- Canada

- /

- Other Utilities

- /

- TSX:CU

Here's Why We're Wary Of Buying Canadian Utilities' (TSE:CU) For Its Upcoming Dividend

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see Canadian Utilities Limited (TSE:CU) is about to trade ex-dividend in the next 4 days. Typically, the ex-dividend date is one business day before the record date which is the date on which a company determines the shareholders eligible to receive a dividend. The ex-dividend date is important because any transaction on a stock needs to have been settled before the record date in order to be eligible for a dividend. Meaning, you will need to purchase Canadian Utilities' shares before the 1st of November to receive the dividend, which will be paid on the 1st of December.

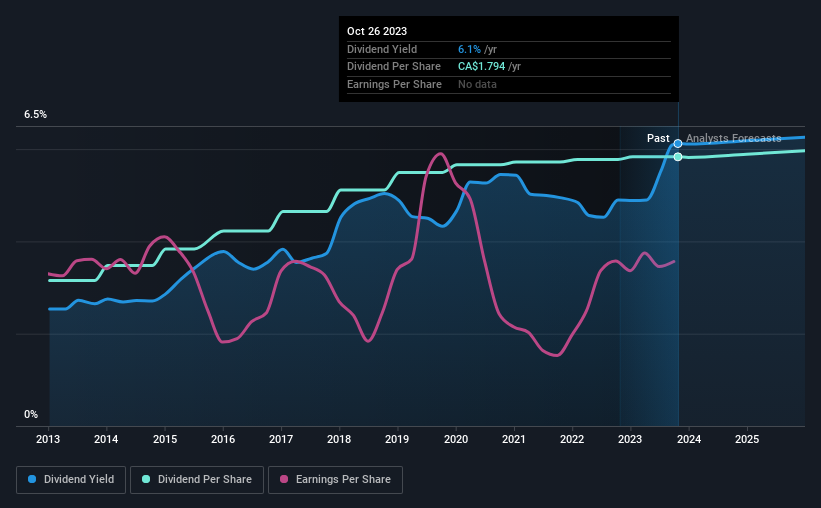

The company's upcoming dividend is CA$0.45 a share, following on from the last 12 months, when the company distributed a total of CA$1.79 per share to shareholders. Based on the last year's worth of payments, Canadian Utilities stock has a trailing yield of around 6.1% on the current share price of CA$29.32. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. We need to see whether the dividend is covered by earnings and if it's growing.

Check out our latest analysis for Canadian Utilities

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Its dividend payout ratio is 81% of profit, which means the company is paying out a majority of its earnings. The relatively limited profit reinvestment could slow the rate of future earnings growth. We'd be worried about the risk of a drop in earnings. Yet cash flows are even more important than profits for assessing a dividend, so we need to see if the company generated enough cash to pay its distribution. Over the past year it paid out 111% of its free cash flow as dividends, which is uncomfortably high. It's hard to consistently pay out more cash than you generate without either borrowing or using company cash, so we'd wonder how the company justifies this payout level.

Canadian Utilities paid out less in dividends than it reported in profits, but unfortunately it didn't generate enough cash to cover the dividend. Were this to happen repeatedly, this would be a risk to Canadian Utilities's ability to maintain its dividend.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. With that in mind, we're encouraged by the steady growth at Canadian Utilities, with earnings per share up 5.7% on average over the last five years. Earnings have been growing at a steady rate, but we're concerned dividend payments consumed most of the company's cash flow over the past year.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. In the last 10 years, Canadian Utilities has lifted its dividend by approximately 6.3% a year on average. It's encouraging to see the company lifting dividends while earnings are growing, suggesting at least some corporate interest in rewarding shareholders.

Final Takeaway

Is Canadian Utilities an attractive dividend stock, or better left on the shelf? Earnings per share have grown somewhat, although Canadian Utilities paid out over half its profits and the dividend was not well covered by free cash flow. It's not an attractive combination from a dividend perspective, and we're inclined to pass on this one for the time being.

With that being said, if you're still considering Canadian Utilities as an investment, you'll find it beneficial to know what risks this stock is facing. Every company has risks, and we've spotted 2 warning signs for Canadian Utilities (of which 1 can't be ignored!) you should know about.

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:CU

Canadian Utilities

Engages in the electricity, natural gas, renewables, pipelines, and liquids businesses in Canada, Australia, and internationally.

Second-rate dividend payer low.

Similar Companies

Market Insights

Community Narratives