- Hong Kong

- /

- Real Estate

- /

- SEHK:1995

Top Dividend Stocks To Consider In February 2025

Reviewed by Simply Wall St

As global markets navigate a landscape marked by tariff uncertainties and mixed economic signals, investors are increasingly seeking stability amidst volatility. With U.S. job growth cooling and manufacturing showing signs of recovery, dividend stocks can offer a reliable income stream, making them an attractive option for those looking to balance risk with potential returns in these fluctuating times.

Top 10 Dividend Stocks

| Name | Dividend Yield | Dividend Rating |

| Guaranty Trust Holding (NGSE:GTCO) | 5.87% | ★★★★★★ |

| Wuliangye YibinLtd (SZSE:000858) | 4.03% | ★★★★★★ |

| Padma Oil (DSE:PADMAOIL) | 7.55% | ★★★★★★ |

| Peoples Bancorp (NasdaqGS:PEBO) | 4.79% | ★★★★★★ |

| Tsubakimoto Chain (TSE:6371) | 4.28% | ★★★★★★ |

| Daito Trust ConstructionLtd (TSE:1878) | 4.04% | ★★★★★★ |

| GakkyushaLtd (TSE:9769) | 4.51% | ★★★★★★ |

| CAC Holdings (TSE:4725) | 4.46% | ★★★★★★ |

| Citizens & Northern (NasdaqCM:CZNC) | 5.11% | ★★★★★★ |

| Nihon Parkerizing (TSE:4095) | 3.99% | ★★★★★★ |

Click here to see the full list of 1964 stocks from our Top Dividend Stocks screener.

Here we highlight a subset of our preferred stocks from the screener.

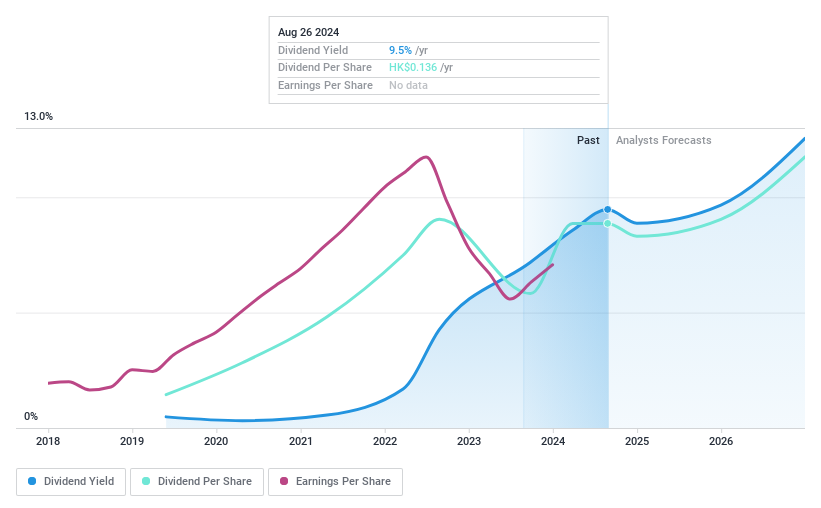

Ever Sunshine Services Group (SEHK:1995)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Ever Sunshine Services Group Limited is an investment holding company offering property management services in the People's Republic of China, with a market cap of HK$3.13 billion.

Operations: The company's revenue segment is primarily derived from Property Management Services, amounting to CN¥6.72 billion.

Dividend Yield: 8.9%

Ever Sunshine Services Group's dividend yield is in the top 25% of Hong Kong payers, with a payout ratio of 60.9%, indicating dividends are covered by earnings. However, its dividend history is volatile and has been inconsistent over six years. Despite this, the cash payout ratio of 31.7% suggests dividends are well-covered by cash flows. The company's stock trades significantly below estimated fair value, but investors should consider its unstable dividend track record.

- Get an in-depth perspective on Ever Sunshine Services Group's performance by reading our dividend report here.

