- Japan

- /

- Electrical

- /

- TSE:6507

Hebei Keli Automobile Equipment And 2 Other Undiscovered Gems For Your Portfolio

Reviewed by Simply Wall St

As global markets continue to reach new heights, small-cap stocks are finally joining their larger peers in record territory, with the Russell 2000 Index hitting an intraday high. Amidst this backdrop of robust market sentiment, fueled by domestic policy shifts and geopolitical developments, investors might find opportunities in lesser-known companies that could offer unique growth potential. In this context, identifying undiscovered gems like Hebei Keli Automobile Equipment can be crucial for diversifying a portfolio and capitalizing on emerging market trends.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Morris State Bancshares | 17.84% | 4.83% | 6.58% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Parker Drilling | 46.05% | 0.86% | 52.25% | ★★★★★★ |

| First Northern Community Bancorp | NA | 7.65% | 11.17% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Arab Banking Corporation (B.S.C.) | 213.15% | 18.58% | 29.63% | ★★★★☆☆ |

| Invest Bank | 135.69% | 11.07% | 18.67% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Krom Bank Indonesia | NA | 40.04% | 35.44% | ★★★★☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

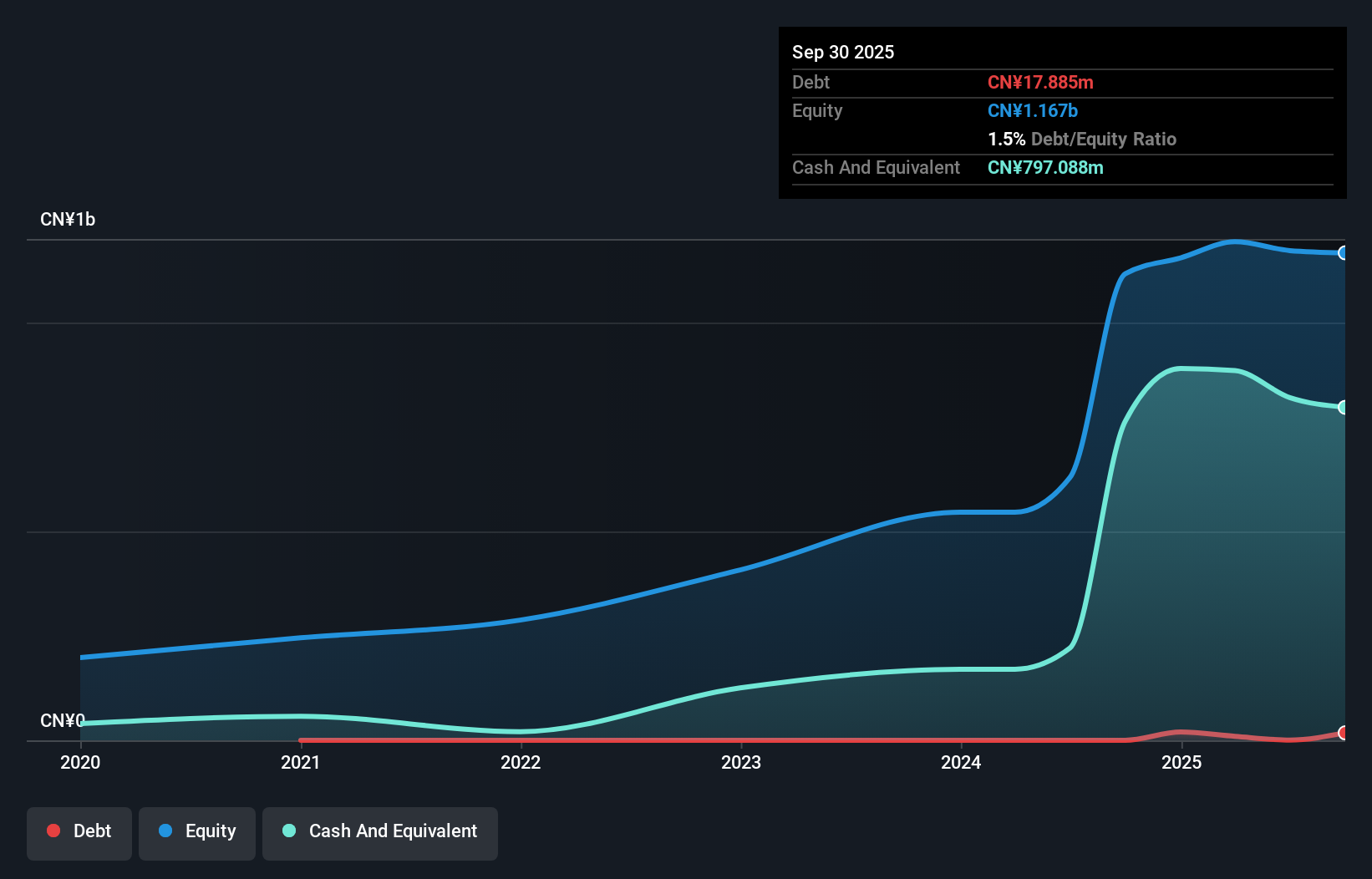

Hebei Keli Automobile Equipment (SZSE:301552)

