- Chile

- /

- Industrials

- /

- SNSE:QUINENCO

Investors Met With Slowing Returns on Capital At Quiñenco (SNSE:QUINENCO)

Finding a business that has the potential to grow substantially is not easy, but it is possible if we look at a few key financial metrics. One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. In light of that, when we looked at Quiñenco (SNSE:QUINENCO) and its ROCE trend, we weren't exactly thrilled.

Understanding Return On Capital Employed (ROCE)

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on Quiñenco is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

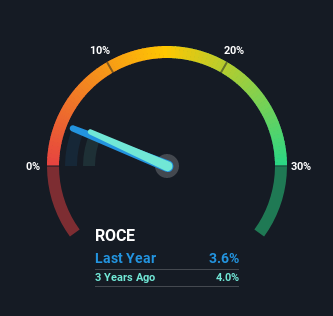

0.036 = CL$811b ÷ (CL$55t - CL$32t) (Based on the trailing twelve months to June 2021).

So, Quiñenco has an ROCE of 3.6%. On its own that's a low return on capital but it's in line with the industry's average returns of 4.5%.

See our latest analysis for Quiñenco

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating Quiñenco's past further, check out this free graph of past earnings, revenue and cash flow.

What Can We Tell From Quiñenco's ROCE Trend?

There are better returns on capital out there than what we're seeing at Quiñenco. The company has consistently earned 3.6% for the last five years, and the capital employed within the business has risen 61% in that time. This poor ROCE doesn't inspire confidence right now, and with the increase in capital employed, it's evident that the business isn't deploying the funds into high return investments.

Another thing to note, Quiñenco has a high ratio of current liabilities to total assets of 59%. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. While it's not necessarily a bad thing, it can be beneficial if this ratio is lower.

In Conclusion...

As we've seen above, Quiñenco's returns on capital haven't increased but it is reinvesting in the business. And with the stock having returned a mere 37% in the last five years to shareholders, you could argue that they're aware of these lackluster trends. So if you're looking for a multi-bagger, the underlying trends indicate you may have better chances elsewhere.

If you'd like to know more about Quiñenco, we've spotted 2 warning signs, and 1 of them shouldn't be ignored.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

Valuation is complex, but we're here to simplify it.

Discover if Quiñenco might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SNSE:QUINENCO

Quiñenco

A business conglomerate, operates in the industrial and financial services sectors in Chile and internationally.

Adequate balance sheet slight.