Advertisement

Does Zhuzhou Kibing GroupLtd (SHSE:601636) Have A Healthy Balance Sheet?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Zhuzhou Kibing Group Co.,Ltd (SHSE:601636) does carry debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Zhuzhou Kibing GroupLtd

What Is Zhuzhou Kibing GroupLtd's Net Debt?

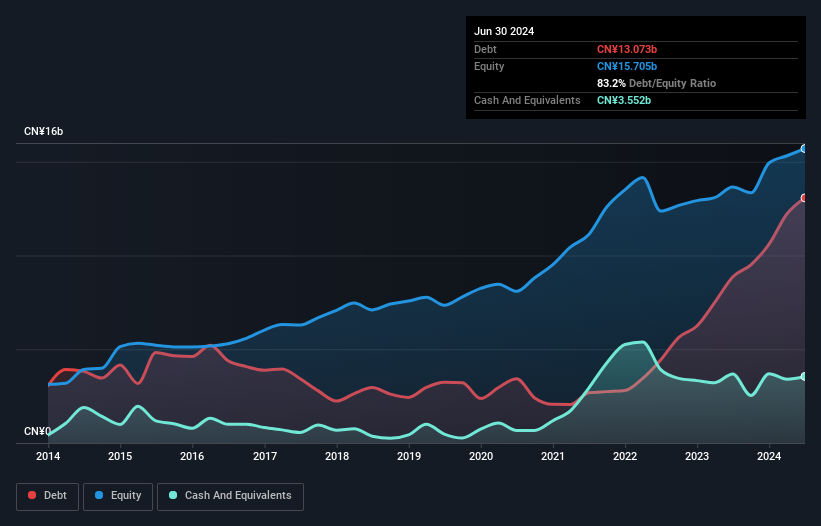

As you can see below, at the end of June 2024, Zhuzhou Kibing GroupLtd had CN¥13.1b of debt, up from CN¥8.86b a year ago. Click the image for more detail. However, it also had CN¥3.55b in cash, and so its net debt is CN¥9.52b.

How Strong Is Zhuzhou Kibing GroupLtd's Balance Sheet?

The latest balance sheet data shows that Zhuzhou Kibing GroupLtd had liabilities of CN¥7.89b due within a year, and liabilities of CN¥11.4b falling due after that. On the other hand, it had cash of CN¥3.55b and CN¥2.34b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥13.4b.

This is a mountain of leverage relative to its market capitalization of CN¥15.3b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Zhuzhou Kibing GroupLtd has a debt to EBITDA ratio of 2.6, which signals significant debt, but is still pretty reasonable for most types of business. However, its interest coverage of 10.8 is very high, suggesting that the interest expense on the debt is currently quite low. Notably, Zhuzhou Kibing GroupLtd's EBIT launched higher than Elon Musk, gaining a whopping 165% on last year. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Zhuzhou Kibing GroupLtd can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Over the last three years, Zhuzhou Kibing GroupLtd saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

We feel some trepidation about Zhuzhou Kibing GroupLtd's difficulty conversion of EBIT to free cash flow, but we've got positives to focus on, too. For example, its EBIT growth rate and interest cover give us some confidence in its ability to manage its debt. Taking the abovementioned factors together we do think Zhuzhou Kibing GroupLtd's debt poses some risks to the business. So while that leverage does boost returns on equity, we wouldn't really want to see it increase from here. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. To that end, you should learn about the 3 warning signs we've spotted with Zhuzhou Kibing GroupLtd (including 2 which don't sit too well with us) .

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Zhuzhou Kibing GroupLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:601636

Zhuzhou Kibing GroupLtd

Manufactures and sells glass in China and internationally.

Slight risk and fair value.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|30.4% undervalued

MA

Community Contributor

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.0% undervalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|20.4% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor