- China

- /

- Electrical

- /

- SHSE:600522

Jiangsu Zhongtian Technology Co., Ltd.'s (SHSE:600522) Price Is Right But Growth Is Lacking After Shares Rocket 25%

Jiangsu Zhongtian Technology Co., Ltd. (SHSE:600522) shareholders have had their patience rewarded with a 25% share price jump in the last month. Longer-term shareholders would be thankful for the recovery in the share price since it's now virtually flat for the year after the recent bounce.

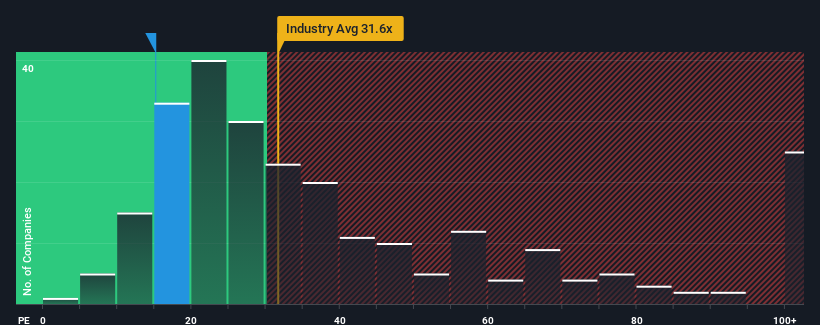

Even after such a large jump in price, given about half the companies in China have price-to-earnings ratios (or "P/E's") above 32x, you may still consider Jiangsu Zhongtian Technology as a highly attractive investment with its 15.1x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

With earnings growth that's superior to most other companies of late, Jiangsu Zhongtian Technology has been doing relatively well. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

See our latest analysis for Jiangsu Zhongtian Technology

How Is Jiangsu Zhongtian Technology's Growth Trending?

Jiangsu Zhongtian Technology's P/E ratio would be typical for a company that's expected to deliver very poor growth or even falling earnings, and importantly, perform much worse than the market.

Retrospectively, the last year delivered an exceptional 54% gain to the company's bottom line. The strong recent performance means it was also able to grow EPS by 43% in total over the last three years. So we can start by confirming that the company has done a great job of growing earnings over that time.

Turning to the outlook, the next year should generate growth of 22% as estimated by the analysts watching the company. That's shaping up to be materially lower than the 41% growth forecast for the broader market.

With this information, we can see why Jiangsu Zhongtian Technology is trading at a P/E lower than the market. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

What We Can Learn From Jiangsu Zhongtian Technology's P/E?

Shares in Jiangsu Zhongtian Technology are going to need a lot more upward momentum to get the company's P/E out of its slump. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Jiangsu Zhongtian Technology maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

A lot of potential risks can sit within a company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Jiangsu Zhongtian Technology with six simple checks.

You might be able to find a better investment than Jiangsu Zhongtian Technology. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600522

Jiangsu Zhongtian Technology

Produces and sells electrical machinery and equipment for the communications, electric power, marine, new energy, marine engineering construction, and other business sectors in China and internationally.

Very undervalued with flawless balance sheet and pays a dividend.

Market Insights

Community Narratives