- Japan

- /

- Trade Distributors

- /

- TSE:9960

Undiscovered Gems with Strong Fundamentals for November 2024

Reviewed by Simply Wall St

As global markets navigate a challenging landscape marked by mixed economic signals and cautious investor sentiment, small-cap stocks have shown resilience, holding up better than their large-cap counterparts despite a busy earnings season. In this environment, uncovering stocks with strong fundamentals becomes crucial for investors seeking opportunities that can weather volatility and capitalize on potential growth.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Techno Smart | NA | 6.07% | -0.57% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Industrias del Cobre Sociedad Anónima | NA | 19.63% | 22.92% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Compañía Electro Metalúrgica | 72.83% | 12.17% | 19.18% | ★★★★☆☆ |

| Hermes Transportes Blindados | 58.80% | 4.29% | 2.04% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Al Wathba National Insurance Company PJSC | 14.56% | 13.48% | 31.31% | ★★★★☆☆ |

We'll examine a selection from our screener results.

Runner (Xiamen) (SHSE:603408)

Simply Wall St Value Rating: ★★★★★★

Overview: Runner (Xiamen) Corp. focuses on the research and development, design, production, and sale of kitchen and bathroom products as well as water purification products both in China and internationally, with a market cap of CN¥5.96 billion.

Operations: Runner (Xiamen) generates revenue primarily through the sale of kitchen and bathroom products, along with water purification products. The company shows a gross profit margin trend worth noting, which has fluctuated between 30% and 35% over recent periods.

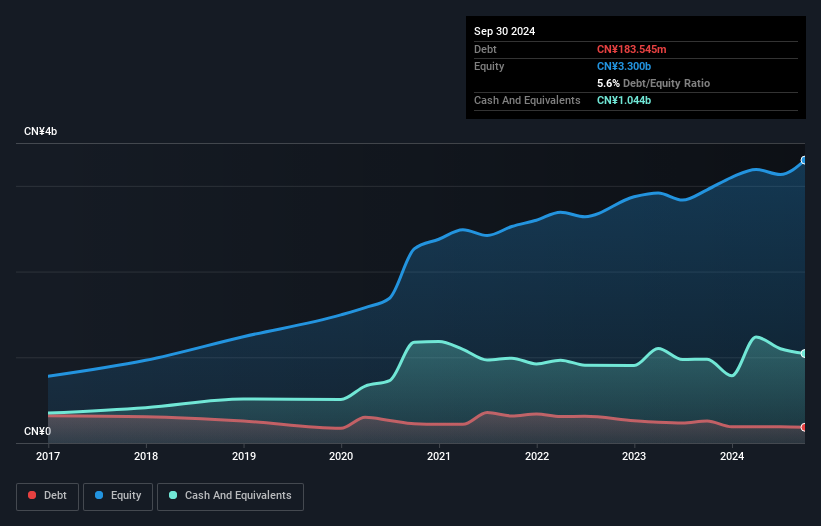

Runner Corp. has shown impressive growth, with earnings increasing by 35.9% over the past year, outpacing the building industry’s -8%. Their debt-to-equity ratio improved significantly from 13.5% to 5.6% over five years, highlighting effective financial management. Runner's sales for the nine months ending September 2024 reached CNY 3.78 billion, up from CNY 3.09 billion a year earlier, while net income rose to CNY 396.6 million from CNY 290.2 million in the previous period, reflecting strong operational performance and high-quality earnings that are expected to grow at a rate of about 13.87% annually moving forward.

- Dive into the specifics of Runner (Xiamen) here with our thorough health report.

Assess Runner (Xiamen)'s past performance with our detailed historical performance reports.

Guangzhou Ruoyuchen TechnologyLtd (SZSE:003010)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Guangzhou Ruoyuchen Technology Co., Ltd. specializes in offering brand integrated marketing solutions within China and has a market capitalization of CN¥2.67 billion.

Operations: Ruoyuchen Technology generates revenue primarily from the e-commerce service industry, amounting to CN¥1.56 billion.

