Advertisement

Ningbo BaoSi Energy Equipment Co., Ltd.'s (SZSE:300441) Share Price Boosted 35% But Its Business Prospects Need A Lift Too

Ningbo BaoSi Energy Equipment Co., Ltd. (SZSE:300441) shares have continued their recent momentum with a 35% gain in the last month alone. Looking back a bit further, it's encouraging to see the stock is up 34% in the last year.

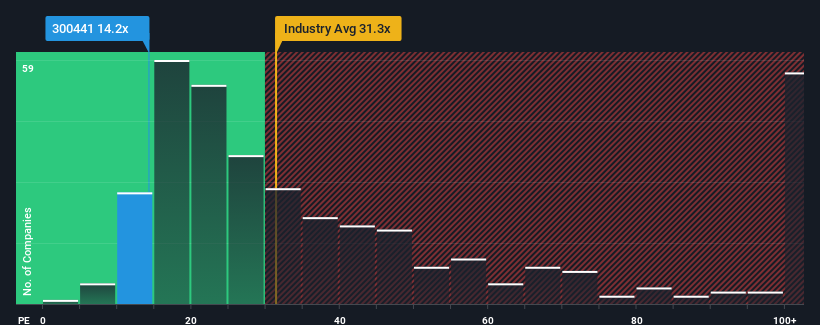

Although its price has surged higher, Ningbo BaoSi Energy Equipment's price-to-earnings (or "P/E") ratio of 14.2x might still make it look like a strong buy right now compared to the market in China, where around half of the companies have P/E ratios above 33x and even P/E's above 63x are quite common. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

Recent times have been pleasing for Ningbo BaoSi Energy Equipment as its earnings have risen in spite of the market's earnings going into reverse. One possibility is that the P/E is low because investors think the company's earnings are going to fall away like everyone else's soon. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

See our latest analysis for Ningbo BaoSi Energy Equipment

Does Growth Match The Low P/E?

Ningbo BaoSi Energy Equipment's P/E ratio would be typical for a company that's expected to deliver very poor growth or even falling earnings, and importantly, perform much worse than the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 242% last year. The strong recent performance means it was also able to grow EPS by 141% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Turning to the outlook, the next three years should generate growth of 16% each year as estimated by the sole analyst watching the company. With the market predicted to deliver 19% growth per year, the company is positioned for a weaker earnings result.

With this information, we can see why Ningbo BaoSi Energy Equipment is trading at a P/E lower than the market. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Bottom Line On Ningbo BaoSi Energy Equipment's P/E

Even after such a strong price move, Ningbo BaoSi Energy Equipment's P/E still trails the rest of the market significantly. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Ningbo BaoSi Energy Equipment's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Plus, you should also learn about these 3 warning signs we've spotted with Ningbo BaoSi Energy Equipment (including 2 which don't sit too well with us).

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Ningbo BaoSi Energy Equipment might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300441

Ningbo BaoSi Energy Equipment

Engages in research, development, production, and sale of high-end precision mechanical parts and sets of equipment in China and internationally.

Solid track record with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.8% undervalued

NO

Community Contributor