The Market Lifts Han's Laser Technology Industry Group Co., Ltd. (SZSE:002008) Shares 29% But It Can Do More

Han's Laser Technology Industry Group Co., Ltd. (SZSE:002008) shareholders are no doubt pleased to see that the share price has bounced 29% in the last month, although it is still struggling to make up recently lost ground. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 32% in the last twelve months.

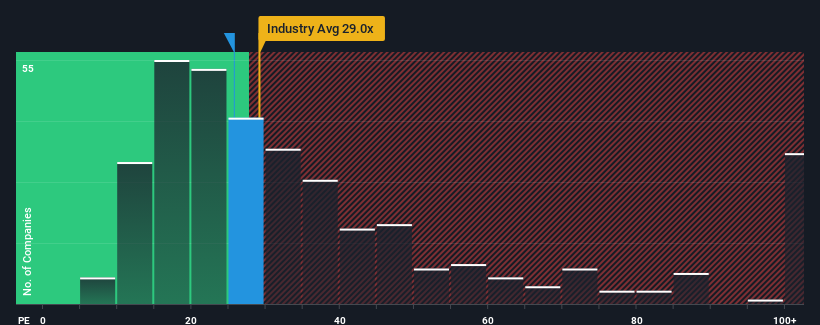

In spite of the firm bounce in price, Han's Laser Technology Industry Group may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 25.7x, since almost half of all companies in China have P/E ratios greater than 31x and even P/E's higher than 56x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

With earnings that are retreating more than the market's of late, Han's Laser Technology Industry Group has been very sluggish. It seems that many are expecting the dismal earnings performance to persist, which has repressed the P/E. You'd much rather the company wasn't bleeding earnings if you still believe in the business. If not, then existing shareholders will probably struggle to get excited about the future direction of the share price.

See our latest analysis for Han's Laser Technology Industry Group

Does Growth Match The Low P/E?

There's an inherent assumption that a company should underperform the market for P/E ratios like Han's Laser Technology Industry Group's to be considered reasonable.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 45%. The last three years don't look nice either as the company has shrunk EPS by 22% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Shifting to the future, estimates from the analysts covering the company suggest earnings should grow by 21% per year over the next three years. That's shaping up to be similar to the 22% per annum growth forecast for the broader market.

With this information, we find it odd that Han's Laser Technology Industry Group is trading at a P/E lower than the market. Apparently some shareholders are doubtful of the forecasts and have been accepting lower selling prices.

The Bottom Line On Han's Laser Technology Industry Group's P/E

Despite Han's Laser Technology Industry Group's shares building up a head of steam, its P/E still lags most other companies. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Han's Laser Technology Industry Group currently trades on a lower than expected P/E since its forecast growth is in line with the wider market. There could be some unobserved threats to earnings preventing the P/E ratio from matching the outlook. It appears some are indeed anticipating earnings instability, because these conditions should normally provide more support to the share price.

Before you settle on your opinion, we've discovered 3 warning signs for Han's Laser Technology Industry Group that you should be aware of.

If you're unsure about the strength of Han's Laser Technology Industry Group's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Han's Laser Technology Industry Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002008

Han's Laser Technology Industry Group

Researches, develops, produces, and sells laser processing equipment in China and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Community Narratives