Advertisement

- Canada

- /

- Specialty Stores

- /

- TSX:DIV

Here's Why We're Wary Of Buying Diversified Royalty's (TSE:DIV) For Its Upcoming Dividend

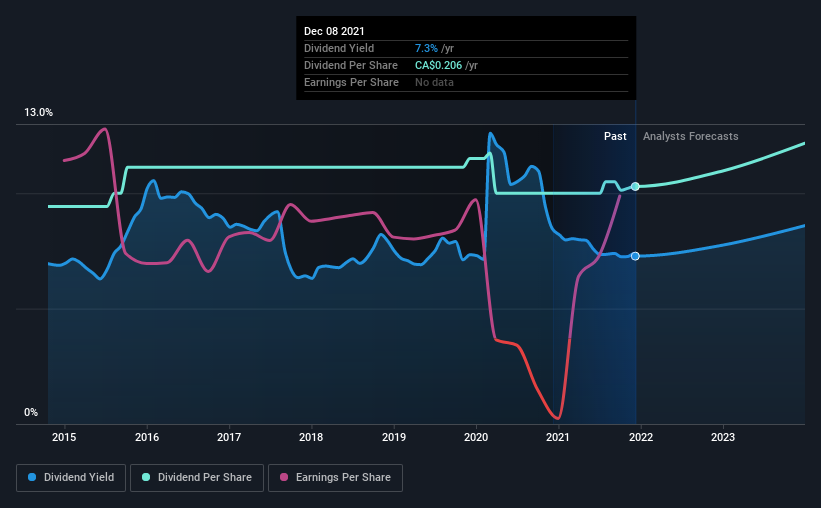

Diversified Royalty Corp. (TSE:DIV) stock is about to trade ex-dividend in four days. Typically, the ex-dividend date is one business day before the record date which is the date on which a company determines the shareholders eligible to receive a dividend. The ex-dividend date is of consequence because whenever a stock is bought or sold, the trade takes at least two business day to settle. This means that investors who purchase Diversified Royalty's shares on or after the 14th of December will not receive the dividend, which will be paid on the 31st of December.

The company's upcoming dividend is CA$0.018 a share, following on from the last 12 months, when the company distributed a total of CA$0.20 per share to shareholders. Based on the last year's worth of payments, Diversified Royalty has a trailing yield of 7.3% on the current stock price of CA$2.83. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. As a result, readers should always check whether Diversified Royalty has been able to grow its dividends, or if the dividend might be cut.

See our latest analysis for Diversified Royalty

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Diversified Royalty paid out 152% of profit in the past year, which we think is typically not sustainable unless there are mitigating characteristics such as unusually strong cash flow or a large cash balance. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. It paid out an unsustainably high 272% of its free cash flow as dividends over the past 12 months, which is worrying. It's pretty hard to pay out more than you earn, so we wonder how Diversified Royalty intends to continue funding this dividend, or if it could be forced to cut the payment.

Cash is slightly more important than profit from a dividend perspective, but given Diversified Royalty's payouts were not well covered by either earnings or cash flow, we would be concerned about the sustainability of this dividend.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If earnings fall far enough, the company could be forced to cut its dividend. For this reason, we're glad to see Diversified Royalty's earnings per share have risen 14% per annum over the last five years. It's great to see earnings per share growing rapidly, but we're disturbed to see the company paid out 152% of its earnings last year. We're wary of fast-growing companies flaming out by over-committing themselves financially, and consider this a yellow flag.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Since the start of our data, seven years ago, Diversified Royalty has lifted its dividend by approximately 1.3% a year on average. Earnings per share have been growing much quicker than dividends, potentially because Diversified Royalty is keeping back more of its profits to grow the business.

To Sum It Up

Has Diversified Royalty got what it takes to maintain its dividend payments? While it's nice to see earnings per share growing, we're curious about how Diversified Royalty intends to continue growing, or maintain the dividend in a downturn given that it's paying out such a high percentage of its earnings and cashflow. It's not the most attractive proposition from a dividend perspective, and we'd probably give this one a miss for now.

Although, if you're still interested in Diversified Royalty and want to know more, you'll find it very useful to know what risks this stock faces. For example, Diversified Royalty has 3 warning signs (and 2 which are a bit concerning) we think you should know about.

If you're in the market for dividend stocks, we recommend checking our list of top dividend stocks with a greater than 2% yield and an upcoming dividend.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:DIV

Diversified Royalty

A multi-royalty corporation, engages in the acquisition of royalties from multi-location businesses and franchisors in North America.

Average dividend payer and fair value.

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4039.0% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6087.9% undervalued

8 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8143.2% undervalued

21 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

NO

Norms70 on Standard Lithium ·

SLI is share to watch next 5 years

Fair Value:€4.57.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15082.3% undervalued

61 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RedhawkCC on Prime Medicine ·

PRME remains a long shot but publication in the New England Journal of Medicine helps.

Fair Value:US$0.0469.1k% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.1% undervalued

962 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

75 followersusers have followed this narrative

7 commentsusers have commented on this narrative

21 likesusers have liked this narrative