Advertisement

- Switzerland

- /

- Food

- /

- SWX:LISN

These 4 Measures Indicate That Chocoladefabriken Lindt & Sprüngli (VTX:LISN) Is Using Debt Reasonably Well

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Chocoladefabriken Lindt & Sprüngli AG (VTX:LISN) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Chocoladefabriken Lindt & Sprüngli

How Much Debt Does Chocoladefabriken Lindt & Sprüngli Carry?

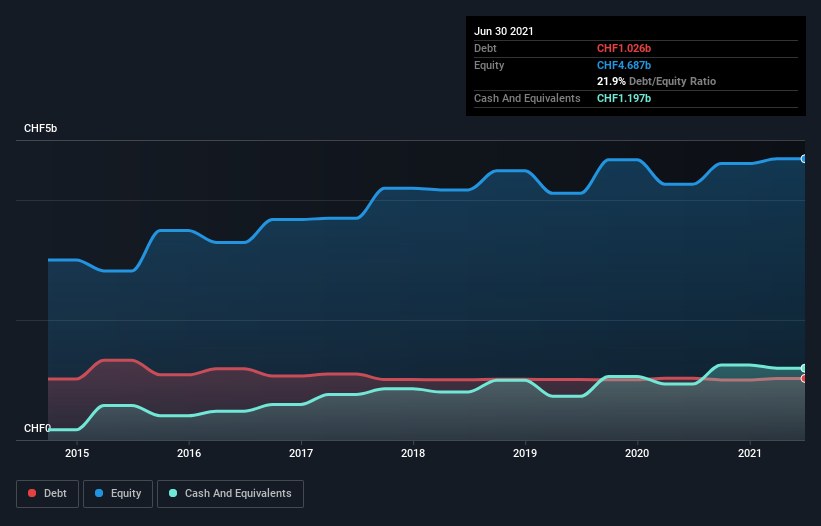

As you can see below, Chocoladefabriken Lindt & Sprüngli had CHF1.03b of debt, at June 2021, which is about the same as the year before. You can click the chart for greater detail. However, it does have CHF1.20b in cash offsetting this, leading to net cash of CHF170.4m.

How Healthy Is Chocoladefabriken Lindt & Sprüngli's Balance Sheet?

According to the last reported balance sheet, Chocoladefabriken Lindt & Sprüngli had liabilities of CHF1.15b due within 12 months, and liabilities of CHF2.24b due beyond 12 months. Offsetting this, it had CHF1.20b in cash and CHF565.3m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by CHF1.63b.

Given Chocoladefabriken Lindt & Sprüngli has a humongous market capitalization of CHF24.8b, it's hard to believe these liabilities pose much threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. While it does have liabilities worth noting, Chocoladefabriken Lindt & Sprüngli also has more cash than debt, so we're pretty confident it can manage its debt safely.

While Chocoladefabriken Lindt & Sprüngli doesn't seem to have gained much on the EBIT line, at least earnings remain stable for now. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Chocoladefabriken Lindt & Sprüngli can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. Chocoladefabriken Lindt & Sprüngli may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last three years, Chocoladefabriken Lindt & Sprüngli recorded free cash flow worth a fulsome 87% of its EBIT, which is stronger than we'd usually expect. That puts it in a very strong position to pay down debt.

Summing up

While it is always sensible to look at a company's total liabilities, it is very reassuring that Chocoladefabriken Lindt & Sprüngli has CHF170.4m in net cash. And it impressed us with free cash flow of CHF578m, being 87% of its EBIT. So is Chocoladefabriken Lindt & Sprüngli's debt a risk? It doesn't seem so to us. Over time, share prices tend to follow earnings per share, so if you're interested in Chocoladefabriken Lindt & Sprüngli, you may well want to click here to check an interactive graph of its earnings per share history.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you’re looking to trade Chocoladefabriken Lindt & Sprüngli, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SWX:LISN

Chocoladefabriken Lindt & Sprüngli

Engages in the manufacture and sale of chocolate products worldwide.

Excellent balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor