Advertisement

With A 25% Price Drop For BAIC BluePark New Energy Technology Co.,Ltd. (SHSE:600733) You'll Still Get What You Pay For

The BAIC BluePark New Energy Technology Co.,Ltd. (SHSE:600733) share price has softened a substantial 25% over the previous 30 days, handing back much of the gains the stock has made lately. Looking at the bigger picture, even after this poor month the stock is up 39% in the last year.

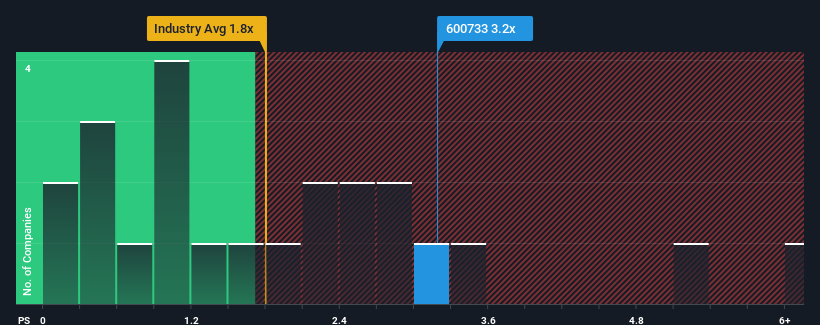

Even after such a large drop in price, given close to half the companies operating in China's Auto industry have price-to-sales ratios (or "P/S") below 1.8x, you may still consider BAIC BluePark New Energy TechnologyLtd as a stock to potentially avoid with its 3.2x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

See our latest analysis for BAIC BluePark New Energy TechnologyLtd

How Has BAIC BluePark New Energy TechnologyLtd Performed Recently?

Recent times have been advantageous for BAIC BluePark New Energy TechnologyLtd as its revenues have been rising faster than most other companies. It seems that many are expecting the strong revenue performance to persist, which has raised the P/S. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on BAIC BluePark New Energy TechnologyLtd.How Is BAIC BluePark New Energy TechnologyLtd's Revenue Growth Trending?

In order to justify its P/S ratio, BAIC BluePark New Energy TechnologyLtd would need to produce impressive growth in excess of the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 30%. Pleasingly, revenue has also lifted 200% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing revenue over that time.

Looking ahead now, revenue is anticipated to climb by 73% each year during the coming three years according to the four analysts following the company. That's shaping up to be materially higher than the 31% each year growth forecast for the broader industry.

With this information, we can see why BAIC BluePark New Energy TechnologyLtd is trading at such a high P/S compared to the industry. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Bottom Line On BAIC BluePark New Energy TechnologyLtd's P/S

There's still some elevation in BAIC BluePark New Energy TechnologyLtd's P/S, even if the same can't be said for its share price recently. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Our look into BAIC BluePark New Energy TechnologyLtd shows that its P/S ratio remains high on the merit of its strong future revenues. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

Before you settle on your opinion, we've discovered 2 warning signs for BAIC BluePark New Energy TechnologyLtd that you should be aware of.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if BAIC BluePark New Energy TechnologyLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600733

BAIC BluePark New Energy TechnologyLtd

BAIC BluePark New Energy Technology Co., Ltd.

High growth potential with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|20.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.5% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|20.5% undervalued

CH

Community Contributor