UBS Group (SWX:UBSG) shares have shown mixed signals over the past month, dipping slightly despite a solid year-to-date gain. Investors are closely watching recent trends to gauge where the stock could head next.

UBS Group's recent 4.6% dip in 1-month share price return has not erased the tailwind from a strong year-to-date gain. Long-term investors have enjoyed a robust 190.7% total shareholder return over five years. Momentum appears to be shifting lately as the market recalibrates expectations following rapid gains.

With UBS shares still trading at a slight discount to analyst price targets and impressive multi-year returns in tow, the key question now is whether UBS is undervalued or if future growth is already priced in.

Advertisement

Most Popular Narrative: 6.5% Undervalued

UBS Group's most widely followed narrative suggests its fair value sits above the recent closing price. The consensus sees current levels as a potential bargain, based on a blend of operational improvements, revenue growth, and sector dynamics that have yet to fully play out.

“The ongoing integration of Credit Suisse is progressing ahead of schedule, driving meaningful cost savings, increased scale, and improved operating efficiency. As these synergies are realized through further platform migration and operational streamlining, UBS's net margins and return on equity are likely to improve, supporting higher earnings growth.”

Want to know what assumptions lie behind this confidence? The financial blueprint powering this narrative is focused on accelerating profit margins and an ambitious future earnings target. Curious to uncover which projections were bold enough to boost the fair value? Dive in to see what the consensus is betting on for UBS’s next phase.

However, heightened regulatory requirements or setbacks in integrating Credit Suisse could challenge UBS’s growth outlook. These factors may keep investor caution firmly in play.

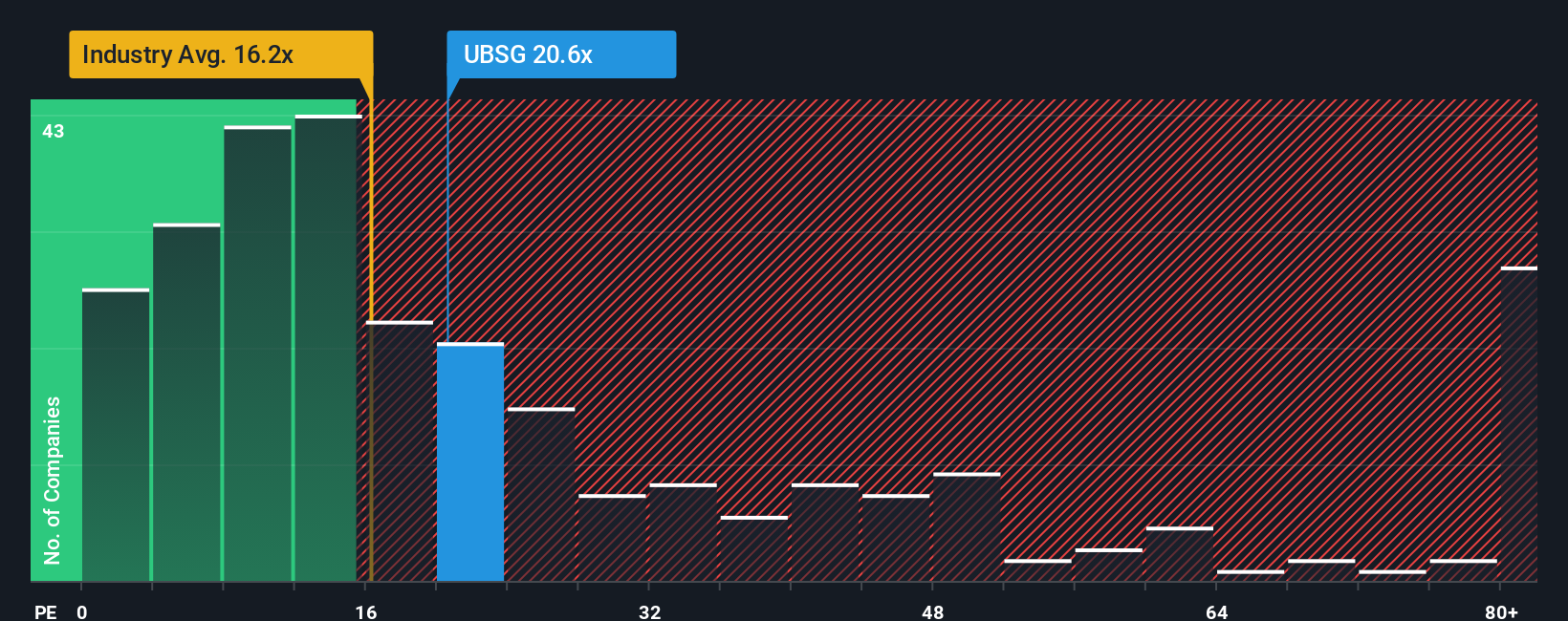

While our first approach points to UBS as undervalued, looking at its price-to-earnings ratio tells a slightly different story. UBS trades at 16.6 times earnings, which aligns with the Capital Markets industry average of 16.3 and is considerably lower than the peer average of 20.9. Compared to its fair ratio of 25.1, the current level suggests there may still be room for the market to re-rate higher, but this would not come without some risks if expectations shift.

If the current outlook does not align with your perspective, you can examine the underlying numbers and shape your own narrative in just a few short minutes, all at your own pace. Do it your way

Don't wait on the sidelines while smarter investors take action. Use Simply Wall Street’s powerful screener to spot hidden opportunities tailored to you.

Get ahead of the tech curve and target companies fueling healthcare breakthroughs by exploring these 33 healthcare AI stocks, shaping tomorrow’s medical landscape today.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies