As global markets rally with U.S. stocks nearing record highs, driven by optimism around AI investments and potential trade deals, investors are increasingly focused on growth stocks that have outperformed their value counterparts recently. In this buoyant environment, companies with significant insider ownership often attract attention as they suggest confidence from those who know the business best.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 26.3% |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 41.2% |

| Laopu Gold (SEHK:6181) | 36.4% | 36.6% |

| Waystream Holding (OM:WAYS) | 11.3% | 113.3% |

| Medley (TSE:4480) | 34.1% | 27.3% |

| Brightstar Resources (ASX:BTR) | 16.2% | 84.1% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.2% | 135% |

| Fulin Precision (SZSE:300432) | 13.6% | 71% |

| HANA Micron (KOSDAQ:A067310) | 18.2% | 119.4% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 121.1% |

Let's uncover some gems from our specialized screener.

JHT DesignLtd (SHSE:603061)

Simply Wall St Growth Rating: ★★★★★☆

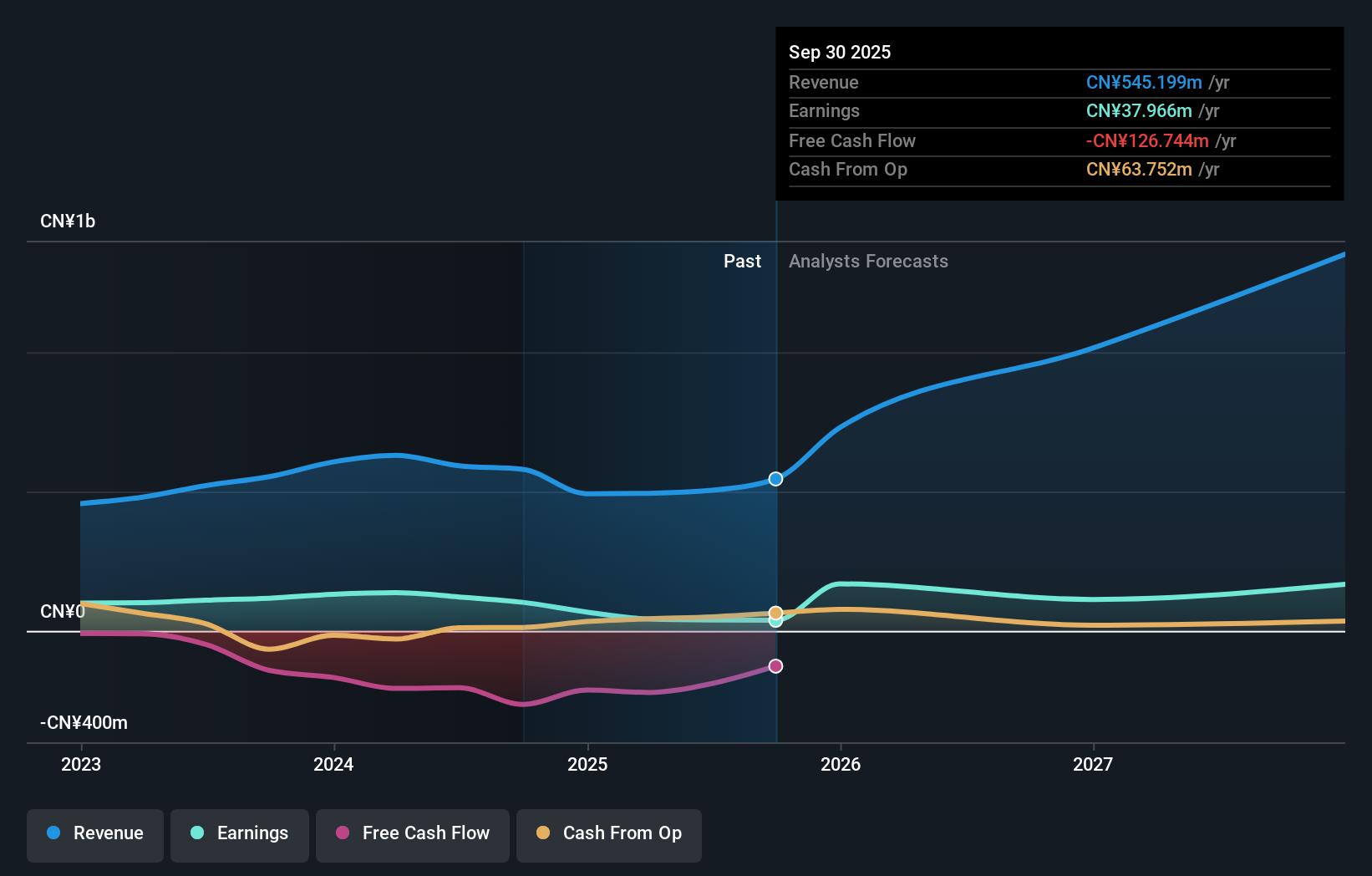

Overview: JHT Design Co., Ltd. is involved in the research, development, production, and sale of semiconductor chip testing equipment in China, with a market cap of CN¥4.67 billion.

Operations: I'm sorry, but it seems that there is no specific revenue segment information provided in the text you supplied. If you have more detailed data on their revenue segments, I would be happy to help summarize it for you.

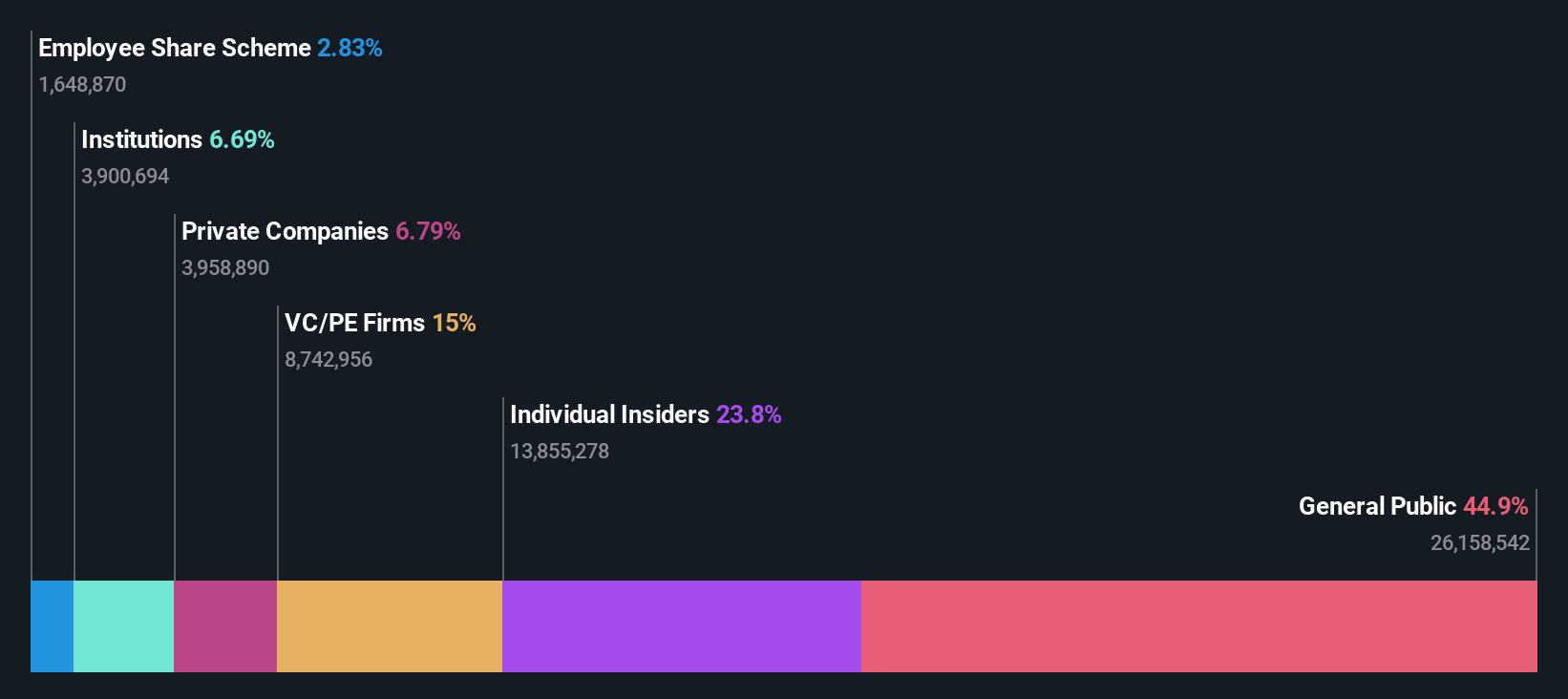

Insider Ownership: 23.8%

Revenue Growth Forecast: 29.3% p.a.

