- Switzerland

- /

- Software

- /

- SWX:TEMN

3 Growth Companies With High Insider Ownership On SIX Swiss Exchange

Reviewed by Simply Wall St

The Swiss market experienced a modest uptick recently, buoyed by expectations of further interest rate cuts following the European Central Bank's latest reduction. In this environment, identifying growth companies with high insider ownership on the SIX Swiss Exchange can be appealing to investors, as these stocks often reflect strong confidence from those closest to the business.

Top 10 Growth Companies With High Insider Ownership In Switzerland

| Name | Insider Ownership | Earnings Growth |

| LEM Holding (SWX:LEHN) | 29.9% | 20.5% |

| Stadler Rail (SWX:SRAIL) | 14.5% | 24.1% |

| VAT Group (SWX:VACN) | 10.2% | 21.5% |

| Straumann Holding (SWX:STMN) | 32.7% | 21.7% |

| Addex Therapeutics (SWX:ADXN) | 19% | 33.3% |

| Swissquote Group Holding (SWX:SQN) | 11.4% | 12.6% |

| Temenos (SWX:TEMN) | 21.8% | 14.4% |

| V-ZUG Holding (SWX:VZUG) | 20.9% | 38.7% |

| Partners Group Holding (SWX:PGHN) | 17% | 14.2% |

| Sensirion Holding (SWX:SENS) | 19.9% | 102.7% |

Let's uncover some gems from our specialized screener.

Stadler Rail (SWX:SRAIL)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Stadler Rail AG is a company that manufactures and sells trains across Switzerland, Germany, Austria, various parts of Europe, the Americas, and CIS countries, with a market cap of CHF2.60 billion.

Operations: The company's revenue is primarily derived from Rolling Stock at CHF3.10 billion, followed by Service & Components at CHF789.41 million, and Signalling at CHF135.68 million.

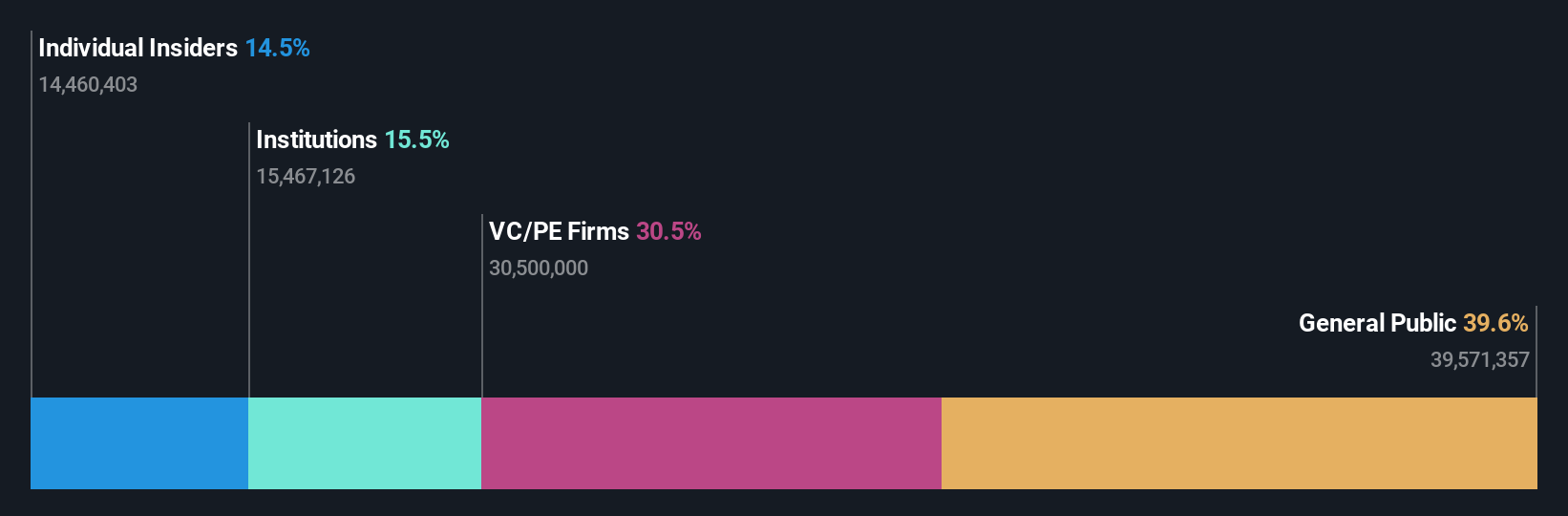

Insider Ownership: 14.5%

Earnings Growth Forecast: 24.1% p.a.

Stadler Rail demonstrates growth potential with forecasted revenue expansion of 8.9% annually, outpacing the Swiss market's 4.2%. Despite recent earnings showing a slight decline in net income to CHF 23.95 million, its earnings are expected to grow significantly at over 24% per year. Although trading well below its estimated fair value, the dividend yield of 3.45% is not fully covered by free cash flow, highlighting a potential risk for investors focusing on dividends.

- Dive into the specifics of Stadler Rail here with our thorough growth forecast report.

- The valuation report we've compiled suggests that Stadler Rail's current price could be quite moderate.

Temenos (SWX:TEMN)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Temenos AG develops, markets, and sells integrated banking software systems to financial institutions globally, with a market cap of CHF4.66 billion.

Operations: The company's revenue is derived from two main segments: Products, contributing $879.99 million, and Services, which account for $132.98 million.

Insider Ownership: 21.8%

Earnings Growth Forecast: 14.4% p.a.

Temenos showcases growth potential with earnings forecasted to increase by 14.4% annually, surpassing the Swiss market's 11.6%. Its revenue is expected to grow at 7.6% per year, faster than the market's average but below significant levels. The company trades at a discount to its estimated fair value despite having high debt levels. Recent executive appointments aim to bolster technology and product development, enhancing global reach through AI-driven solutions and cloud platforms.

- Take a closer look at Temenos' potential here in our earnings growth report.

- Our valuation report unveils the possibility Temenos' shares may be trading at a premium.

V-ZUG Holding (SWX:VZUG)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: V-ZUG Holding AG specializes in the development, manufacture, marketing, sale, and servicing of kitchen and laundry appliances for private households both in Switzerland and internationally, with a market capitalization of CHF353.57 million.

Operations: The company generates revenue of CHF571.35 million from its household appliances segment, which includes kitchen and laundry products for private households in Switzerland and internationally.

Insider Ownership: 20.9%

Earnings Growth Forecast: 38.7% p.a.

V-ZUG Holding demonstrates strong growth potential with earnings projected to increase significantly at 38.7% annually, outpacing the Swiss market's 11.6%. Despite its revenue growth forecast of 4.4% being modest, it still surpasses the market average slightly. The stock trades at a substantial discount to its estimated fair value, offering potential upside for investors mindful of its low return on equity forecast of 7.5% in three years and lack of recent insider trading activity.

- Navigate through the intricacies of V-ZUG Holding with our comprehensive analyst estimates report here.

- In light of our recent valuation report, it seems possible that V-ZUG Holding is trading behind its estimated value.

Summing It All Up

- Click this link to deep-dive into the 14 companies within our Fast Growing SIX Swiss Exchange Companies With High Insider Ownership screener.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Temenos might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SWX:TEMN

Temenos

Develops, markets, and sells integrated banking software systems to banking and other financial institutions worldwide.

Reasonable growth potential with proven track record and pays a dividend.