Advertisement

BlackBerry Limited (TSE:BB) Just Reported And Analysts Have Been Cutting Their Estimates

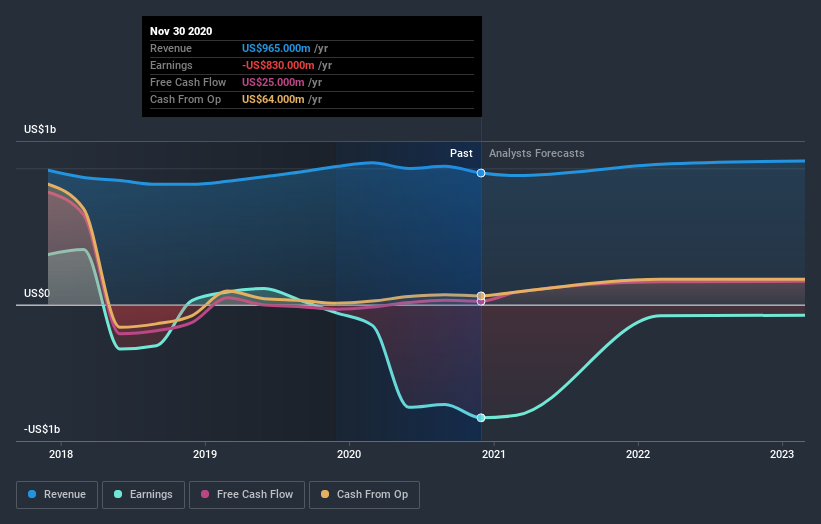

As you might know, BlackBerry Limited (TSE:BB) last week released its latest yearly, and things did not turn out so great for shareholders. Revenues missed expectations somewhat, coming in at US$893m, but statutory earnings fell catastrophically short, with a loss of US$1.97 some 36% larger than what the analysts had predicted. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

See our latest analysis for BlackBerry

After the latest results, the consensus from BlackBerry's five analysts is for revenues of US$795.0m in 2022, which would reflect a definite 11% decline in sales compared to the last year of performance. Losses are predicted to fall substantially, shrinking 79% to US$0.41. Before this latest report, the consensus had been expecting revenues of US$1.04b and US$0.15 per share in losses. So there's been quite a change-up of views after the recent consensus updates, withthe analysts making a serious cut to their revenue outlook while also expecting losses per share to increase.

The analysts lifted their price target 17% to US$5.88, implicitly signalling that lower earnings per share are not expected to have a longer-term impact on the stock's value. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. There are some variant perceptions on BlackBerry, with the most bullish analyst valuing it at US$8.76 and the most bearish at US$4.43 per share. This is a fairly broad spread of estimates, suggesting that analysts are forecasting a wide range of possible outcomes for the business.

Of course, another way to look at these forecasts is to place them into context against the industry itself. We would also point out that the forecast 11% annualised revenue decline to the end of 2022 is better than the historical trend, which saw revenues shrink 15% annually over the past five years Compare this against analyst estimates for companies in the broader industry, which suggest that revenues (in aggregate) are expected to grow 18% annually. So while a broad number of companies are forecast to grow, unfortunately BlackBerry is expected to see its sales affected worse than other companies in the industry.

The Bottom Line

The most important thing to take away is that the analysts increased their loss per share estimates for next year. On the negative side, they also downgraded their revenue estimates, and forecasts imply revenues will perform worse than the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for BlackBerry going out to 2023, and you can see them free on our platform here..

It is also worth noting that we have found 3 warning signs for BlackBerry that you need to take into consideration.

If you’re looking to trade BlackBerry, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if BlackBerry might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSX:BB

BlackBerry

Provides intelligent security software and services to enterprises and governments worldwide.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|40.2% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|62.7% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.1% undervalued

UN

Community Contributor