JHT Design Ltd. showcases significant growth potential with its earnings forecasted to grow 33.9% annually, outpacing the Chinese market average of 25.1%. Despite a decline in recent earnings, the company anticipates revenue growth of 29.3% per year, surpassing market expectations. Insider ownership remains high without notable buying or selling activity recently. The price-to-earnings ratio of 60.7x is competitive within the semiconductor industry, suggesting reasonable valuation amidst high-quality earnings influenced by large one-off items.

- Get an in-depth perspective on JHT DesignLtd's performance by reading our analyst estimates report here.

- Insights from our recent valuation report point to the potential overvaluation of JHT DesignLtd shares in the market.

Farsoon Technologies (SHSE:688433)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Farsoon Technologies supplies industrial plastic laser sintering and metal laser melting systems across China, North America, and Europe, with a market cap of CN¥10.52 billion.

Operations: The company's revenue segment includes Machinery & Industrial Equipment, contributing CN¥579.72 million.

Insider Ownership: 11.5%

Revenue Growth Forecast: 52.3% p.a.

Farsoon Technologies is poised for robust growth, with revenue expected to increase 52.3% annually, significantly outpacing the broader Chinese market's 13.4%. Earnings are forecasted to grow at a very high rate of 68.4% per year, indicating strong potential despite recent share price volatility and insufficient data on return on equity projections. No insider trading activity has been reported in the last three months, suggesting stability in insider sentiment.

- Dive into the specifics of Farsoon Technologies here with our thorough growth forecast report.

- In light of our recent valuation report, it seems possible that Farsoon Technologies is trading beyond its estimated value.

Dalian Haosen Intelligent Manufacturing (SHSE:688529)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Dalian Haosen Intelligent Manufacturing Co., Ltd. operates in the field of intelligent manufacturing solutions and has a market cap of CN¥2.68 billion.

Operations: Revenue Segments (in millions of CN¥): null

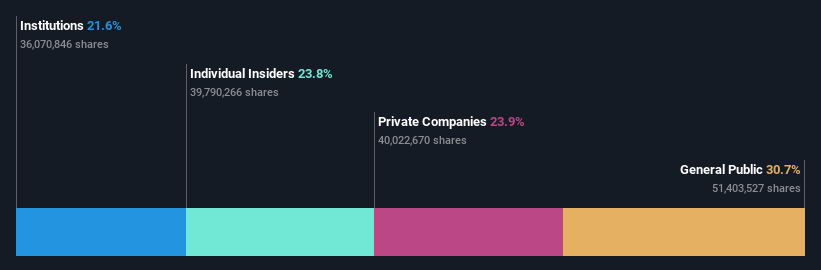

Insider Ownership: 23.8%

Revenue Growth Forecast: 17.3% p.a.

Dalian Haosen Intelligent Manufacturing is trading at a good value compared to peers, with revenue projected to grow 17.3% annually, surpassing the broader Chinese market's growth rate of 13.4%. However, interest payments are not well covered by earnings, and its low return on equity forecast of 6.7% in three years raises concerns. Despite no recent insider trading activity, the company aims for profitability within three years with earnings expected to grow at an impressive annual rate of 87.12%.

- Click to explore a detailed breakdown of our findings in Dalian Haosen Intelligent Manufacturing's earnings growth report.

- According our valuation report, there's an indication that Dalian Haosen Intelligent Manufacturing's share price might be on the cheaper side.

Summing It All Up

- Unlock our comprehensive list of 1470 Fast Growing Companies With High Insider Ownership by clicking here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688529

Dalian Haosen Intelligent Manufacturing

Dalian Haosen Intelligent Manufacturing Co., Ltd.

Reasonable growth potential and fair value.

Market Insights

Community Narratives