Many Still Looking Away From ActBlue Co., Ltd. (SZSE:300816)

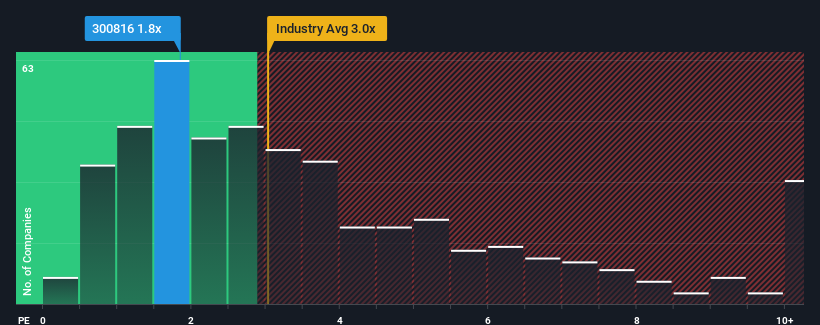

You may think that with a price-to-sales (or "P/S") ratio of 1.8x ActBlue Co., Ltd. (SZSE:300816) is a stock worth checking out, seeing as almost half of all the Machinery companies in China have P/S ratios greater than 3x and even P/S higher than 6x aren't out of the ordinary. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

View our latest analysis for ActBlue

How ActBlue Has Been Performing

Recent revenue growth for ActBlue has been in line with the industry. Perhaps the market is expecting future revenue performance to dive, which has kept the P/S suppressed. If you like the company, you'd be hoping this isn't the case so that you could pick up some stock while it's out of favour.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on ActBlue.How Is ActBlue's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as low as ActBlue's is when the company's growth is on track to lag the industry.

Retrospectively, the last year delivered a decent 6.2% gain to the company's revenues. The latest three year period has also seen a 22% overall rise in revenue, aided somewhat by its short-term performance. Therefore, it's fair to say the revenue growth recently has been respectable for the company.

Shifting to the future, estimates from the lone analyst covering the company suggest revenue should grow by 52% over the next year. Meanwhile, the rest of the industry is forecast to only expand by 22%, which is noticeably less attractive.

With this information, we find it odd that ActBlue is trading at a P/S lower than the industry. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

What Does ActBlue's P/S Mean For Investors?

Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

A look at ActBlue's revenues reveals that, despite glowing future growth forecasts, its P/S is much lower than we'd expect. There could be some major risk factors that are placing downward pressure on the P/S ratio. While the possibility of the share price plunging seems unlikely due to the high growth forecasted for the company, the market does appear to have some hesitation.

A lot of potential risks can sit within a company's balance sheet. Take a look at our free balance sheet analysis for ActBlue with six simple checks on some of these key factors.

If these risks are making you reconsider your opinion on ActBlue, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300816

ActBlue

Researches, develops, and sells diesel, gasoline, and natural gas engine exhaust after-treatment products.

High growth potential with adequate balance sheet.

Market Insights

Community Narratives