Advertisement

- China

- /

- Aerospace & Defense

- /

- SHSE:688084

Beijing Jingpin Tezhuang Technology Co.,Ltd. (SHSE:688084) Stocks Shoot Up 35% But Its P/S Still Looks Reasonable

The Beijing Jingpin Tezhuang Technology Co.,Ltd. (SHSE:688084) share price has done very well over the last month, posting an excellent gain of 35%. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 17% in the last twelve months.

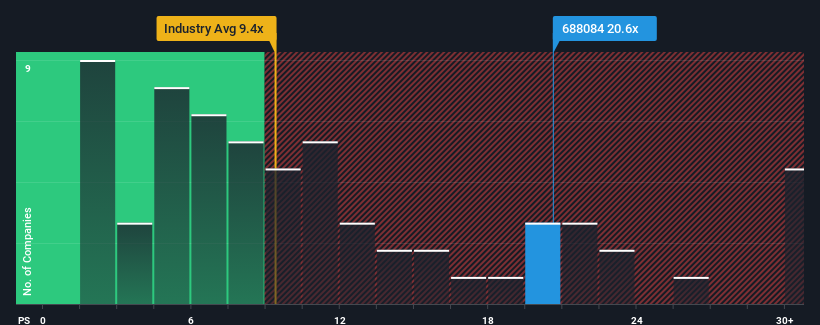

Following the firm bounce in price, you could be forgiven for thinking Beijing Jingpin Tezhuang TechnologyLtd is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 20.6x, considering almost half the companies in China's Aerospace & Defense industry have P/S ratios below 9.4x. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

Check out our latest analysis for Beijing Jingpin Tezhuang TechnologyLtd

How Beijing Jingpin Tezhuang TechnologyLtd Has Been Performing

Beijing Jingpin Tezhuang TechnologyLtd certainly has been doing a good job lately as its revenue growth has been positive while most other companies have been seeing their revenue go backwards. The P/S ratio is probably high because investors think the company will continue to navigate the broader industry headwinds better than most. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Keen to find out how analysts think Beijing Jingpin Tezhuang TechnologyLtd's future stacks up against the industry? In that case, our free report is a great place to start.Is There Enough Revenue Growth Forecasted For Beijing Jingpin Tezhuang TechnologyLtd?

Beijing Jingpin Tezhuang TechnologyLtd's P/S ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the industry.

Retrospectively, the last year delivered a decent 14% gain to the company's revenues. Ultimately though, it couldn't turn around the poor performance of the prior period, with revenue shrinking 50% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Shifting to the future, estimates from the sole analyst covering the company suggest revenue should grow by 177% over the next year. With the industry only predicted to deliver 60%, the company is positioned for a stronger revenue result.

With this information, we can see why Beijing Jingpin Tezhuang TechnologyLtd is trading at such a high P/S compared to the industry. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What We Can Learn From Beijing Jingpin Tezhuang TechnologyLtd's P/S?

The strong share price surge has lead to Beijing Jingpin Tezhuang TechnologyLtd's P/S soaring as well. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Beijing Jingpin Tezhuang TechnologyLtd maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Aerospace & Defense industry, as expected. Right now shareholders are comfortable with the P/S as they are quite confident future revenues aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

Don't forget that there may be other risks. For instance, we've identified 3 warning signs for Beijing Jingpin Tezhuang TechnologyLtd (1 doesn't sit too well with us) you should be aware of.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Beijing Jingpin Tezhuang TechnologyLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688084

Beijing Jingpin Tezhuang TechnologyLtd

Beijing Jingpin Tezhuang Technology Co.,Ltd.

Adequate balance sheet very low.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|20.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.5% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|20.5% undervalued

CH

Community Contributor