Simply Wall St Value Rating: ★★★★★★

Overview: Hebei Keli Automobile Equipment Co., Ltd. specializes in the production of auto parts and accessories, with a market cap of CN¥3.92 billion.

Operations: The company generates revenue primarily from its auto parts and accessories segment, totaling CN¥590.95 million.

Hebei Keli, a nimble player in the auto components sector, showcases a compelling profile with its earnings growing by 19% over the past year, outpacing the industry average of 10.5%. The company reported sales of CNY 443.94 million for the first nine months of 2024, up from CNY 340.74 million last year, while net income rose to CNY 114.97 million from CNY 94.79 million. Trading at an attractive valuation—39% below estimated fair value—and boasting high-quality earnings without debt concerns over five years, it seems well-positioned despite recent share price volatility.

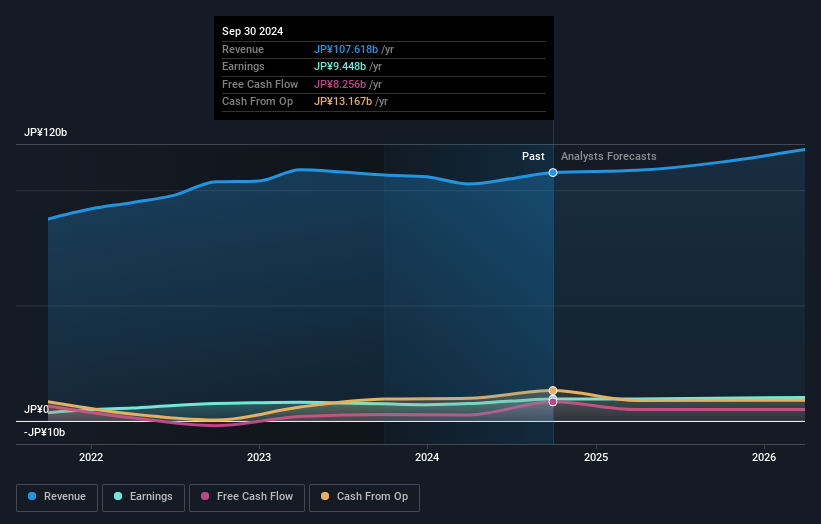

Sinfonia TechnologyLtd (TSE:6507)

Simply Wall St Value Rating: ★★★★★★

Overview: Sinfonia Technology Co., Ltd. is a company that focuses on the manufacturing and sale of various equipment, with a market capitalization of ¥170.69 billion.

Operations: Sinfonia Technology generates revenue primarily through its Motion Equipment segment, contributing ¥38.58 billion, followed by the Engineer Ring & Service and Power Electronics Equipment segments at ¥26.97 billion and ¥25.54 billion, respectively. The Clean Conveyance System adds another ¥22.93 billion to the revenue stream.

Sinfonia Technology, a smaller player in the electrical sector, has shown impressive financial health with earnings growing by 27.9% over the past year, outpacing the industry's 11.6%. The company appears to manage its debt well, reducing its debt to equity ratio from 53.5% to 23.9% over five years and maintaining a satisfactory level at 13.2%. With high-quality past earnings and positive free cash flow, Sinfonia seems well-positioned for steady growth as it forecasts an annual earnings increase of around 5.46%, suggesting potential resilience despite recent share price volatility.

