3 Asian Growth Companies With High Insider Ownership Growing Earnings At 64%

Reviewed by Simply Wall St

As global markets navigate economic uncertainty and inflation concerns, the Asian market presents a unique opportunity for investors seeking growth amidst volatility. In this environment, companies with high insider ownership and strong earnings growth can offer a compelling investment case, as they often demonstrate alignment of interests between management and shareholders.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Zhejiang Jolly PharmaceuticalLTD (SZSE:300181) | 23.3% | 26% |

| AcrelLtd (SZSE:300286) | 40% | 32% |

| Seojin SystemLtd (KOSDAQ:A178320) | 32.1% | 39.3% |

| Laopu Gold (SEHK:6181) | 36.4% | 47.2% |

| Global Tax Free (KOSDAQ:A204620) | 21.8% | 89.3% |

| Oscotec (KOSDAQ:A039200) | 21.3% | 85.9% |

| UTour Group (SZSE:002707) | 23.5% | 32.7% |

| Fulin Precision (SZSE:300432) | 13.6% | 78.6% |

| Synspective (TSE:290A) | 13.2% | 37.4% |

| Ascentage Pharma Group International (SEHK:6855) | 17.9% | 83.6% |

Below we spotlight a couple of our favorites from our exclusive screener.

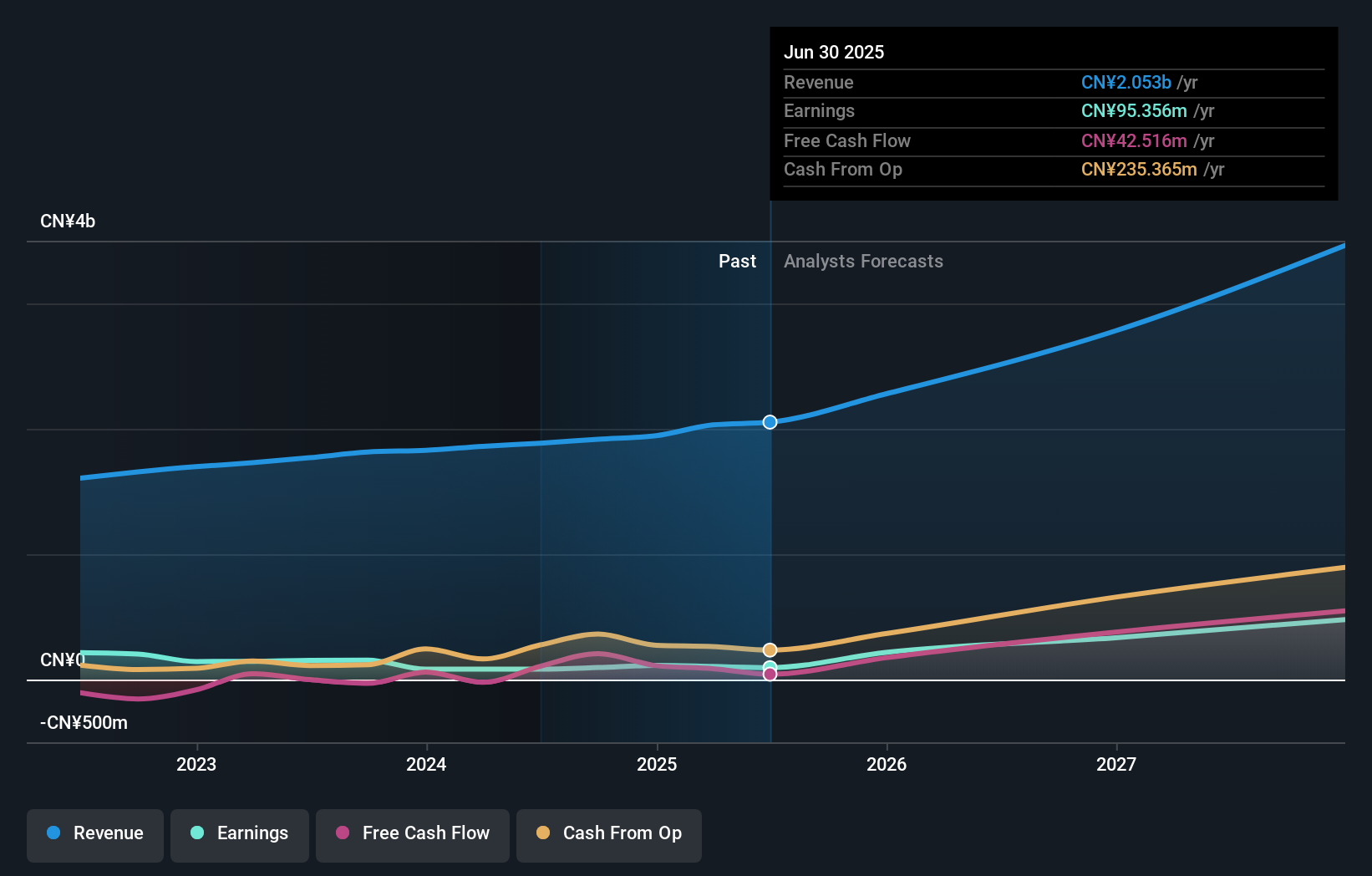

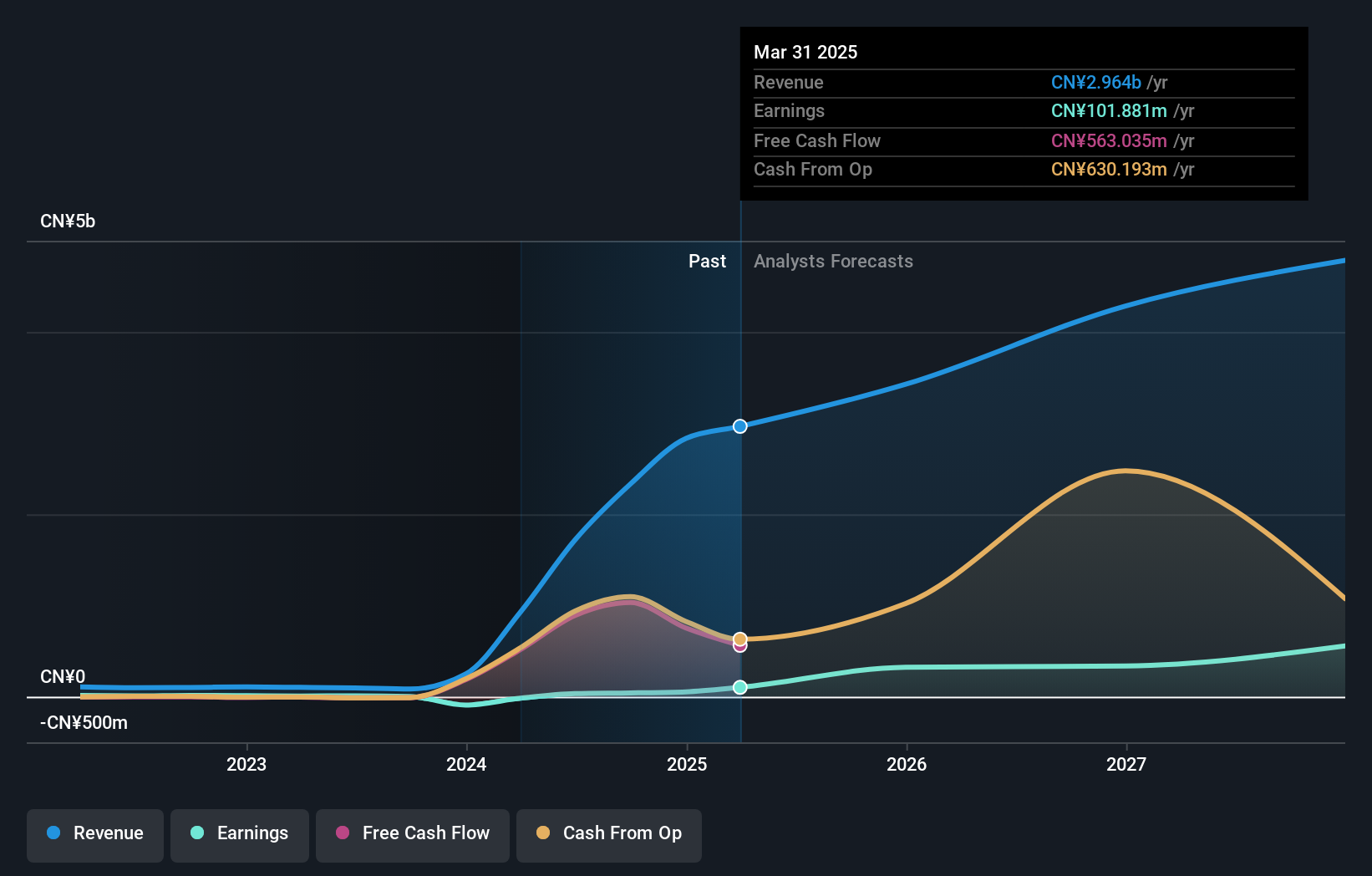

Servyou Software Group (SHSE:603171)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Servyou Software Group Co., Ltd. operates in China, offering financial and tax information services, with a market cap of CN¥18.53 billion.

