Advertisement

BlackBerry (TSX:BB) Valuation Check After QNX Sound Win With Leading Chinese Luxury EV Maker

Simply Wall St

Reviewed by Simply Wall St

BlackBerry (TSX:BB) just landed a meaningful design win for its QNX Sound platform with a leading Chinese automaker, securing a spot in next generation luxury EVs and pushing its automotive software story forward.

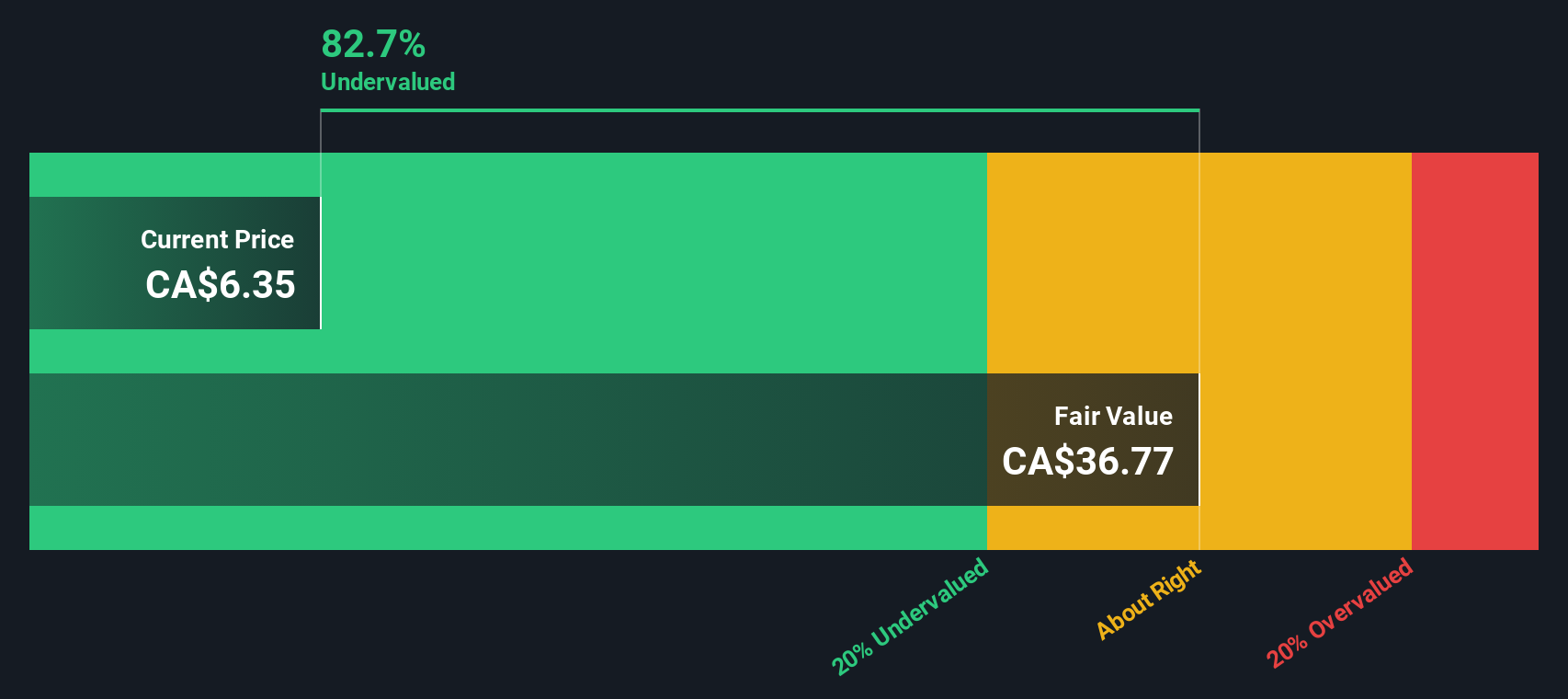

See our latest analysis for BlackBerry.

That backdrop helps explain why BlackBerry’s share price, now at $5.93, shows a solid 90 day share price return of 10.43% and a standout 1 year total shareholder return of 62.02%. This suggests momentum is rebuilding after recent volatility.

If this QNX win has you thinking more broadly about software and connected car plays, it could be a good moment to scout auto manufacturers for other interesting ideas in the space.

Yet with BlackBerry trading slightly above analyst targets but screens still flagging deep intrinsic value, investors face a key question: is this renewed momentum an underappreciated turnaround, or has the market already priced in the next leg of growth?

Price-to-Earnings of 127.3x: Is it justified?

On a headline basis, BlackBerry’s CA$5.93 share price translates into a steep price-to-earnings ratio of 127.3 times, well above peers and industry benchmarks.

The price-to-earnings ratio compares what investors pay today for each dollar of current earnings, a common yardstick for mature and emerging software names. With BlackBerry only recently returning to profitability, this elevated multiple hints that the market is pricing in a powerful earnings recovery rather than paying for today’s modest profit base.

Against the Canadian software industry average of 54.5 times earnings, BlackBerry’s 127.3 times looks aggressively priced, and it also exceeds the peer group’s 73.7 times benchmark. Our estimated fair price-to-earnings ratio of 36.8 times suggests a much lower level the market could eventually gravitate toward if expectations moderate or execution disappoints.

Explore the SWS fair ratio for BlackBerry

Result: Price-to-Earnings of 127.3x (OVERVALUED)

However, investors must still weigh modest 5.4% revenue growth and a history of weak long term returns. These factors could quickly challenge today’s upbeat expectations.

Find out about the key risks to this BlackBerry narrative.

Another View: Our DCF Model Says the Opposite

While earnings multiples make BlackBerry look expensive, our DCF model tells a different story. It suggests the shares are trading about 84% below a fair value of roughly CA$37.41, which implies the market may be heavily discounting BlackBerry’s long term cash flow potential. Which signal deserves more weight?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out BlackBerry for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 911 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own BlackBerry Narrative

If you want to dig into the numbers yourself or challenge these conclusions, you can quickly build a custom view of BlackBerry in just a few minutes: Do it your way.

A great starting point for your BlackBerry research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready for more high conviction ideas?

Do not stop at one opportunity when you can systematically hunt for three. Use the Simply Wall Street Screener to surface data driven candidates across the market.

- Capture potential multibaggers early by scanning these 3572 penny stocks with strong financials that already back their promise with stronger balance sheets and improving fundamentals.

- Ride the next wave of intelligent automation by targeting these 26 AI penny stocks positioned at the crossroads of software, data, and exponential computing power.

- Lock in income while rates shift by focusing on these 15 dividend stocks with yields > 3% that balance attractive yields with sustainable payout ratios and resilient cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if BlackBerry might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:BB

BlackBerry

Provides intelligent security software and services to enterprises and governments worldwide.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

49 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4729.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6410.8% overvalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.8% undervalued

956 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Alphabet ·

GOOGL: AI Platform Expansion And Cloud Demand Will Support Durable Performance Amid Competitive Pressures

Fair Value:US$323.71.9% undervalued

1342 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative