Advertisement

February 2025's Top Growth Companies With High Insider Ownership

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate geopolitical tensions and consumer spending concerns, with major indexes experiencing fluctuations, investors are increasingly looking for growth opportunities that can weather economic uncertainties. In this environment, companies with high insider ownership often attract attention due to the potential alignment of interests between management and shareholders, which can be a key factor in identifying promising growth stocks.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Propel Holdings (TSX:PRL) | 36.5% | 38.7% |

| Seojin SystemLtd (KOSDAQ:A178320) | 32.1% | 39.9% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 10.4% | 26.2% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| CD Projekt (WSE:CDR) | 29.7% | 39.4% |

| Pharma Mar (BME:PHM) | 11.9% | 45.4% |

| Kingstone Companies (NasdaqCM:KINS) | 20.8% | 24.9% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 121.1% |

| Plenti Group (ASX:PLT) | 12.7% | 120.1% |

| Fulin Precision (SZSE:300432) | 13.6% | 71% |

We'll examine a selection from our screener results.

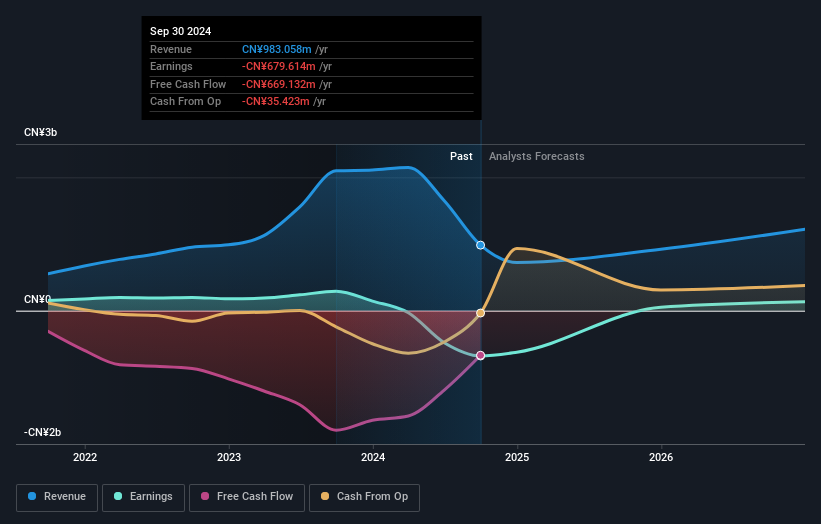

Beijing Tianyishangjia New Material (SHSE:688033)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Beijing Tianyishangjia New Material Corp., Ltd. operates in the new materials industry with a market cap of CN¥3.40 billion.

Operations: Beijing Tianyishangjia New Material Corp., Ltd. generates its revenue from various segments within the new materials industry.

Insider Ownership: 25.8%

Earnings Growth Forecast: 106.6% p.a.

Beijing Tianyishangjia New Material is forecast to grow its revenue at 15.5% annually, outpacing the Chinese market's 13.4% growth rate, but still below a high-growth threshold of 20%. The company is expected to achieve profitability within three years, surpassing average market growth expectations. Despite being dropped from the S&P Global BMI Index in December 2024, no substantial insider trading activity has been reported recently. Return on equity remains low at a forecasted 2.4%.

- Get an in-depth perspective on Beijing Tianyishangjia New Material's performance by reading our analyst estimates report here.

- Our valuation report unveils the possibility Beijing Tianyishangjia New Material's shares may be trading at a premium.

