Advertisement

- China

- /

- Electrical

- /

- SZSE:002339

Integrated Electronic Systems Lab Co., Ltd.'s (SZSE:002339) Shares Bounce 26% But Its Business Still Trails The Industry

Those holding Integrated Electronic Systems Lab Co., Ltd. (SZSE:002339) shares would be relieved that the share price has rebounded 26% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 32% over that time.

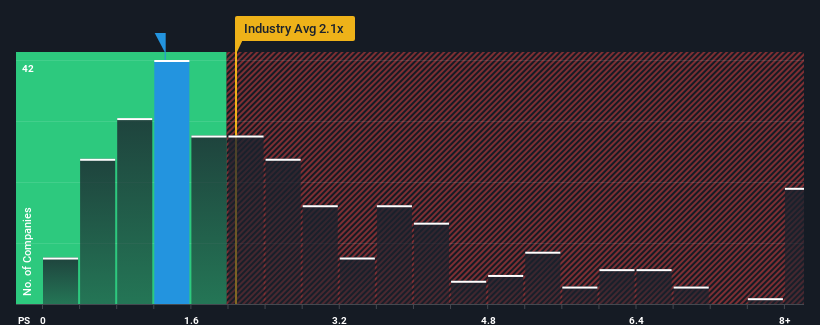

Although its price has surged higher, when close to half the companies operating in China's Electrical industry have price-to-sales ratios (or "P/S") above 2.1x, you may still consider Integrated Electronic Systems Lab as an enticing stock to check out with its 1.3x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

Check out our latest analysis for Integrated Electronic Systems Lab

How Integrated Electronic Systems Lab Has Been Performing

Revenue has risen firmly for Integrated Electronic Systems Lab recently, which is pleasing to see. Perhaps the market is expecting this acceptable revenue performance to take a dive, which has kept the P/S suppressed. If that doesn't eventuate, then existing shareholders have reason to be optimistic about the future direction of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Integrated Electronic Systems Lab will help you shine a light on its historical performance.Is There Any Revenue Growth Forecasted For Integrated Electronic Systems Lab?

There's an inherent assumption that a company should underperform the industry for P/S ratios like Integrated Electronic Systems Lab's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 16% gain to the company's top line. As a result, it also grew revenue by 22% in total over the last three years. Accordingly, shareholders would have probably been satisfied with the medium-term rates of revenue growth.

Comparing the recent medium-term revenue trends against the industry's one-year growth forecast of 26% shows it's noticeably less attractive.

With this in consideration, it's easy to understand why Integrated Electronic Systems Lab's P/S falls short of the mark set by its industry peers. It seems most investors are expecting to see the recent limited growth rates continue into the future and are only willing to pay a reduced amount for the stock.

What We Can Learn From Integrated Electronic Systems Lab's P/S?

The latest share price surge wasn't enough to lift Integrated Electronic Systems Lab's P/S close to the industry median. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

In line with expectations, Integrated Electronic Systems Lab maintains its low P/S on the weakness of its recent three-year growth being lower than the wider industry forecast. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

Before you settle on your opinion, we've discovered 1 warning sign for Integrated Electronic Systems Lab that you should be aware of.

If these risks are making you reconsider your opinion on Integrated Electronic Systems Lab, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002339

Integrated Electronic Systems Lab

Integrated Electronic Systems Lab Co., Ltd.

Adequate balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|40.2% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|62.7% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.1% undervalued

UN

Community Contributor