Advertisement

Linzhou Heavy Machinery Group Co.,Ltd (SZSE:002535) Might Not Be As Mispriced As It Looks After Plunging 27%

Unfortunately for some shareholders, the Linzhou Heavy Machinery Group Co.,Ltd (SZSE:002535) share price has dived 27% in the last thirty days, prolonging recent pain. The recent drop has obliterated the annual return, with the share price now down 3.1% over that longer period.

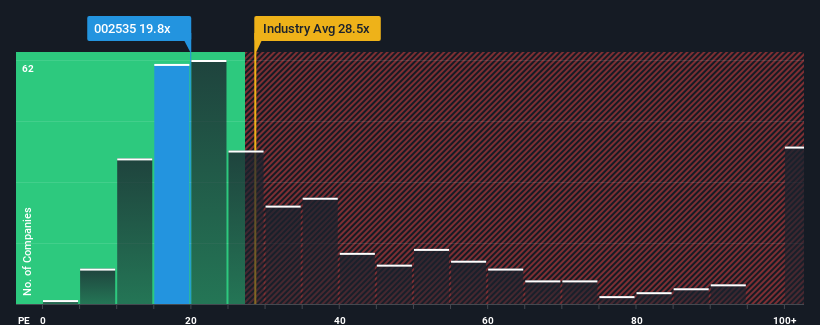

Following the heavy fall in price, Linzhou Heavy Machinery GroupLtd's price-to-earnings (or "P/E") ratio of 19.8x might make it look like a buy right now compared to the market in China, where around half of the companies have P/E ratios above 31x and even P/E's above 57x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

Linzhou Heavy Machinery GroupLtd certainly has been doing a great job lately as it's been growing earnings at a really rapid pace. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If that doesn't eventuate, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

View our latest analysis for Linzhou Heavy Machinery GroupLtd

What Are Growth Metrics Telling Us About The Low P/E?

In order to justify its P/E ratio, Linzhou Heavy Machinery GroupLtd would need to produce sluggish growth that's trailing the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 203% last year. The strong recent performance means it was also able to grow EPS by 197% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

This is in contrast to the rest of the market, which is expected to grow by 38% over the next year, materially lower than the company's recent medium-term annualised growth rates.

With this information, we find it odd that Linzhou Heavy Machinery GroupLtd is trading at a P/E lower than the market. Apparently some shareholders believe the recent performance has exceeded its limits and have been accepting significantly lower selling prices.

The Final Word

The softening of Linzhou Heavy Machinery GroupLtd's shares means its P/E is now sitting at a pretty low level. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Linzhou Heavy Machinery GroupLtd currently trades on a much lower than expected P/E since its recent three-year growth is higher than the wider market forecast. When we see strong earnings with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. It appears many are indeed anticipating earnings instability, because the persistence of these recent medium-term conditions would normally provide a boost to the share price.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Linzhou Heavy Machinery GroupLtd that you need to be mindful of.

If these risks are making you reconsider your opinion on Linzhou Heavy Machinery GroupLtd, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002535

Linzhou Heavy Machinery GroupLtd

Manufactures and sells coal mining machinery in China.

Good value with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|40.2% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.1% undervalued

UN

Community Contributor