- China

- /

- Auto Components

- /

- SHSE:600699

Ningbo Joyson Electronic (SHSE:600699) Has A Somewhat Strained Balance Sheet

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Ningbo Joyson Electronic Corp. (SHSE:600699) does carry debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Ningbo Joyson Electronic

What Is Ningbo Joyson Electronic's Net Debt?

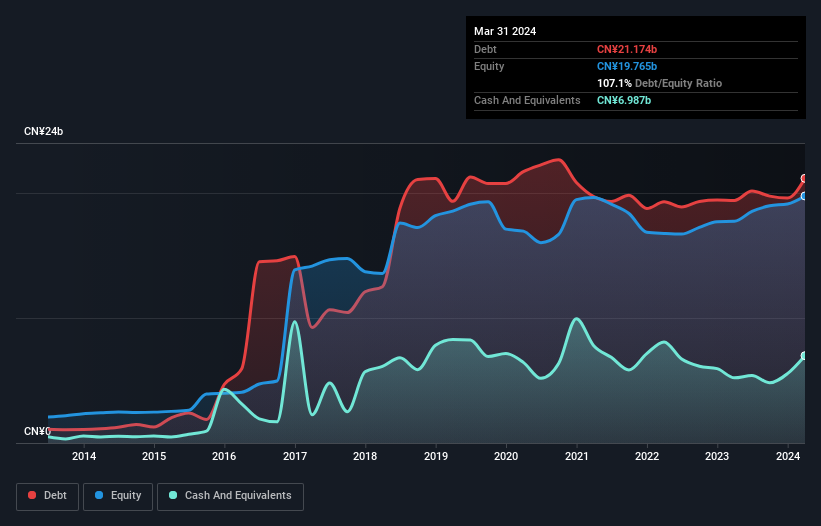

The image below, which you can click on for greater detail, shows that at March 2024 Ningbo Joyson Electronic had debt of CN¥21.2b, up from CN¥19.4b in one year. However, it does have CN¥6.99b in cash offsetting this, leading to net debt of about CN¥14.2b.

A Look At Ningbo Joyson Electronic's Liabilities

We can see from the most recent balance sheet that Ningbo Joyson Electronic had liabilities of CN¥21.6b falling due within a year, and liabilities of CN¥17.4b due beyond that. Offsetting these obligations, it had cash of CN¥6.99b as well as receivables valued at CN¥10.0b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥21.9b.

This is a mountain of leverage relative to its market capitalization of CN¥24.2b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Ningbo Joyson Electronic's debt is 3.4 times its EBITDA, and its EBIT cover its interest expense 3.2 times over. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. However, it should be some comfort for shareholders to recall that Ningbo Joyson Electronic actually grew its EBIT by a hefty 117%, over the last 12 months. If it can keep walking that path it will be in a position to shed its debt with relative ease. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Ningbo Joyson Electronic can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of that EBIT is backed by free cash flow. Considering the last two years, Ningbo Joyson Electronic actually recorded a cash outflow, overall. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for an improvement.

Our View

We'd go so far as to say Ningbo Joyson Electronic's conversion of EBIT to free cash flow was disappointing. But on the bright side, its EBIT growth rate is a good sign, and makes us more optimistic. Looking at the balance sheet and taking into account all these factors, we do believe that debt is making Ningbo Joyson Electronic stock a bit risky. Some people like that sort of risk, but we're mindful of the potential pitfalls, so we'd probably prefer it carry less debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 3 warning signs we've spotted with Ningbo Joyson Electronic (including 1 which is significant) .

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Ningbo Joyson Electronic might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600699

Ningbo Joyson Electronic

Engages in the research and development, manufacturing, and sale of automotive parts and accessories in China, the United States, Japan, Germany, Mexico, Italy, Romania, Portugal, Poland, Brazil, India, and internationally.

Solid track record average dividend payer.

Market Insights

Community Narratives