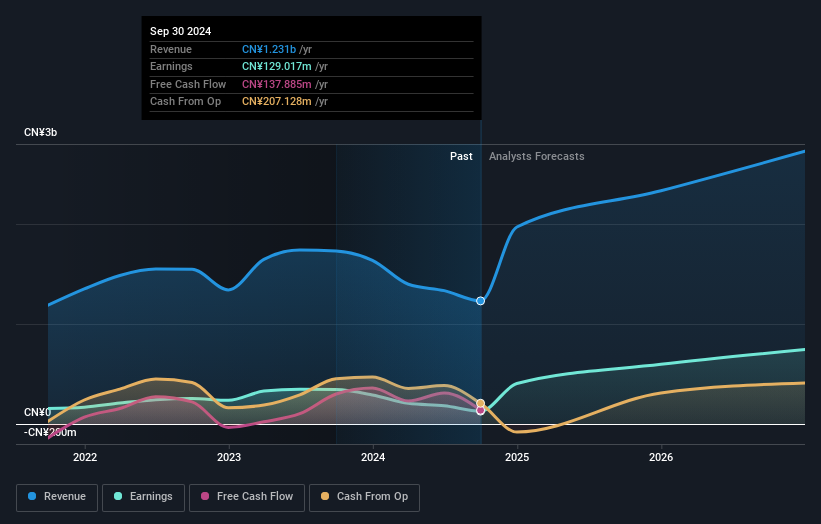

Beijing Tieke Shougang Rail Way-Tech (SHSE:688569)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Beijing Tieke Shougang Rail Way-Tech Co., Ltd. operates in the railway technology sector and has a market cap of CN¥4.36 billion.

Operations: The company's revenue from Industrial Manufacturing is CN¥1.23 billion.

Insider Ownership: 12%

Earnings Growth Forecast: 51.5% p.a.

Beijing Tieke Shougang Rail Way-Tech is trading at a favorable value with a P/E ratio of 34x, below the Chinese market average. The company is poised for significant growth, with earnings expected to rise by 51.5% annually and revenue projected to grow at 27.5% per year, both surpassing market averages. However, profit margins have declined from last year and the return on equity remains low at a forecasted 17.6%. No recent insider trading activity has been noted.

- Delve into the full analysis future growth report here for a deeper understanding of Beijing Tieke Shougang Rail Way-Tech.

- Our expertly prepared valuation report Beijing Tieke Shougang Rail Way-Tech implies its share price may be lower than expected.

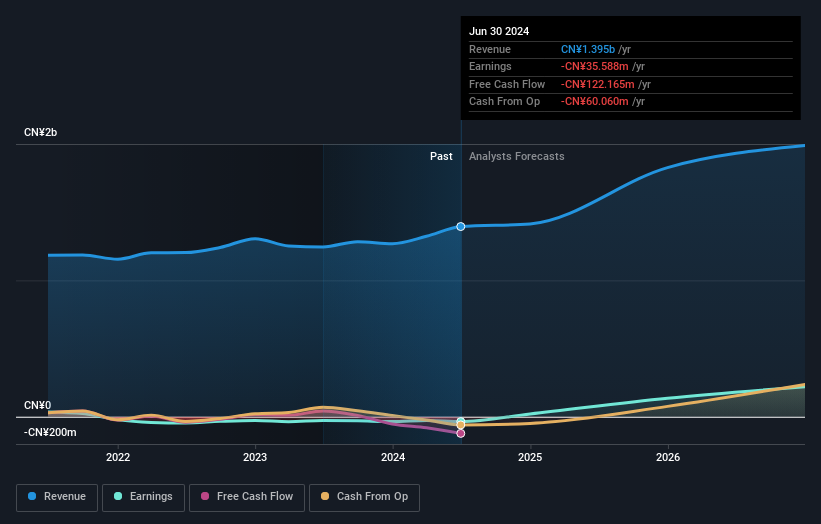

Xiamen Wanli Stone StockLtd (SZSE:002785)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Xiamen Wanli Stone Stock Co., Ltd is engaged in the development, processing, and installation of stone products, construction stones, stone carving handicrafts, and mineral products across China and international markets including Japan, South Korea, and the United States; it has a market cap of CN¥6.67 billion.

Operations: The company's revenue primarily comes from its Stone Processing and Manufacturing Industry segment, which generated CN¥1.01 billion.

Insider Ownership: 18.9%

Earnings Growth Forecast: 107.5% p.a.

Xiamen Wanli Stone Stock Ltd. is expected to see substantial earnings growth of 107.53% per year, outpacing the Chinese market's revenue growth rate of 13.4%. Despite a forecasted low return on equity at 15.3%, the company is set to become profitable within three years, exceeding average market profit growth expectations. Recent events include a shareholder meeting discussing changes in audit firms and independent director elections, with no significant insider trading activity noted recently.

- Dive into the specifics of Xiamen Wanli Stone StockLtd here with our thorough growth forecast report.

- Our comprehensive valuation report raises the possibility that Xiamen Wanli Stone StockLtd is priced higher than what may be justified by its financials.

Turning Ideas Into Actions

- Embark on your investment journey to our 1450 Fast Growing Companies With High Insider Ownership selection here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Beijing Tieke Shougang Rail Way-Tech might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688569

Beijing Tieke Shougang Rail Way-Tech

Beijing Tieke Shougang Rail Way-Tech Co., Ltd.

Solid track record with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor