Advertisement

- Switzerland

- /

- Biotech

- /

- SWX:RLF

We Wouldn't Rely On Relief Therapeutics Holding's (VTX:RLF) Statutory Earnings As A Guide

Many investors consider it preferable to invest in profitable companies over unprofitable ones, because profitability suggests a business is sustainable. Having said that, sometimes statutory profit levels are not a good guide to ongoing profitability, because some short term one-off factor has impacted profit levels. This article will consider whether Relief Therapeutics Holding's (VTX:RLF) statutory profits are a good guide to its underlying earnings.

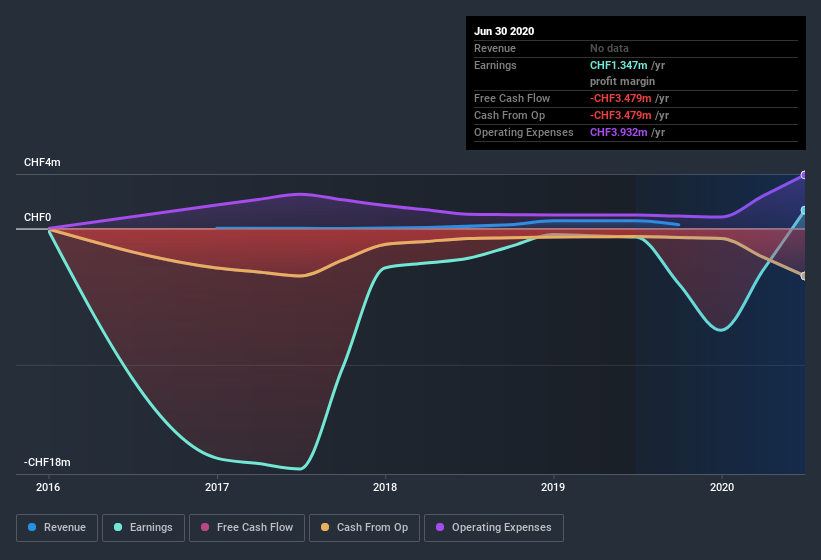

While Relief Therapeutics Holding was able to generate revenue of CHF283.5k in the last twelve months, we think its profit result of CHF1.35m was more important. Even though revenue has remained steady over the last three years, you can see in the chart below that the company has moved from loss-making to profitable.

Check out our latest analysis for Relief Therapeutics Holding

Importantly, statutory profits are not always the best tool for understanding a company's true earnings power, so it's well worth examining profits in a little more detail. Therefore, today we'll take a look at Relief Therapeutics Holding's cashflow, share issues and unusual items with a view to better understanding the nature of its statutory earnings. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Relief Therapeutics Holding.

Examining Cashflow Against Relief Therapeutics Holding's Earnings

Many investors haven't heard of the accrual ratio from cashflow, but it is actually a useful measure of how well a company's profit is backed up by free cash flow (FCF) during a given period. The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. The ratio shows us how much a company's profit exceeds its FCF.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

Relief Therapeutics Holding has an accrual ratio of 0.20 for the year to June 2020. Unfortunately, that means its free cash flow fell significantly short of its reported profits. In the last twelve months it actually had negative free cash flow, with an outflow of CHF3.5m despite its profit of CHF1.35m, mentioned above. We also note that Relief Therapeutics Holding's free cash flow was actually negative last year as well, so we could understand if shareholders were bothered by its outflow of CHF3.5m. Having said that, there is more to consider. We must also consider the impact of unusual items on statutory profit (and thus the accrual ratio), as well as note the ramifications of the company issuing new shares. The good news for shareholders is that Relief Therapeutics Holding's accrual ratio was much better last year, so this year's poor reading might simply be a case of a short term mismatch between profit and FCF. Shareholders should look for improved cashflow relative to profit in the current year, if that is indeed the case.

In order to understand the potential for per share returns, it is essential to consider how much a company is diluting shareholders. As it happens, Relief Therapeutics Holding issued 54% more new shares over the last year. As a result, its net income is now split between a greater number of shares. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. Check out Relief Therapeutics Holding's historical EPS growth by clicking on this link.

How Is Dilution Impacting Relief Therapeutics Holding's Earnings Per Share? (EPS)

Three years ago, Relief Therapeutics Holding lost money. Zooming in to the last year, we still can't talk about growth rates coherently, since it made a loss last year. But mathematics aside, it is always good to see when a formerly unprofitable business come good (though we accept profit would have been higher if dilution had not been required). And so, you can see quite clearly that dilution is having a rather significant impact on shareholders.

In the long term, if Relief Therapeutics Holding's earnings per share can increase, then the share price should too. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

How Do Unusual Items Influence Profit?

The fact that the company had unusual items boosting profit by CHF2.5m, in the last year, probably goes some way to explain why its accrual ratio was so weak. While it's always nice to have higher profit, a large contribution from unusual items sometimes dampens our enthusiasm. We ran the numbers on most publicly listed companies worldwide, and it's very common for unusual items to be once-off in nature. And, after all, that's exactly what the accounting terminology implies. Relief Therapeutics Holding had a rather significant contribution from unusual items relative to its profit to June 2020. All else being equal, this would likely have the effect of making the statutory profit a poor guide to underlying earnings power.

Our Take On Relief Therapeutics Holding's Profit Performance

In conclusion, Relief Therapeutics Holding's weak accrual ratio suggested its statutory earnings have been inflated by the unusual items. The dilution means the results are weaker when viewed from a per-share perspective. For all the reasons mentioned above, we think that, at a glance, Relief Therapeutics Holding's statutory profits could be considered to be low quality, because they are likely to give investors an overly positive impression of the company. Keep in mind, when it comes to analysing a stock it's worth noting the risks involved. Be aware that Relief Therapeutics Holding is showing 4 warning signs in our investment analysis and 3 of those shouldn't be ignored...

In this article we've looked at a number of factors that can impair the utility of profit numbers, and we've come away cautious. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you decide to trade Relief Therapeutics Holding, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SWX:RLF

Relief Therapeutics Holding

A biopharmaceutical company, engages in identification, development, and commercialization of novel, patent protected products for the treatment of dermatological, metabolic, and pulmonary rare diseases in Switzerland, Europe, North America, and internationally.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|28.3% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.8% undervalued

AG

Community Contributor