Advertisement

Does Shanghai Highly (Group) (SHSE:600619) Have A Healthy Balance Sheet?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Shanghai Highly (Group) Co., Ltd. (SHSE:600619) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Shanghai Highly (Group)

What Is Shanghai Highly (Group)'s Debt?

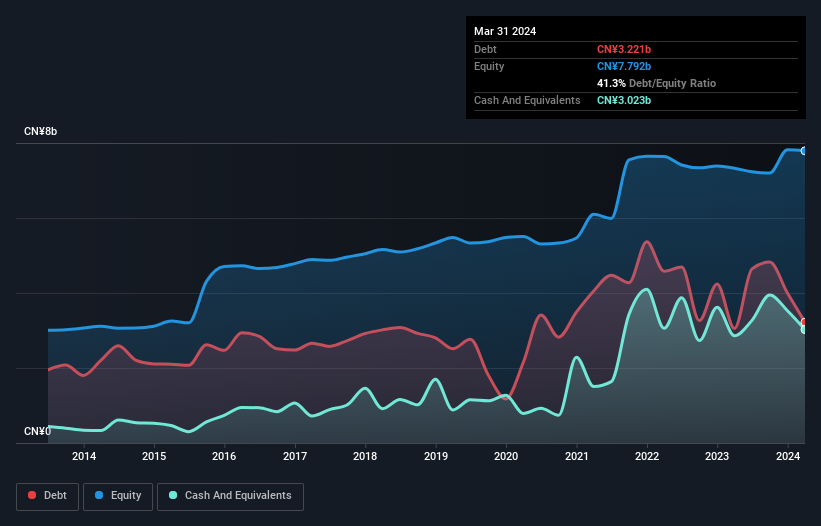

The image below, which you can click on for greater detail, shows that at March 2024 Shanghai Highly (Group) had debt of CN¥3.22b, up from CN¥3.05b in one year. However, it does have CN¥3.02b in cash offsetting this, leading to net debt of about CN¥197.5m.

A Look At Shanghai Highly (Group)'s Liabilities

According to the last reported balance sheet, Shanghai Highly (Group) had liabilities of CN¥10.7b due within 12 months, and liabilities of CN¥2.58b due beyond 12 months. Offsetting these obligations, it had cash of CN¥3.02b as well as receivables valued at CN¥6.53b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥3.76b.

This deficit is considerable relative to its market capitalization of CN¥4.86b, so it does suggest shareholders should keep an eye on Shanghai Highly (Group)'s use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Given net debt is only 0.31 times EBITDA, it is initially surprising to see that Shanghai Highly (Group)'s EBIT has low interest coverage of 0.18 times. So while we're not necessarily alarmed we think that its debt is far from trivial. Notably, Shanghai Highly (Group) made a loss at the EBIT level, last year, but improved that to positive EBIT of CN¥18m in the last twelve months. When analysing debt levels, the balance sheet is the obvious place to start. But it is Shanghai Highly (Group)'s earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it is important to check how much of its earnings before interest and tax (EBIT) converts to actual free cash flow. Happily for any shareholders, Shanghai Highly (Group) actually produced more free cash flow than EBIT over the last year. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

Shanghai Highly (Group)'s interest cover was a real negative on this analysis, although the other factors we considered were considerably better. In particular, we are dazzled with its conversion of EBIT to free cash flow. When we consider all the factors mentioned above, we do feel a bit cautious about Shanghai Highly (Group)'s use of debt. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example Shanghai Highly (Group) has 2 warning signs (and 1 which makes us a bit uncomfortable) we think you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600619

Shanghai Highly (Group)

Researches, develops, manufactures, and sells components for white goods and energy vehicles in China and internationally.

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|36.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.0% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|46.4% overvalued

DA

Community Contributor