Advertisement

- Canada

- /

- Renewable Energy

- /

- TSX:TA

Revenue Downgrade: Here's What Analysts Forecast For TransAlta Corporation (TSE:TA)

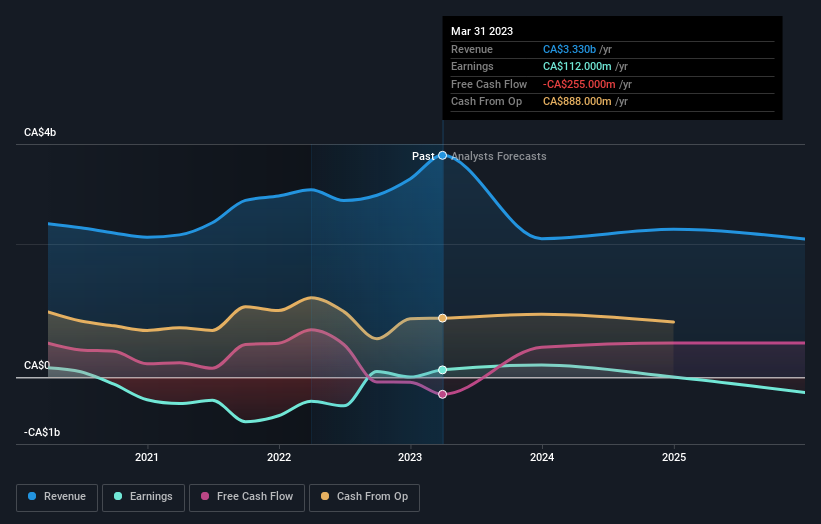

The latest analyst coverage could presage a bad day for TransAlta Corporation (TSE:TA), with the analysts making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. This report focused on revenue estimates, and it looks as though the consensus view of the business has become substantially more conservative. At CA$12.74, shares are up 5.5% in the past 7 days. We'd be curious to see if the downgrade is enough to reverse investor sentiment on the business.

Following the latest downgrade, the five analysts covering TransAlta provided consensus estimates of CA$2.1b revenue in 2023, which would reflect a substantial 38% decline on its sales over the past 12 months. Prior to the latest estimates, the analysts were forecasting revenues of CA$2.5b in 2023. The consensus view seems to have become more pessimistic on TransAlta, noting the measurable cut to revenue estimates in this update.

See our latest analysis for TransAlta

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. We would highlight that sales are expected to reverse, with a forecast 47% annualised revenue decline to the end of 2023. That is a notable change from historical growth of 6.0% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 3.5% per year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - TransAlta is expected to lag the wider industry.

The Bottom Line

The clear low-light was that analysts slashing their revenue forecasts for TransAlta this year. They're also anticipating slower revenue growth than the wider market. Overall, given the drastic downgrade to this year's forecasts, we'd be feeling a little more wary of TransAlta going forwards.

There might be good reason for analyst bearishness towards TransAlta, like a weak balance sheet. For more information, you can click here to discover this and the 2 other flags we've identified.

Another thing to consider is whether management and directors have been buying or selling stock recently. We provide an overview of all open market stock trades for the last twelve months on our platform, here.

Valuation is complex, but we're here to simplify it.

Discover if TransAlta might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:TA

TransAlta

Engages in the development, production, and sale of electric energy.

Good value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|35.7% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|20.5% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|25.2% overvalued

DA

Community Contributor