Advertisement

Beijing Worldia Diamond Tools Co.,Ltd. (SHSE:688028) Soars 26% But It's A Story Of Risk Vs Reward

Beijing Worldia Diamond Tools Co.,Ltd. (SHSE:688028) shares have continued their recent momentum with a 26% gain in the last month alone. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 12% in the last twelve months.

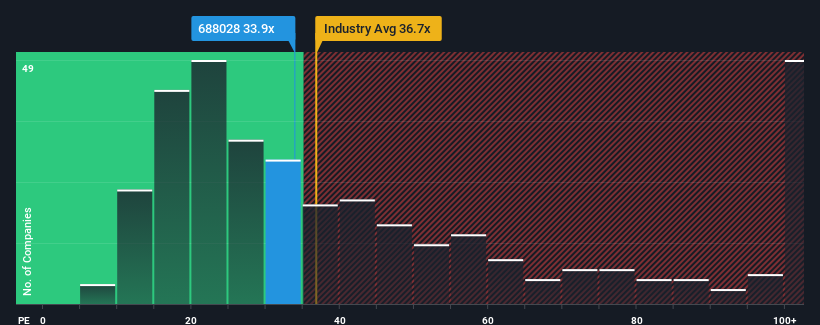

Although its price has surged higher, it's still not a stretch to say that Beijing Worldia Diamond ToolsLtd's price-to-earnings (or "P/E") ratio of 33.9x right now seems quite "middle-of-the-road" compared to the market in China, where the median P/E ratio is around 37x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

Recent times haven't been advantageous for Beijing Worldia Diamond ToolsLtd as its earnings have been falling quicker than most other companies. One possibility is that the P/E is moderate because investors think the company's earnings trend will eventually fall in line with most others in the market. If you still like the company, you'd want its earnings trajectory to turn around before making any decisions. If not, then existing shareholders may be a little nervous about the viability of the share price.

View our latest analysis for Beijing Worldia Diamond ToolsLtd

What Are Growth Metrics Telling Us About The P/E?

There's an inherent assumption that a company should be matching the market for P/E ratios like Beijing Worldia Diamond ToolsLtd's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 4.2% decrease to the company's bottom line. This has soured the latest three-year period, which nevertheless managed to deliver a decent 27% overall rise in EPS. So we can start by confirming that the company has generally done a good job of growing earnings over that time, even though it had some hiccups along the way.

Turning to the outlook, the next year should generate growth of 62% as estimated by the one analyst watching the company. Meanwhile, the rest of the market is forecast to only expand by 39%, which is noticeably less attractive.

In light of this, it's curious that Beijing Worldia Diamond ToolsLtd's P/E sits in line with the majority of other companies. Apparently some shareholders are skeptical of the forecasts and have been accepting lower selling prices.

The Bottom Line On Beijing Worldia Diamond ToolsLtd's P/E

Its shares have lifted substantially and now Beijing Worldia Diamond ToolsLtd's P/E is also back up to the market median. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of Beijing Worldia Diamond ToolsLtd's analyst forecasts revealed that its superior earnings outlook isn't contributing to its P/E as much as we would have predicted. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing pressure on the P/E ratio. At least the risk of a price drop looks to be subdued, but investors seem to think future earnings could see some volatility.

You should always think about risks. Case in point, we've spotted 1 warning sign for Beijing Worldia Diamond ToolsLtd you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're here to simplify it.

Discover if Beijing Worldia Diamond ToolsLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688028

Beijing Worldia Diamond ToolsLtd

Engages in the research and development, production, and sale of high precision diamond cutting tools in China and internationally.

Excellent balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|20.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.5% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|20.5% undervalued

CH

Community Contributor