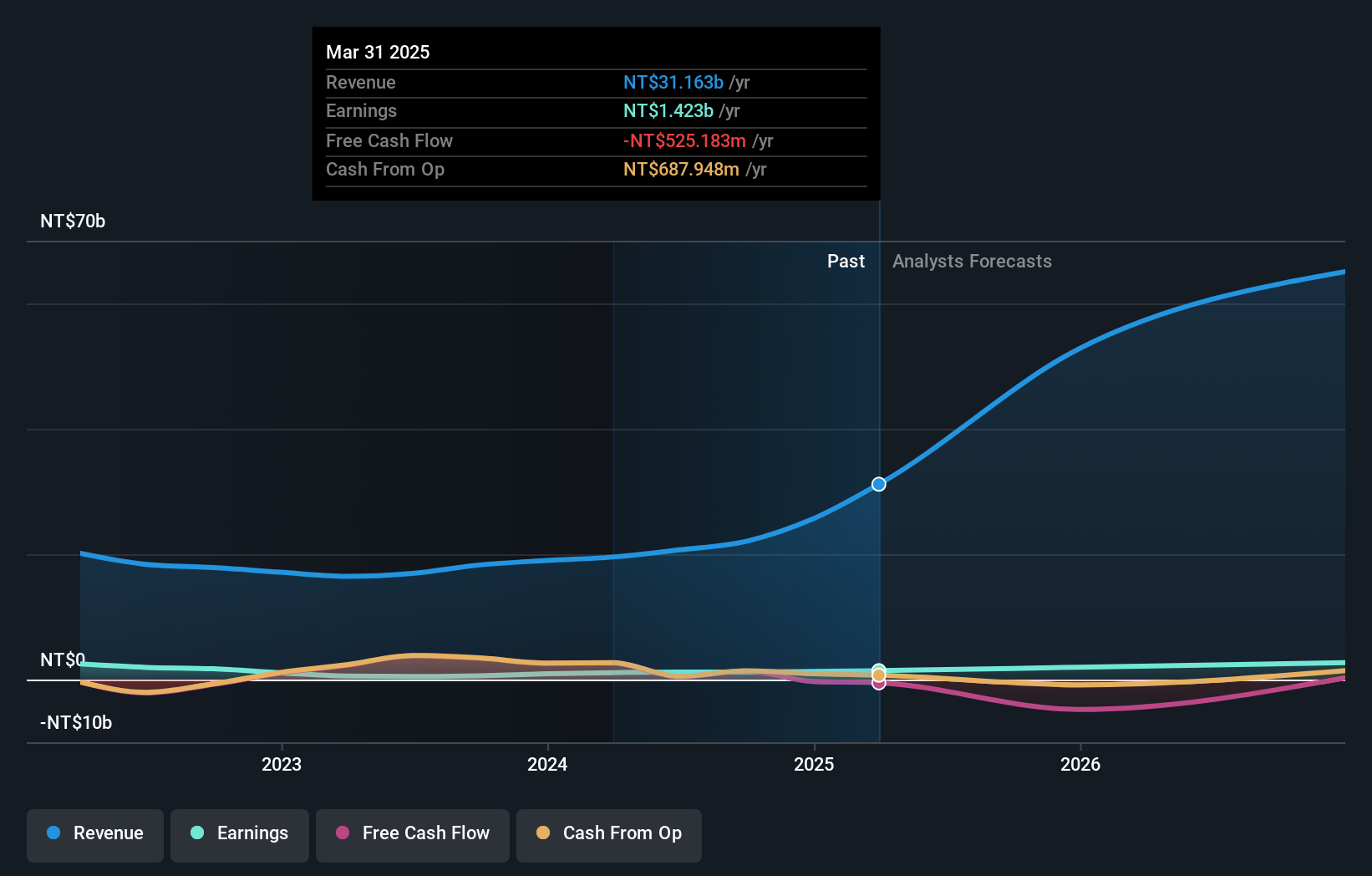

ASROCK Incorporation (TWSE:3515)

Simply Wall St Value Rating: ★★★★★★

Overview: ASROCK Incorporation designs, develops, and sells motherboards in Taiwan with a market capitalization of NT$30.28 billion.

Operations: The company generates revenue primarily from the sale of motherboards and related products, amounting to NT$22.05 billion.

ASROCK Incorporation, a tech player with significant growth potential, has seen its earnings surge by 95.8% over the past year, outpacing the broader tech industry's 10%. The firm remains debt-free and boasts high-quality earnings, positioning it well for future expansion. Recent board changes and the establishment of an Audit Committee reflect strategic governance improvements. For Q3 2024, ASROCK reported sales of TWD 6.27 billion compared to TWD 4.90 billion last year, while net income was slightly lower at TWD 305 million from TWD 309 million previously. Earnings per share stood at TWD 2.5 versus last year's TWD 2.53.

- Dive into the specifics of ASROCK Incorporation here with our thorough health report.

Explore historical data to track ASROCK Incorporation's performance over time in our Past section.

Seize The Opportunity

- Navigate through the entire inventory of 4638 Undiscovered Gems With Strong Fundamentals here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6507

Flawless balance sheet with solid track record.