As global markets navigate the complexities of shifting political landscapes and economic indicators, investors are closely watching how policy changes might impact corporate earnings and sector performances. Amid these fluctuations, growth companies with high insider ownership often garner attention for their potential resilience and alignment of interests between management and shareholders. In this context, understanding the characteristics that make a stock attractive—such as strong growth prospects coupled with significant insider investment—can be crucial in evaluating opportunities within today's market environment.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Seojin SystemLtd (KOSDAQ:A178320) | 31.1% | 52.4% |

| On Holding (NYSE:ONON) | 19.1% | 29.7% |

| Pharma Mar (BME:PHM) | 11.8% | 56.9% |

| Medley (TSE:4480) | 34% | 31.7% |

| Findi (ASX:FND) | 34.8% | 71.5% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 103.6% |

| Plenti Group (ASX:PLT) | 12.8% | 120.1% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.8% | 95% |

| Alkami Technology (NasdaqGS:ALKT) | 11% | 98.6% |

| Brightstar Resources (ASX:BTR) | 16.2% | 84.6% |

Below we spotlight a couple of our favorites from our exclusive screener.

Hunan Oil Pump (SHSE:603319)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Hunan Oil Pump Co., Ltd. manufactures and sells oil pumps both in China and internationally, with a market cap of CN¥5.02 billion.

Operations: Hunan Oil Pump Co., Ltd. generates revenue through the manufacture and sale of oil pumps in both domestic and international markets.

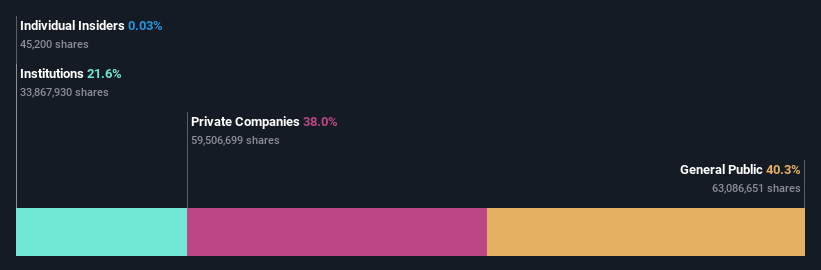

Insider Ownership: 32.7%

Hunan Oil Pump demonstrates strong growth potential with forecasted revenue and earnings growth rates of 27.5% and 28.48% per year, respectively, outpacing the broader Chinese market. Its price-to-earnings ratio of 24.4x suggests it is valued attractively compared to the CN market's average of 36x. Recent earnings show a slight decline in net income despite increased sales, highlighting potential profitability challenges that may impact its ability to sustain dividends at current levels.

- Click to explore a detailed breakdown of our findings in Hunan Oil Pump's earnings growth report.

- The valuation report we've compiled suggests that Hunan Oil Pump's current price could be inflated.

Wetown Electric Group (SHSE:688226)

Simply Wall St Growth Rating: ★★★★★★

Overview: Wetown Electric Group Co., Ltd. focuses on the research, development, production, and sale of electrical products both in China and internationally, with a market cap of CN¥2.94 billion.

Operations: The company generates revenue through the research, development, production, and sale of electrical products across domestic and international markets.

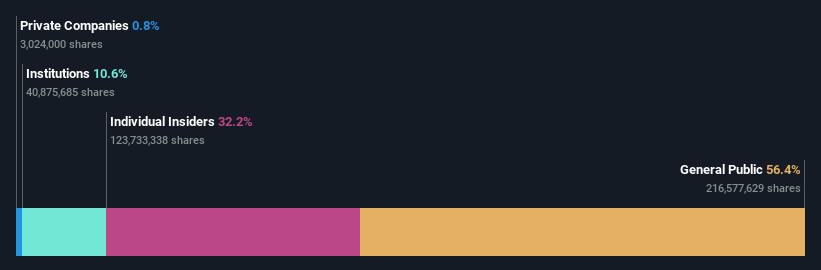

Insider Ownership: 22.3%

Wetown Electric Group exhibits robust growth potential, with earnings and revenue forecasted to grow significantly faster than the Chinese market. Recent results show a substantial increase in sales to CNY 2.74 billion, with net income rising to CNY 109.04 million. Trading at a price-to-earnings ratio of 21.2x, it is considered good value compared to the market average of 36x. However, its dividend yield of 1.19% is not well covered by free cash flows, indicating potential sustainability issues.

- Navigate through the intricacies of Wetown Electric Group with our comprehensive analyst estimates report here.

- In light of our recent valuation report, it seems possible that Wetown Electric Group is trading behind its estimated value.

Guangdong Yussen Energy Technology (SZSE:002986)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Guangdong Yussen Energy Technology Co., Ltd. operates in the energy technology sector with a market cap of CN¥4.75 billion.

Operations: Unfortunately, the revenue segments for Guangdong Yussen Energy Technology Co., Ltd. are not provided in the text you shared, so I'm unable to summarize them.

Insider Ownership: 32.1%

Guangdong Yussen Energy Technology's revenue is forecast to grow 21.3% annually, outpacing the Chinese market, with earnings expected to rise significantly by 36.87%. Despite this growth potential, profit margins have declined from last year. The company trades at a favorable price-to-earnings ratio of 13.6x compared to the market average of 36x but has diluted shareholders recently. Recent earnings showed a decrease in net income despite higher sales, impacting overall profitability.

- Click here and access our complete growth analysis report to understand the dynamics of Guangdong Yussen Energy Technology.

- Our valuation report unveils the possibility Guangdong Yussen Energy Technology's shares may be trading at a discount.

Summing It All Up

- Discover the full array of 1530 Fast Growing Companies With High Insider Ownership right here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

If you're looking to trade Guangdong Yussen Energy Technology, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002986

Guangdong Yussen Energy Technology

Guangdong Yussen Energy Technology Co., Ltd.

High growth potential with adequate balance sheet.