- Chile

- /

- Consumer Durables

- /

- SNSE:ELUXSA

Electrolux de Chile's (SNSE:ELUXSA) Strong Earnings Are Of Good Quality

Even though Electrolux de Chile S.A.'s (SNSE:ELUXSA) recent earnings release was robust, the market didn't seem to notice. Our analysis suggests that investors might be missing some promising details.

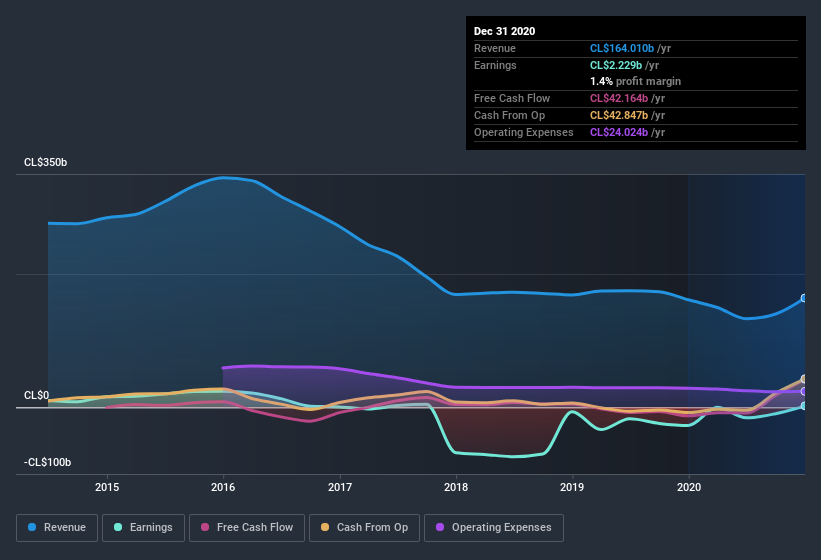

See our latest analysis for Electrolux de Chile

A Closer Look At Electrolux de Chile's Earnings

As finance nerds would already know, the accrual ratio from cashflow is a key measure for assessing how well a company's free cash flow (FCF) matches its profit. The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. This ratio tells us how much of a company's profit is not backed by free cashflow.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. That is not intended to imply we should worry about a positive accrual ratio, but it's worth noting where the accrual ratio is rather high. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

Electrolux de Chile has an accrual ratio of -0.32 for the year to December 2020. That indicates that its free cash flow quite significantly exceeded its statutory profit. In fact, it had free cash flow of CL$42b in the last year, which was a lot more than its statutory profit of CL$2.23b. Given that Electrolux de Chile had negative free cash flow in the prior corresponding period, the trailing twelve month resul of CL$42b would seem to be a step in the right direction. Notably, the company has issued new shares, thus diluting existing shareholders and reducing their share of future earnings.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Electrolux de Chile.

One essential aspect of assessing earnings quality is to look at how much a company is diluting shareholders. As it happens, Electrolux de Chile issued 5.4% more new shares over the last year. As a result, its net income is now split between a greater number of shares. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. You can see a chart of Electrolux de Chile's EPS by clicking here.

How Is Dilution Impacting Electrolux de Chile's Earnings Per Share? (EPS)

Electrolux de Chile was losing money three years ago. And even focusing only on the last twelve months, we don't have a meaningful growth rate because it made a loss a year ago, too. But mathematics aside, it is always good to see when a formerly unprofitable business come good (though we accept profit would have been higher if dilution had not been required). Therefore, the dilution is having a noteworthy influence on shareholder returns.

In the long term, if Electrolux de Chile's earnings per share can increase, then the share price should too. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

Our Take On Electrolux de Chile's Profit Performance

In conclusion, Electrolux de Chile has a strong cashflow relative to earnings, which indicates good quality earnings, but the dilution means its earnings per share are dropping faster than its profit. Considering all the aforementioned, we'd venture that Electrolux de Chile's profit result is a pretty good guide to its true profitability, albeit a bit on the conservative side. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. In terms of investment risks, we've identified 1 warning sign with Electrolux de Chile, and understanding this should be part of your investment process.

Our examination of Electrolux de Chile has focussed on certain factors that can make its earnings look better than they are. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you’re looking to trade Electrolux de Chile, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Electrolux de Chile might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SNSE:ELUXSA

Electrolux de Chile

Electrolux de Chile S.A. manufactures and sells household appliances for consumers and professionals.

Adequate balance sheet and overvalued.

Market Insights

Community Narratives