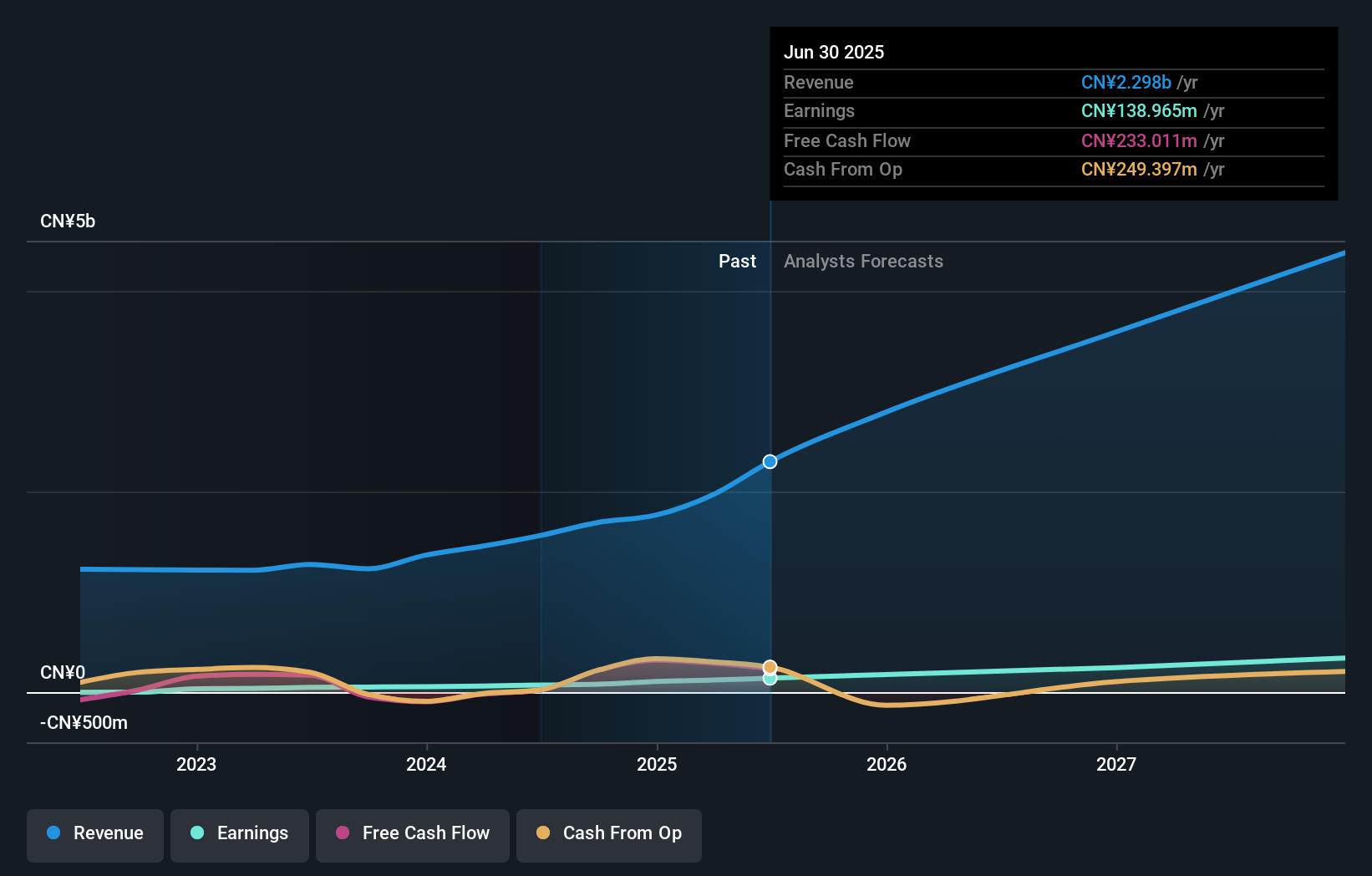

Guangzhou Ruoyuchen Technology, a nimble player in its sector, has shown impressive strides with earnings jumping 49.7% over the past year, outpacing the Consumer Retailing industry’s 6% growth. For the first nine months of 2024, sales reached CNY 1.15 billion from CNY 828.76 million last year, while net income climbed to CNY 57.7 million from CNY 33.73 million previously. Basic earnings per share improved to CNY 0.3532 compared to last year's CNY 0.1974, showcasing robust financial health and potential for continued success amidst recent executive changes and bylaw amendments approved in September.

Totech (TSE:9960)

Simply Wall St Value Rating: ★★★★★★

Overview: Totech Corporation operates in Japan, focusing on the sale of environment control equipment, with a market capitalization of ¥111.65 billion.

Operations: Totech generates revenue primarily through its Merchandise Sales Business and Construction Business, with figures of ¥86.59 billion and ¥60.60 billion, respectively.

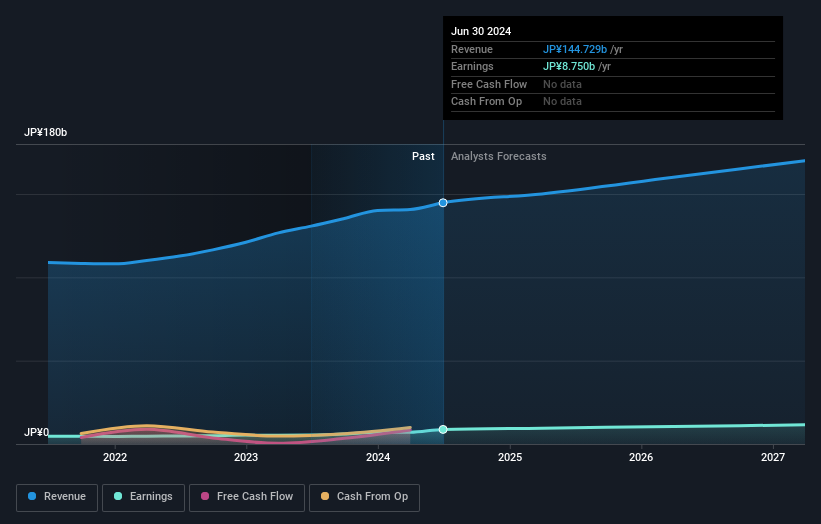

Totech stands out with its robust earnings, having grown by 63.8% in the past year, outpacing the Trade Distributors industry average of 5.3%. Its debt to equity ratio has impressively decreased from 98.4% to 16.9% over five years, reflecting prudent financial management. The company is trading at a discount of 16.8% below its estimated fair value, suggesting potential undervaluation in the market. Looking ahead, Totech anticipates net sales of ¥146 billion and an operating profit of ¥10.5 billion for the fiscal year ending March 2025, indicating positive growth momentum and solid future prospects.

- Unlock comprehensive insights into our analysis of Totech stock in this health report.

Evaluate Totech's historical performance by accessing our past performance report.

Next Steps

- Navigate through the entire inventory of 4726 Undiscovered Gems With Strong Fundamentals here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Totech might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:9960

Flawless balance sheet with solid track record and pays a dividend.