- Switzerland

- /

- Software

- /

- SWX:TEMN

3 Growth Companies On SIX Swiss Exchange With Up To 38% Earnings Growth

Reviewed by Simply Wall St

The Swiss market recently experienced a mixed session, with the SMI index managing to close slightly up despite early losses, reflecting a cautious yet resilient investor sentiment. In this context of fluctuating market dynamics, growth companies with high insider ownership often attract attention due to their potential for significant earnings growth and alignment of interests between management and shareholders.

Top 10 Growth Companies With High Insider Ownership In Switzerland

| Name | Insider Ownership | Earnings Growth |

| Stadler Rail (SWX:SRAIL) | 14.5% | 24.1% |

| VAT Group (SWX:VACN) | 10.2% | 22.5% |

| Addex Therapeutics (SWX:ADXN) | 19% | 33.3% |

| Straumann Holding (SWX:STMN) | 32.7% | 21.8% |

| LEM Holding (SWX:LEHN) | 29.9% | 18.4% |

| Swissquote Group Holding (SWX:SQN) | 11.4% | 12.6% |

| Temenos (SWX:TEMN) | 21.8% | 14.4% |

| Partners Group Holding (SWX:PGHN) | 17% | 14.5% |

| Hocn (SWX:HOCN) | 14.6% | 122.2% |

| Sensirion Holding (SWX:SENS) | 19.9% | 102.7% |

Let's dive into some prime choices out of the screener.

Leonteq (SWX:LEON)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Leonteq AG offers structured investment products and long-term savings and retirement solutions across Switzerland, Europe, and Asia including the Middle East, with a market cap of CHF484.43 million.

Operations: Leonteq generates revenue through its structured investment products and long-term savings and retirement solutions across Switzerland, Europe, and Asia including the Middle East.

Insider Ownership: 11.9%

Earnings Growth Forecast: 35.1% p.a.

Leonteq AG, a Swiss financial services company, is poised for significant earnings growth with forecasts suggesting a 35.1% annual increase, outpacing the broader Swiss market. Despite recent declines in revenue and net income for H1 2024 to CHF 133.4 million and CHF 15.7 million respectively, the company trades at a substantial discount to its estimated fair value. However, challenges include low return on equity projections and unsustainable dividend coverage from current earnings levels.

- Unlock comprehensive insights into our analysis of Leonteq stock in this growth report.

- According our valuation report, there's an indication that Leonteq's share price might be on the expensive side.

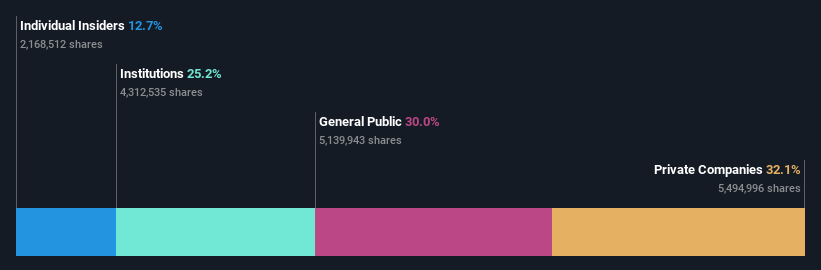

Temenos (SWX:TEMN)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Temenos AG develops, markets, and sells integrated banking software systems to banking and other financial institutions worldwide, with a market cap of CHF4.31 billion.

Operations: The company's revenue is primarily derived from its Product segment, which generated $879.99 million, and its Services segment, contributing $132.98 million.

Insider Ownership: 21.8%

Earnings Growth Forecast: 14.4% p.a.

Temenos is experiencing moderate growth, with earnings and revenue projected to rise at 14.4% and 7.6% annually, respectively, outpacing the Swiss market. Despite trading below estimated fair value, it faces challenges with high debt levels. Recent executive appointments aim to enhance its global SaaS footprint and AI capabilities. The company's recent CHF 200 million buyback reflects confidence in its strategy amid considerations to sell a fund management unit for EUR 600 million.

- Click to explore a detailed breakdown of our findings in Temenos' earnings growth report.

- According our valuation report, there's an indication that Temenos' share price might be on the cheaper side.

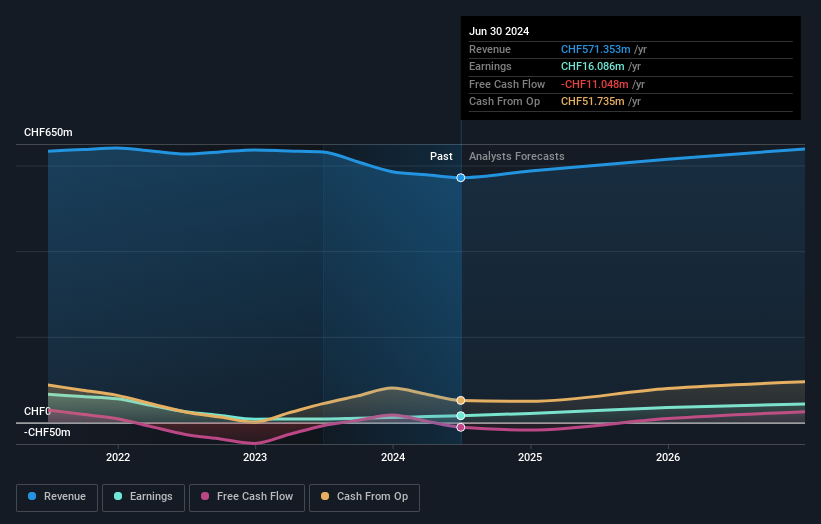

V-ZUG Holding (SWX:VZUG)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: V-ZUG Holding AG is involved in the development, manufacture, marketing, sale, and servicing of kitchen and laundry appliances for private households both in Switzerland and internationally, with a market cap of CHF348.43 million.

Operations: The company's revenue is primarily derived from its Household Appliances segment, totaling CHF571.35 million.

Insider Ownership: 20.9%

Earnings Growth Forecast: 38.7% p.a.

V-ZUG Holding shows promising growth prospects, with earnings increasing by 89.2% over the past year and forecasted to grow significantly at 38.7% annually, surpassing the Swiss market's average. Despite a slight decline in sales to CHF 284.08 million for H1 2024, net income more than doubled to CHF 8.73 million, indicating strong operational performance. The stock trades significantly below its estimated fair value but faces challenges with a low projected return on equity of 7.5%.

- Navigate through the intricacies of V-ZUG Holding with our comprehensive analyst estimates report here.

- Our valuation report unveils the possibility V-ZUG Holding's shares may be trading at a discount.

Next Steps

- Reveal the 13 hidden gems among our Fast Growing SIX Swiss Exchange Companies With High Insider Ownership screener with a single click here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Temenos might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SWX:TEMN

Temenos

Develops, markets, and sells integrated banking software systems to banking and other financial institutions worldwide.

Established dividend payer with reasonable growth potential.