Advertisement

Amidst a backdrop of fluctuating economic indicators and evolving market conditions, Asian markets have shown resilience with indices like the CSI 300 and Shanghai Composite posting gains, driven by optimism in technology and AI sectors. In this environment, growth companies with high insider ownership can be particularly appealing as they often signal strong alignment between management and shareholder interests, potentially enhancing investor confidence during times of economic uncertainty.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| WinWay Technology (TWSE:6515) | 21.7% | 30.3% |

| UTI (KOSDAQ:A179900) | 25.2% | 120.7% |

| Streamax Technology (SZSE:002970) | 32.5% | 33.1% |

| Seers Technology (KOSDAQ:A458870) | 33.9% | 78.8% |

| Novoray (SHSE:688300) | 23.6% | 31.4% |

| Loadstar Capital K.K (TSE:3482) | 31% | 23.6% |

| Laopu Gold (SEHK:6181) | 34.8% | 34.3% |

| J&V Energy Technology (TWSE:6869) | 17.5% | 31.6% |

| Gold Circuit Electronics (TWSE:2368) | 31.4% | 37.2% |

| Fulin Precision (SZSE:300432) | 11.6% | 55.2% |

Below we spotlight a couple of our favorites from our exclusive screener.

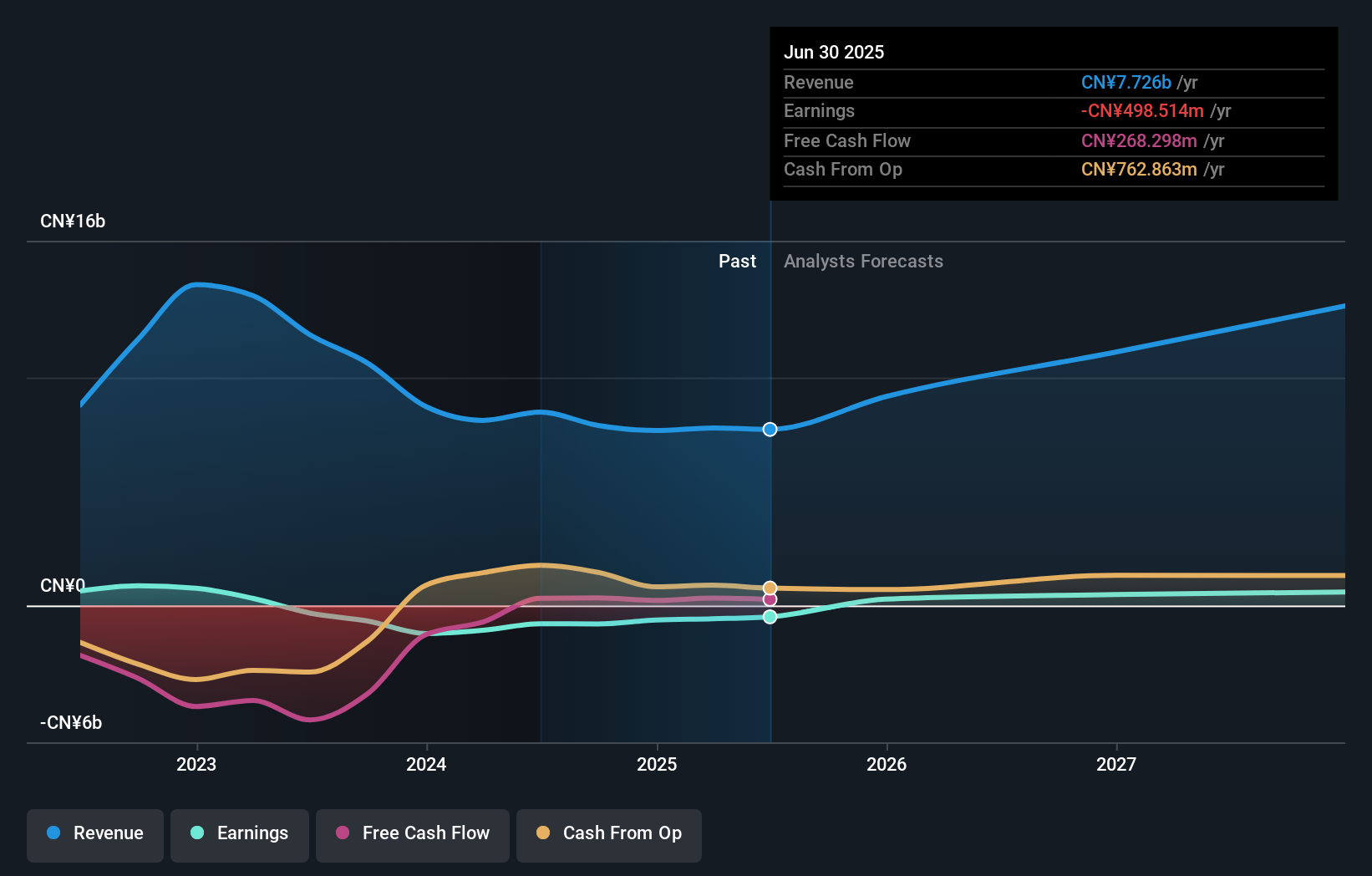

Jiangsu Lopal Tech. Group (SHSE:603906)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Jiangsu Lopal Tech. Group Co., Ltd. focuses on the R&D, production, and sale of lithium iron phosphate cathode materials and environmental protection fine chemicals for vehicles both in China and internationally, with a market cap of CN¥14.98 billion.