- In light of our recent valuation report, it seems possible that Ever Sunshine Services Group is trading behind its estimated value.

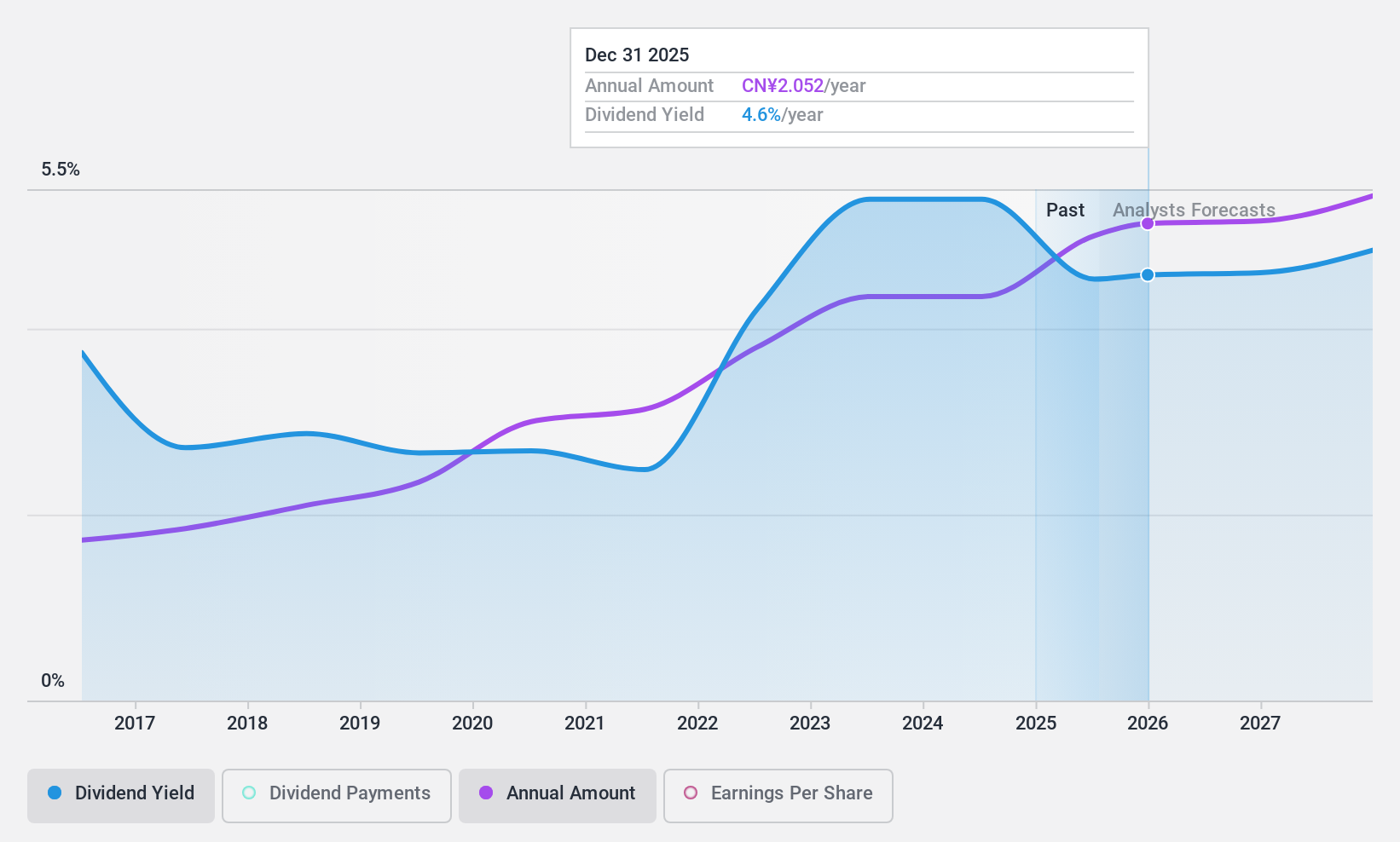

China Merchants Bank (SHSE:600036)

Simply Wall St Dividend Rating: ★★★★★★

Overview: China Merchants Bank Co., Ltd., along with its subsidiaries, offers a range of banking products and services and has a market cap of CN¥1.03 trillion.

Operations: Unfortunately, the provided text does not include specific revenue segment data for China Merchants Bank Co., Ltd. If you have additional information regarding their revenue segments, I can help summarize it for you.

Dividend Yield: 4.7%

China Merchants Bank's dividend yield is among the top 25% in China, with a stable history over the past decade. The payout ratio of 35.2% indicates dividends are well-covered by earnings, and this coverage is expected to improve to 29.8% in three years. Despite trading at a significant discount to estimated fair value, recent board changes and M&A activity may influence future performance considerations for dividend investors.

- Delve into the full analysis dividend report here for a deeper understanding of China Merchants Bank.

- Insights from our recent valuation report point to the potential overvaluation of China Merchants Bank shares in the market.

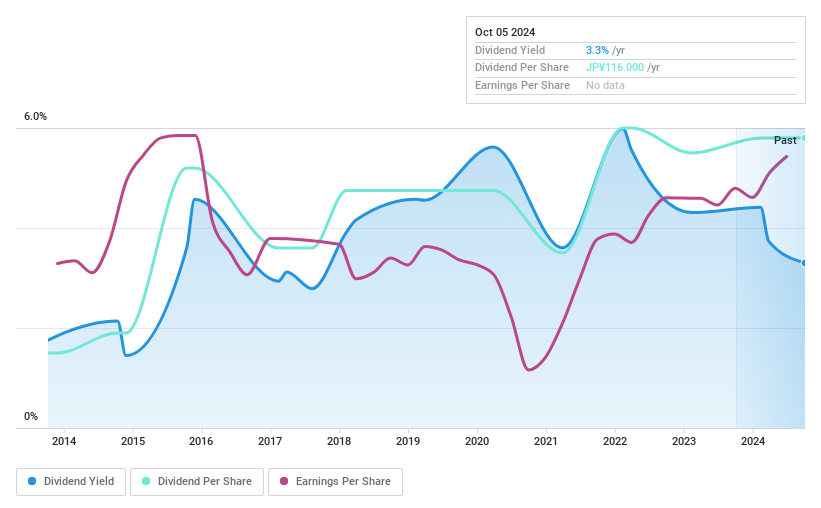

Chiyoda IntegreLtd (TSE:6915)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Chiyoda Integre Co., Ltd. manufactures and sells structural and functional parts for various products in Japan and internationally, with a market cap of ¥28.18 billion.

Operations: Chiyoda Integre Ltd. generates revenue from the manufacturing and sale of structural and functional components for a variety of products both domestically in Japan and internationally.

Dividend Yield: 4%

Chiyoda Integre Ltd. offers a dividend yield in the top 25% of the Japanese market, supported by a payout ratio of 43.4%, indicating dividends are well-covered by earnings and cash flows. However, its dividend history is unstable with volatility over the past decade. Recent share buybacks totaling ¥357.01 million may enhance shareholder returns but do not mitigate concerns about dividend reliability despite ongoing profit growth and trading below estimated fair value.

- Click here and access our complete dividend analysis report to understand the dynamics of Chiyoda IntegreLtd.

- The valuation report we've compiled suggests that Chiyoda IntegreLtd's current price could be quite moderate.

Key Takeaways

- Click through to start exploring the rest of the 1961 Top Dividend Stocks now.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Ever Sunshine Services Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1995

Ever Sunshine Services Group

An investment holding company, provides property management services in the People's Republic of China.

Flawless balance sheet with solid track record and pays a dividend.

Market Insights

Community Narratives