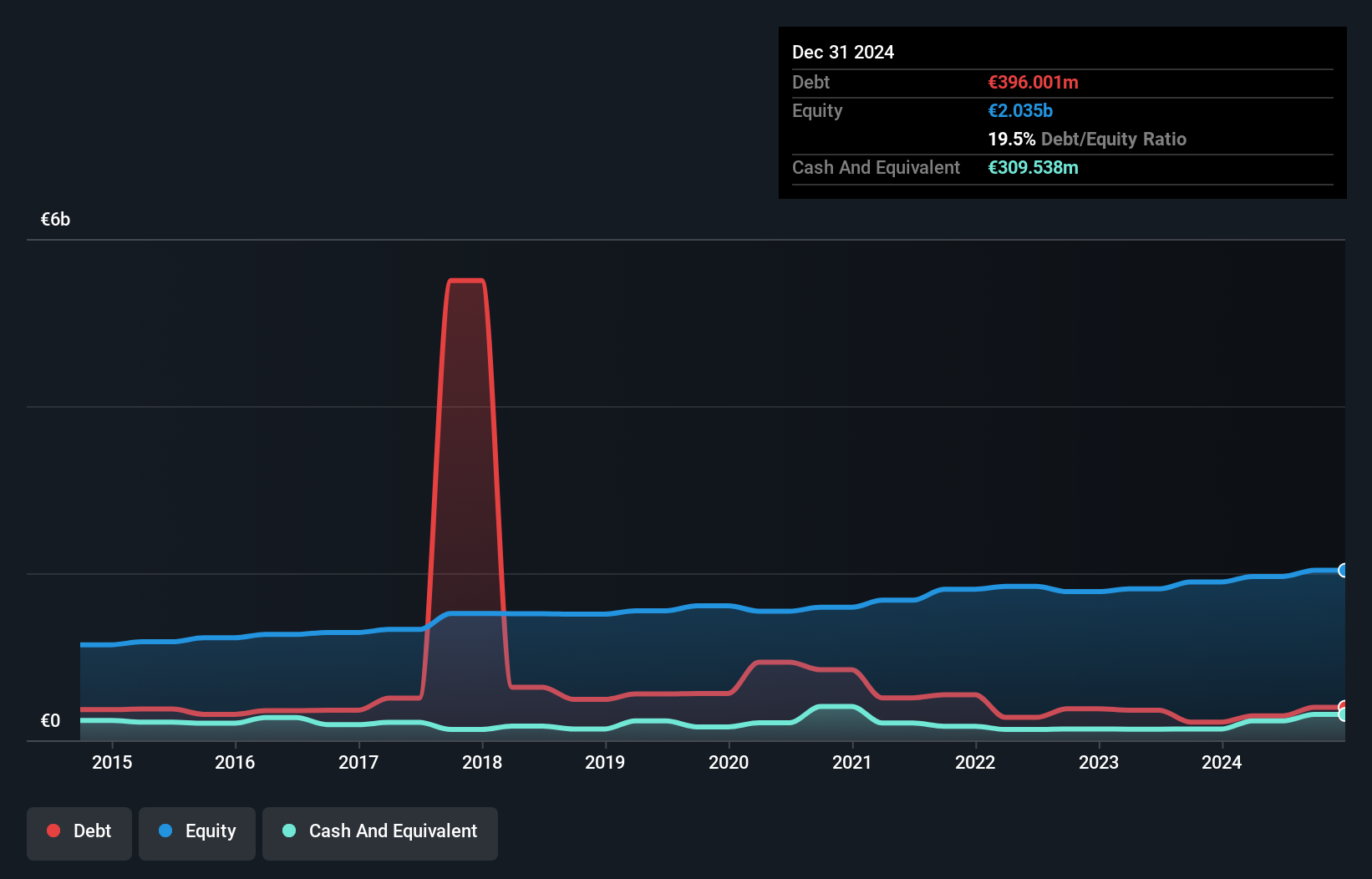

Caisse Regionale de Credit Agricole Mutuel Toulouse 31 (ENXTPA:CAT31)

Simply Wall St Value Rating: ★★★★★☆

Overview: Caisse Regionale de Credit Agricole Mutuel Toulouse 31 operates as a cooperative bank in France with a market capitalization of approximately €329.30 million.

Operations: The cooperative bank generates revenue primarily from its retail banking segment, amounting to €249.69 million.

CAT31's recent performance highlights its potential as an intriguing investment, with earnings growth of 25.4% over the past year, surpassing the industry average of 5.3%. The bank boasts total assets of €16.3 billion and equity of €2 billion, underpinned by deposits totaling €13.5 billion and loans amounting to €12 billion. Its financial health is reinforced by a low bad loan ratio at 1.4% and a modest allowance for bad loans at 85%. Trading at a significant discount—58% below estimated fair value—CAT31 draws interest with its high-quality earnings despite not being free cash flow positive recently.

- Delve into the full analysis health report here for a deeper understanding of Caisse Regionale de Credit Agricole Mutuel Toulouse 31.

Learn about Caisse Regionale de Credit Agricole Mutuel Toulouse 31's historical performance.

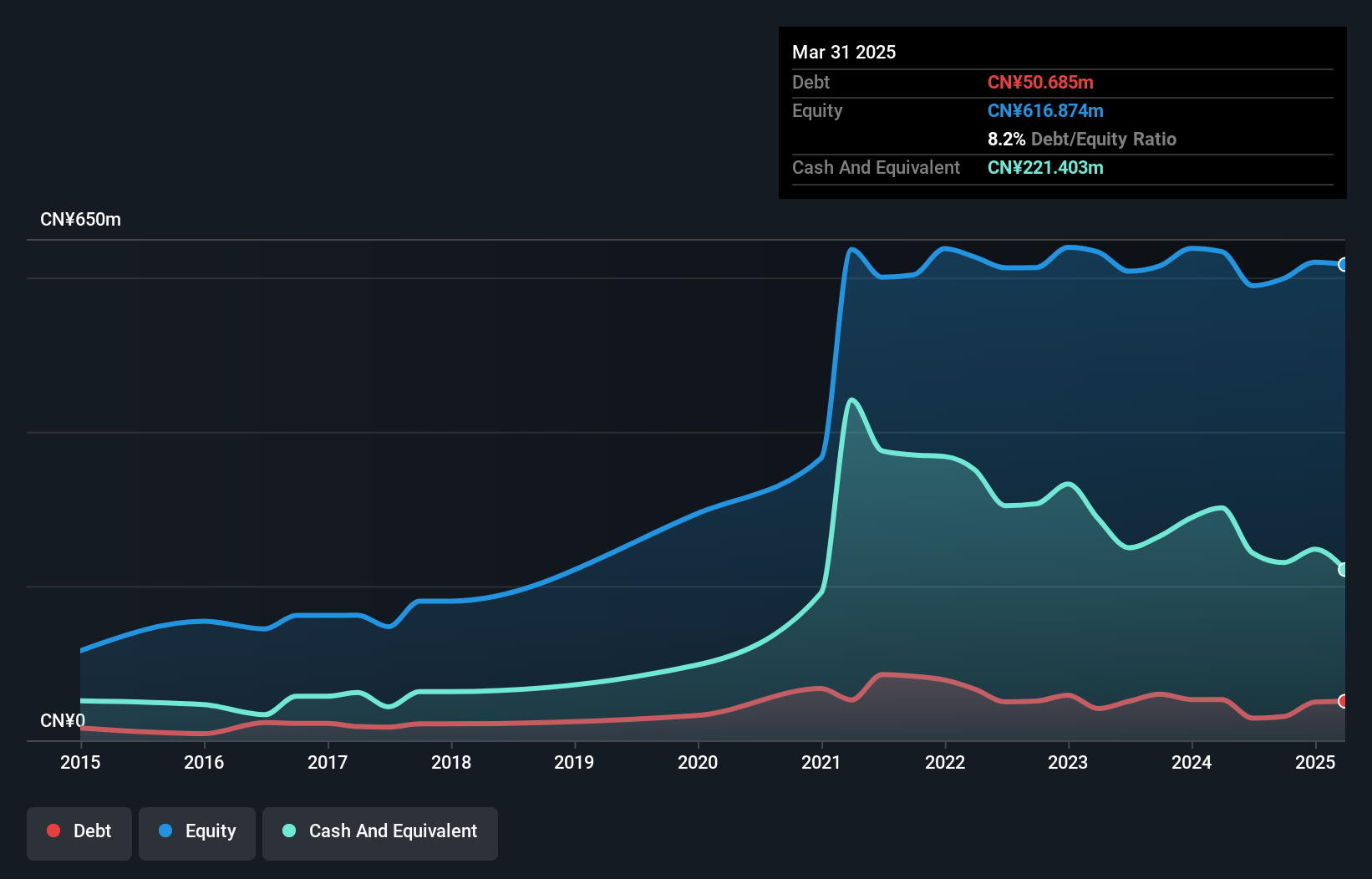

Shenzhen Tongye TechnologyLtd (SZSE:300960)

Simply Wall St Value Rating: ★★★★★★

Overview: Shenzhen Tongye Technology Co., Ltd. specializes in the research, development, production, sale, and maintenance of rail transit electrical equipment products in China and has a market capitalization of approximately CN¥2.47 billion.

Operations: Shenzhen Tongye Technology Co., Ltd. generates revenue primarily from the sale and maintenance of rail transit electrical equipment products in China. The company's net profit margin has shown fluctuations, reflecting changes in cost structures and operational efficiencies over recent periods.

Shenzhen Tongye Technology, a nimble player in its sector, has demonstrated robust performance with earnings jumping 33% over the past year, outpacing the broader machinery industry. The company's debt to equity ratio improved significantly from 11% to 5.1% over five years, indicating prudent financial management. Recent earnings announcements highlighted sales of CNY 262 million for nine months ending September 2024, up from CNY 217 million previously, while net income nearly doubled to CNY 31.52 million. Trading at a substantial discount of around 56% below estimated fair value suggests potential upside for investors eyeing growth opportunities.

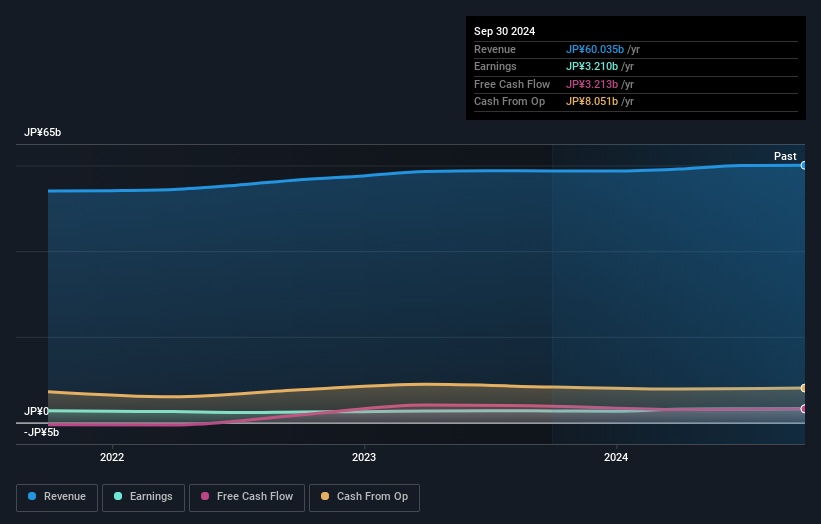

France Bed HoldingsLtd (TSE:7840)

Simply Wall St Value Rating: ★★★★★☆

Overview: France Bed Holdings Co., Ltd. operates in Japan through its subsidiaries, focusing on medical services and home furnishing and health businesses, with a market cap of ¥43.96 billion.

Operations: France Bed Holdings Co., Ltd. generates revenue primarily from its Medical Services segment, contributing ¥39.85 billion, and its Interior Health segment, which adds ¥19.90 billion. The company has a market capitalization of ¥43.96 billion.

France Bed Holdings, a smaller player in the healthcare sector, has shown promising financial health. Trading at 22.2% below its estimated fair value, it offers potential upside for investors. Its earnings growth of 18% over the past year outpaced the industry's 8%, indicating robust performance. The company is free cash flow positive with interest payments well covered by EBIT at an impressive 81x coverage ratio. Despite a rise in its debt-to-equity ratio from 18 to 35 over five years, it holds more cash than total debt, suggesting sound fiscal management and stability moving forward.

Key Takeaways

- Click this link to deep-dive into the 600 companies within our Undiscovered Gems With Strong Fundamentals screener.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Caisse Regionale de Credit Agricole Mutuel Toulouse 31, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:CAT31

Caisse Regionale de Credit Agricole Mutuel Toulouse 31

Operates as a cooperative bank in France.

Solid track record with excellent balance sheet.

Market Insights

Community Narratives