Advertisement

- Canada

- /

- Wireless Telecom

- /

- TSX:RCI.B

Is Expanded Content Partnership and Raised Guidance Reshaping the Investment Case for Rogers (TSX:RCI.B)?

Simply Wall St

Reviewed by Simply Wall St

- In late July 2025, Rogers Communications raised its full-year service revenue guidance and entered into a significant content distribution partnership with Bell, granting expanded specialty channel access for television subscribers across both providers.

- This agreement signals a collaborative shift in Canadian media distribution, potentially reshaping content offerings and subscriber value in a highly competitive landscape.

- We will explore how the improved service revenue outlook and expanded content distribution are shaping Rogers Communications' investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 20 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Rogers Communications Investment Narrative Recap

To be a Rogers Communications shareholder, you need to believe in the company's ability to drive recurring growth in connectivity and media services, even as the Canadian wireless market matures and faces competitive and regulatory headwinds. The recent content partnership with Bell and raised service revenue guidance reinforce Rogers' push to improve subscriber value, but these developments do not fully offset the near-term risk from ongoing ARPU pressure and wireless market saturation.

Of the recent announcements, the uplift in full-year service revenue guidance to 3% to 5% is highly relevant. While this improved outlook reflects confidence in subscriber revenues, it comes alongside persistent net income declines and evidences the delicate balance Rogers must maintain between competitive pricing, rising costs, and investor expectations for profitable growth.

In contrast, investors should be aware that ARPU pressures from market competition and promotional activity remain a concern, particularly if...

Read the full narrative on Rogers Communications (it's free!)

Rogers Communications' outlook anticipates CA$22.7 billion in revenue and CA$2.8 billion in earnings by 2028. This reflects an annual revenue growth rate of 3.0% and a CA$1.3 billion increase in earnings from the current level of CA$1.5 billion.

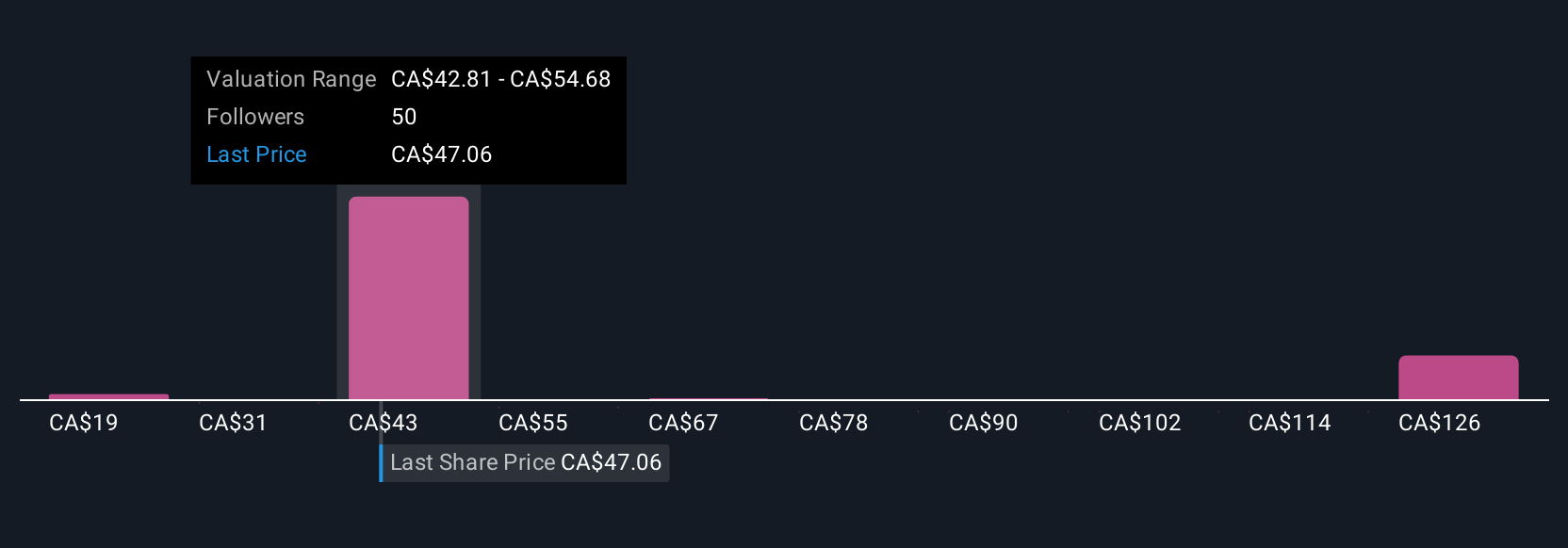

Uncover how Rogers Communications' forecasts yield a CA$55.15 fair value, a 19% upside to its current price.

Exploring Other Perspectives

The Simply Wall St Community shares 10 unique fair value estimates for Rogers ranging from CA$19.07 to CA$141.49 per share. While these opinions reveal wide differences, the company's raised service revenue guidance highlights why expectations for future growth and margin improvement can influence outlooks so much, be sure to explore multiple viewpoints before deciding what matters most.

Explore 10 other fair value estimates on Rogers Communications - why the stock might be worth less than half the current price!

Build Your Own Rogers Communications Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Rogers Communications research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Rogers Communications research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Rogers Communications' overall financial health at a glance.

Searching For A Fresh Perspective?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- These 19 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:RCI.B

Rogers Communications

Operates as a communications and media company in Canada.

Undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

A Quality Compounder Marked Down on Overblown Fears

Fair Value US$120.72|57.7% undervalued

BA

Community Contributor

Wyndham Continues Global Expansion with 19% Ancillary Revenue Growth

Fair Value US$105.80|20.6% undervalued

ZW

Community Contributor