- Switzerland

- /

- Capital Markets

- /

- SWX:PGHN

3 Growth Companies With High Insider Ownership On SIX Swiss Exchange Featuring 51 Percent Return On Equity

Reviewed by Simply Wall St

The Swiss market demonstrated resilience, rebounding from a weak start to close on a strong note with the SMI gaining 0.93% as major companies like Sandoz Group and Julius Baer posted notable gains. In such an environment, growth companies with high insider ownership can be particularly appealing as they often signal confidence in the company's potential and alignment of interests between insiders and shareholders.

Top 10 Growth Companies With High Insider Ownership In Switzerland

| Name | Insider Ownership | Earnings Growth |

| Stadler Rail (SWX:SRAIL) | 14.5% | 24.1% |

| VAT Group (SWX:VACN) | 10.2% | 22.5% |

| Addex Therapeutics (SWX:ADXN) | 19% | 33.3% |

| Straumann Holding (SWX:STMN) | 32.7% | 21.8% |

| Swissquote Group Holding (SWX:SQN) | 11.4% | 12.6% |

| LEM Holding (SWX:LEHN) | 29.9% | 18.4% |

| Temenos (SWX:TEMN) | 21.8% | 14.4% |

| V-ZUG Holding (SWX:VZUG) | 20.9% | 38.7% |

| Sensirion Holding (SWX:SENS) | 19.9% | 102.7% |

| Leonteq (SWX:LEON) | 11.9% | 35.1% |

Let's uncover some gems from our specialized screener.

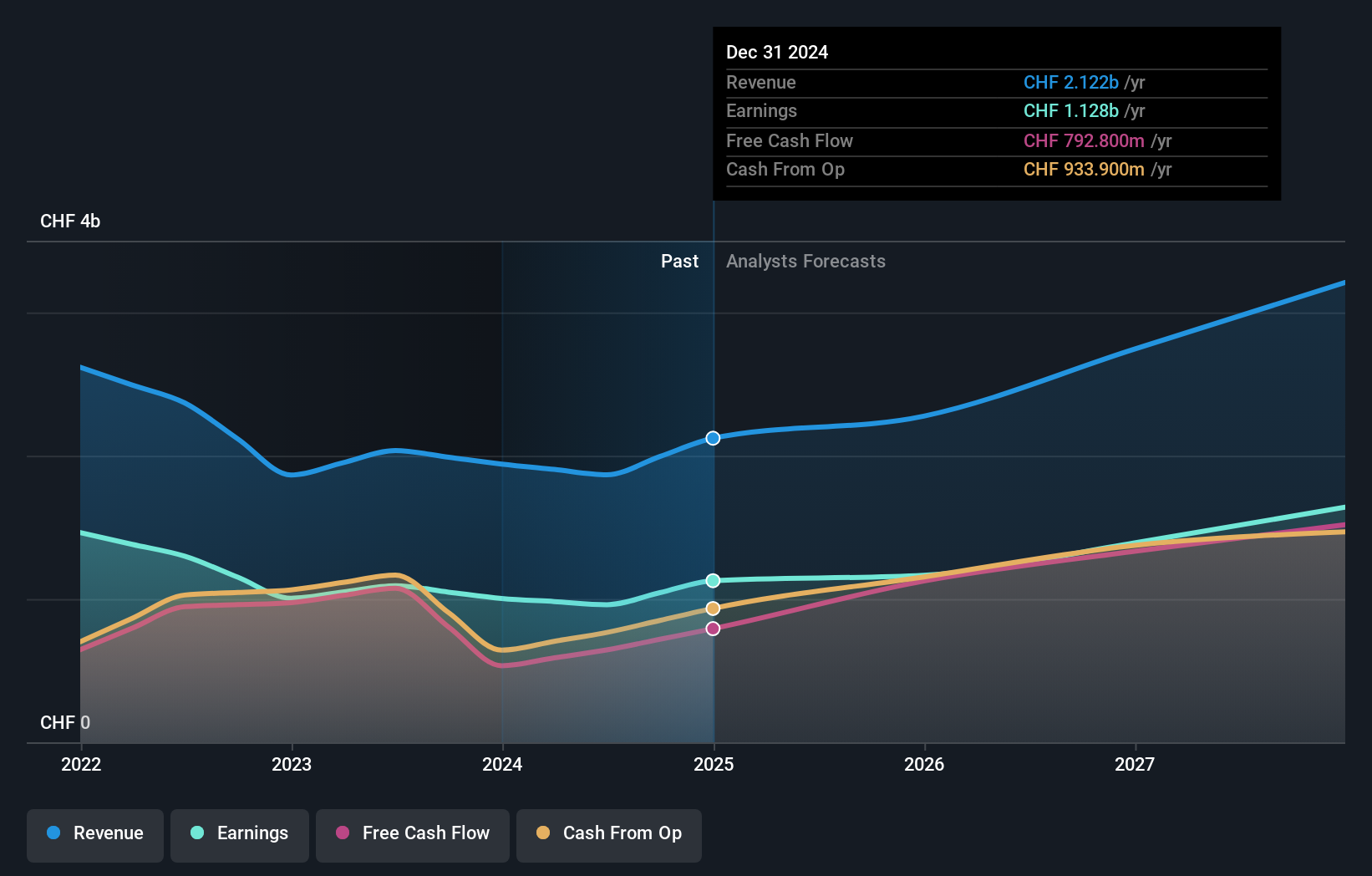

Partners Group Holding (SWX:PGHN)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Partners Group Holding AG is a private equity firm that focuses on direct, secondary, and primary investments in private equity, real estate, infrastructure, and debt with a market cap of CHF33.52 billion.

Operations: The company's revenue segments are comprised of CHF1.19 billion from Private Equity, CHF254.90 million from Infrastructure, CHF218.90 million from Private Credit, and CHF190.90 million from Real Estate.

Insider Ownership: 17%

Return On Equity Forecast: 51% (2027 estimate)

Partners Group Holding, with significant insider ownership, is positioned as a growth company in Switzerland. Despite a high level of debt and recent earnings decline to CHF 508 million for H1 2024, its forecasted earnings growth of 14.5% annually surpasses the Swiss market average. The company's involvement in potential M&A activities, such as the I-MED Radiology acquisition discussions, highlights its strategic expansion focus. However, dividends remain inadequately covered by earnings or free cash flows.

- Delve into the full analysis future growth report here for a deeper understanding of Partners Group Holding.

- According our valuation report, there's an indication that Partners Group Holding's share price might be on the expensive side.

Stadler Rail (SWX:SRAIL)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Stadler Rail AG is a company that manufactures and sells trains across Switzerland, Germany, Austria, various European regions, the Americas, CIS countries and internationally with a market cap of CHF2.61 billion.

Operations: The company's revenue segments consist of CHF3.10 billion from Rolling Stock, CHF789.41 million from Service & Components, and CHF135.68 million from Signalling.

Insider Ownership: 14.5%

Return On Equity Forecast: 22% (2027 estimate)

Stadler Rail, with high insider ownership, is set for robust earnings growth of 24.1% annually, outpacing the Swiss market average. Despite a slight dip in net income to CHF 23.95 million for H1 2024, its revenue forecast of 8.9% per year exceeds the market's growth rate. However, dividends are not well covered by free cash flows. The company's return on equity is expected to be strong at 21.7% in three years.

- Get an in-depth perspective on Stadler Rail's performance by reading our analyst estimates report here.

- According our valuation report, there's an indication that Stadler Rail's share price might be on the cheaper side.

Temenos (SWX:TEMN)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Temenos AG develops, markets, and sells integrated banking software systems to financial institutions globally, with a market cap of CHF4.51 billion.

Operations: The company's revenue is divided into two main segments: Product, generating $879.99 million, and Services, contributing $132.98 million.

Insider Ownership: 21.8%

Return On Equity Forecast: 25% (2027 estimate)

Temenos is poised for solid growth, with earnings expected to increase by 14.4% annually, surpassing the Swiss market average. Recent executive appointments aim to enhance its SaaS and US market presence. Despite trading at a discount to fair value, Temenos carries significant debt. The company completed a CHF 200 million share buyback and is considering selling its fund management unit for EUR 600 million, potentially bolstering financial flexibility amid evolving leadership dynamics in technology and product development.

- Click here to discover the nuances of Temenos with our detailed analytical future growth report.

- Our expertly prepared valuation report Temenos implies its share price may be lower than expected.

Next Steps

- Dive into all 14 of the Fast Growing SIX Swiss Exchange Companies With High Insider Ownership we have identified here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SWX:PGHN

Partners Group Holding

A private equity firm specializing in direct, secondary, and primary investments across private equity, private real estate, private infrastructure, and private debt.

Reasonable growth potential with adequate balance sheet.