Operations: The company's revenue segments include the production and sale of lithium iron phosphate cathode materials and environmental protection fine chemicals for vehicles.

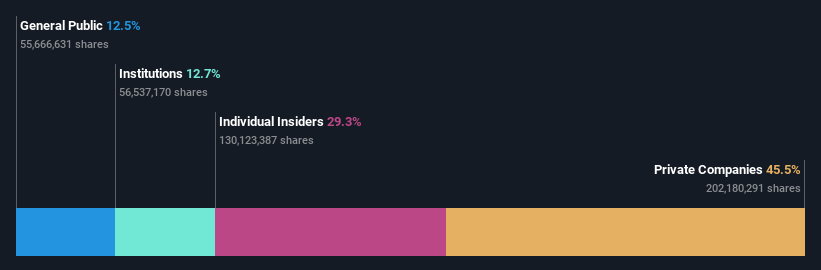

Insider Ownership: 34.7%

Earnings Growth Forecast: 89.6% p.a.

Jiangsu Lopal Tech. Group's revenue is forecast to grow at 22% annually, outpacing the Chinese market average of 14.6%. The company reported a narrowing net loss of CNY 110.47 million for the first nine months of 2025, with sales reaching CNY 5.83 billion. Despite recent volatility in its share price, analysts expect earnings to grow significantly by 89.61% per year and project profitability within three years, indicating strong growth potential amidst high insider ownership levels.

- Click to explore a detailed breakdown of our findings in Jiangsu Lopal Tech. Group's earnings growth report.

- Our comprehensive valuation report raises the possibility that Jiangsu Lopal Tech. Group is priced higher than what may be justified by its financials.

Bozhon Precision Industry TechnologyLtd (SHSE:688097)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Bozhon Precision Industry Technology Co., Ltd. (ticker: SHSE:688097) operates in the precision machinery industry, focusing on the design and manufacture of automation equipment, with a market cap of CN¥15.27 billion.

Operations: The company's revenue is primarily derived from its Industrial Automation & Controls segment, amounting to CN¥5.33 billion.

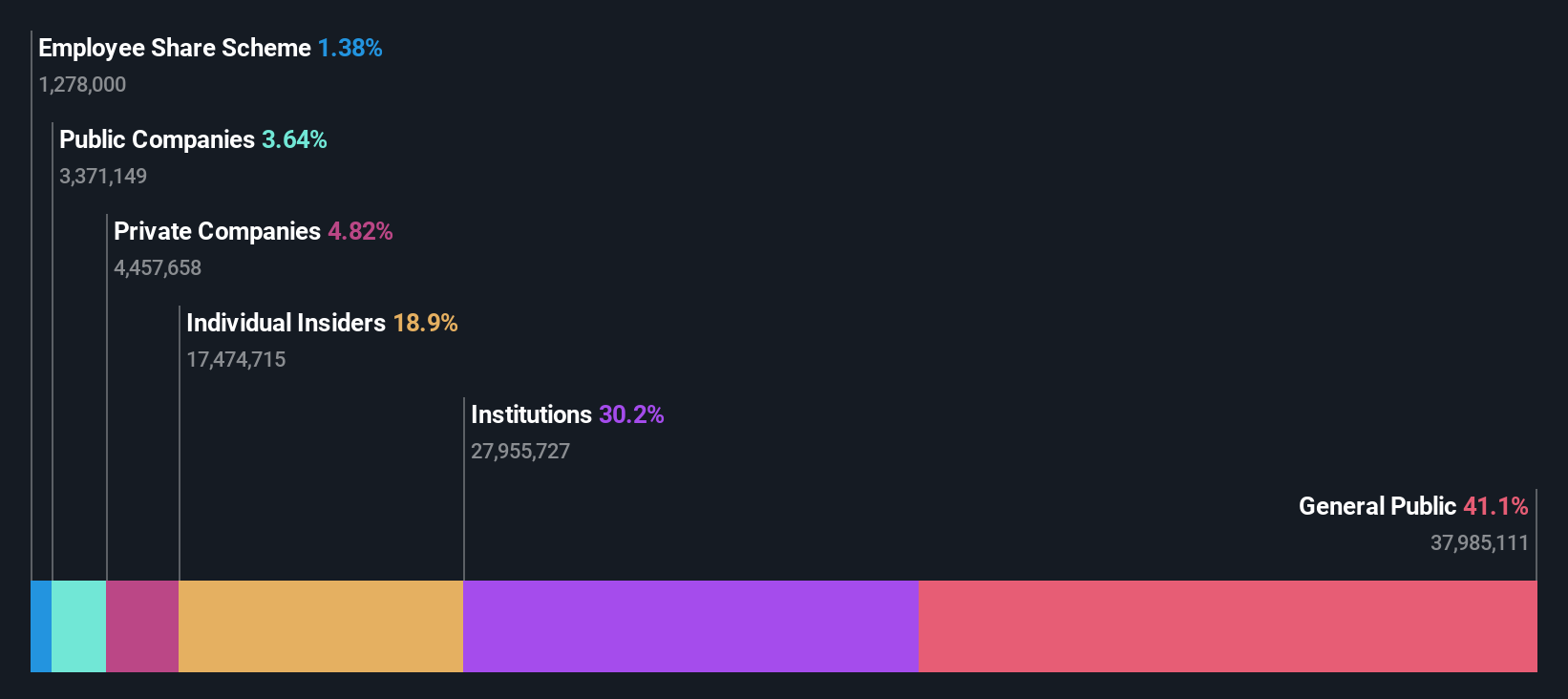

Insider Ownership: 30%

Earnings Growth Forecast: 23.9% p.a.

Bozhon Precision Industry Technology Ltd. has demonstrated strong financial performance, with revenue reaching CNY 3.65 billion for the first nine months of 2025, up from CNY 3.27 billion a year earlier. Net income also increased to CNY 332.38 million, reflecting robust growth in earnings per share from continuing operations to CNY 0.744. Despite high insider ownership and forecasted revenue growth of over 20% annually, its expected earnings growth lags behind the broader Chinese market projections.

- Dive into the specifics of Bozhon Precision Industry TechnologyLtd here with our thorough growth forecast report.

- Our valuation report unveils the possibility Bozhon Precision Industry TechnologyLtd's shares may be trading at a discount.

Shenzhen SEICHI Technologies (SHSE:688627)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shenzhen SEICHI Technologies Co., Ltd. focuses on the R&D, production, and sale of new display device testing equipment in China with a market cap of CN¥17.38 billion.

Operations: The company's revenue primarily comes from its activities in the research, development, production, and sale of innovative display device testing equipment within China.

Insider Ownership: 18.9%

Earnings Growth Forecast: 56.5% p.a.

Shenzhen SEICHI Technologies has shown impressive revenue growth, with sales reaching CNY 753.04 million for the first nine months of 2025, up from CNY 566.2 million a year ago. However, net income declined to CNY 41.47 million from CNY 51.38 million due to lower profit margins and large one-off items affecting earnings quality. Despite high expected annual profit growth of over 20%, share price volatility remains a concern for investors seeking stability in high insider ownership companies in Asia.

- Click here and access our complete growth analysis report to understand the dynamics of Shenzhen SEICHI Technologies.

- Our valuation report here indicates Shenzhen SEICHI Technologies may be overvalued.

Make It Happen

- Explore the 638 names from our Fast Growing Asian Companies With High Insider Ownership screener here.

- Seeking Other Investments? Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Bozhon Precision Industry TechnologyLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688097

Bozhon Precision Industry TechnologyLtd

Bozhon Precision Industry Technology Co.,Ltd.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

37 followersusers have followed this narrative

6 commentsusers have commented on this narrative

10 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1918.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5190.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

114 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

952 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative