DorightLtd (SZSE:300950) Is Increasing Its Dividend To CN¥0.15

Doright Co.,Ltd. (SZSE:300950) has announced that it will be increasing its dividend from last year's comparable payment on the 11th of June to CN¥0.15. Despite this raise, the dividend yield of 1.0% is only a modest boost to shareholder returns.

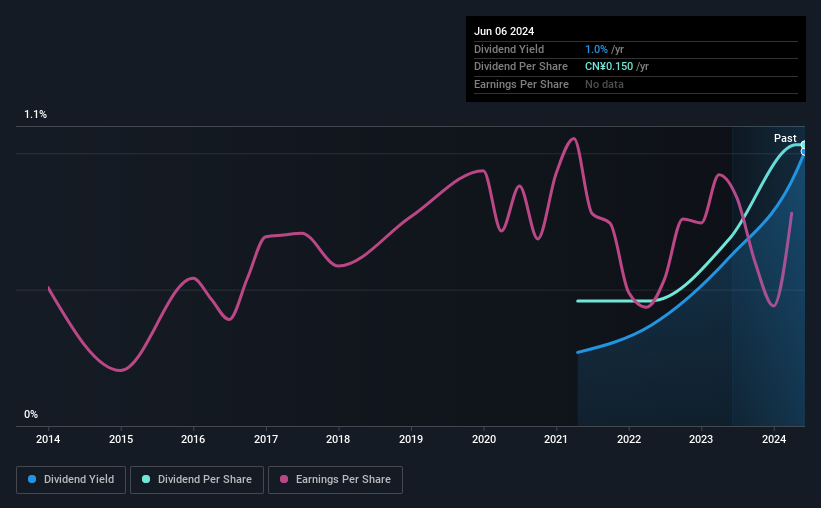

Check out our latest analysis for DorightLtd

DorightLtd's Dividend Is Well Covered By Earnings

If it is predictable over a long period, even low dividend yields can be attractive. Based on the last payment, DorightLtd was earning enough to cover the dividend, but free cash flows weren't positive. With the company not bringing in any cash, paying out to shareholders is bound to become difficult at some point.

Looking forward, earnings per share could rise by 0.2% over the next year if the trend from the last few years continues. Assuming the dividend continues along recent trends, we think the payout ratio could be 20% by next year, which is in a pretty sustainable range.

DorightLtd Is Still Building Its Track Record

The dividend has been pretty stable looking back, but the company hasn't been paying one for very long. This makes it tough to judge how it would fare through a full economic cycle. Since 2021, the annual payment back then was CN¥0.0667, compared to the most recent full-year payment of CN¥0.15. This means that it has been growing its distributions at 31% per annum over that time. We're not overly excited about the relatively short history of dividend payments, however the dividend is growing at a nice rate and we might take a closer look.

The Dividend's Growth Prospects Are Limited

The company's investors will be pleased to have been receiving dividend income for some time. However, DorightLtd's EPS was effectively flat over the past five years, which could stop the company from paying more every year. While EPS growth is quite low, DorightLtd has the option to increase the payout ratio to return more cash to shareholders.

In Summary

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. While DorightLtd is earning enough to cover the payments, the cash flows are lacking. We would be a touch cautious of relying on this stock primarily for the dividend income.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. To that end, DorightLtd has 3 warning signs (and 2 which make us uncomfortable) we think you should know about. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300950

DorightLtd

Engages in the design, research and development, manufacture, inspection, sale, and servicing of energy-saving environmental protection equipment in China.

Flawless balance sheet with proven track record.

Market Insights

Community Narratives