Operations: Servyou Software Group Co., Ltd. generates its revenue primarily from financial and tax information services in China.

Insider Ownership: 22.7%

Earnings Growth Forecast: 57.5% p.a.

Servyou Software Group exhibits a compelling growth trajectory with earnings projected to increase by 57.48% annually, outpacing the broader Chinese market's 24.8%. However, profit margins have declined from 8.6% to 5%, and the share price has been highly volatile recently. The company trades at a discount of approximately 17.7% below its estimated fair value, but insider trading activity remains low over the past three months.

- Navigate through the intricacies of Servyou Software Group with our comprehensive analyst estimates report here.

- Insights from our recent valuation report point to the potential overvaluation of Servyou Software Group shares in the market.

Huatu Cendes (SZSE:300492)

Simply Wall St Growth Rating: ★★★★★★

Overview: Huatu Cendes Co., Ltd. is an architectural design company offering professional design, consulting, and engineering services to a diverse clientele in China, with a market cap of CN¥12.53 billion.

Operations: Huatu Cendes generates revenue through its provision of architectural design, consulting, and engineering services to a wide range of clients including state-owned enterprises, multinational corporations, private companies, and government agencies in China.

Insider Ownership: 19.4%

Earnings Growth Forecast: 64.6% p.a.

Huatu Cendes is poised for significant growth, with earnings expected to rise by 64.58% annually, surpassing the Chinese market's average. Revenue is also projected to increase at 22.5% per year, outpacing market expectations. The company's Return on Equity is forecasted to be very high in three years at 44.8%. While there has been no substantial insider trading recently, the company maintains a robust financial outlook with consistent dividend payments approved for early 2025.

- Delve into the full analysis future growth report here for a deeper understanding of Huatu Cendes.

- The valuation report we've compiled suggests that Huatu Cendes' current price could be inflated.

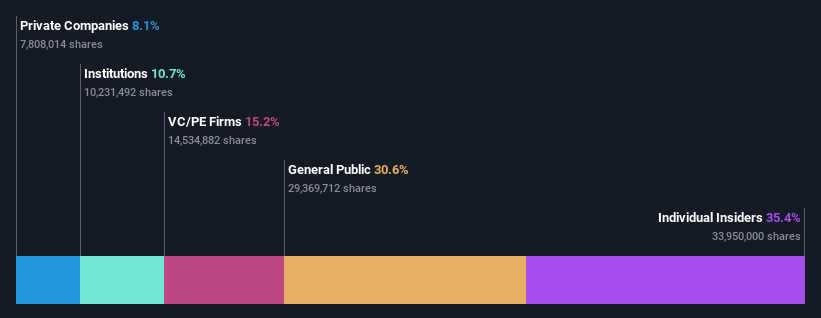

Alnera Aluminium (SZSE:301613)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Alnera Aluminium Co., Ltd. focuses on the R&D, production, and sale of aluminum alloy parts for new energy vehicle battery systems, with a market cap of CN¥7.11 billion.

Operations: Alnera Aluminium Co., Ltd. generates revenue through its involvement in the research, development, production, and sale of aluminum alloy components specifically designed for battery systems in new energy vehicles.

Insider Ownership: 35.4%

Earnings Growth Forecast: 33.1% p.a.

Alnera Aluminium is positioned for strong growth, with revenue forecasted to increase by 26.6% annually, exceeding the Chinese market's average. Earnings are expected to grow significantly at 33.1% per year. Despite having a Price-To-Earnings ratio slightly below the market average, its financial health is challenged by debt not well covered by operating cash flow. Recent private placement plans aim to issue A shares, pending regulatory approvals, potentially impacting insider ownership dynamics positively.

- Click here and access our complete growth analysis report to understand the dynamics of Alnera Aluminium.

- The analysis detailed in our Alnera Aluminium valuation report hints at an inflated share price compared to its estimated value.

Make It Happen

- Explore the 658 names from our Fast Growing Asian Companies With High Insider Ownership screener here.

- Ready To Venture Into Other Investment Styles? Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:603171

Servyou Software Group

Provides financial and tax information services in China.

High growth potential with excellent balance sheet.

Market Insights

Community Narratives