Advertisement

- Canada

- /

- Oil and Gas

- /

- TSX:FRU

Canadian Undervalued Small Caps With Insider Activity For October 2024

Simply Wall St

Reviewed by Simply Wall St

In 2024, the Canadian market has mirrored the impressive performance seen globally, with indices like the TSX showing significant gains amid a growing economy and favorable central bank policies. In this environment, small-cap stocks with insider activity can present intriguing opportunities as they may benefit from rising corporate profits and supportive economic conditions.

Top 10 Undervalued Small Caps With Insider Buying In Canada

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Trican Well Service | 6.9x | 0.9x | 22.30% | ★★★★★★ |

| AutoCanada | NA | 0.1x | 39.05% | ★★★★★★ |

| First National Financial | 10.6x | 3.4x | 49.26% | ★★★★★☆ |

| Calfrac Well Services | 2.4x | 0.2x | 20.35% | ★★★★★☆ |

| Nexus Industrial REIT | 3.7x | 3.7x | 17.62% | ★★★★☆☆ |

| Rogers Sugar | 15.3x | 0.6x | 48.36% | ★★★★☆☆ |

| Primaris Real Estate Investment Trust | 13.0x | 3.5x | 44.74% | ★★★★☆☆ |

| Sagicor Financial | 1.3x | 0.3x | -42.26% | ★★★★☆☆ |

| Vermilion Energy | NA | 1.2x | -212.09% | ★★★★☆☆ |

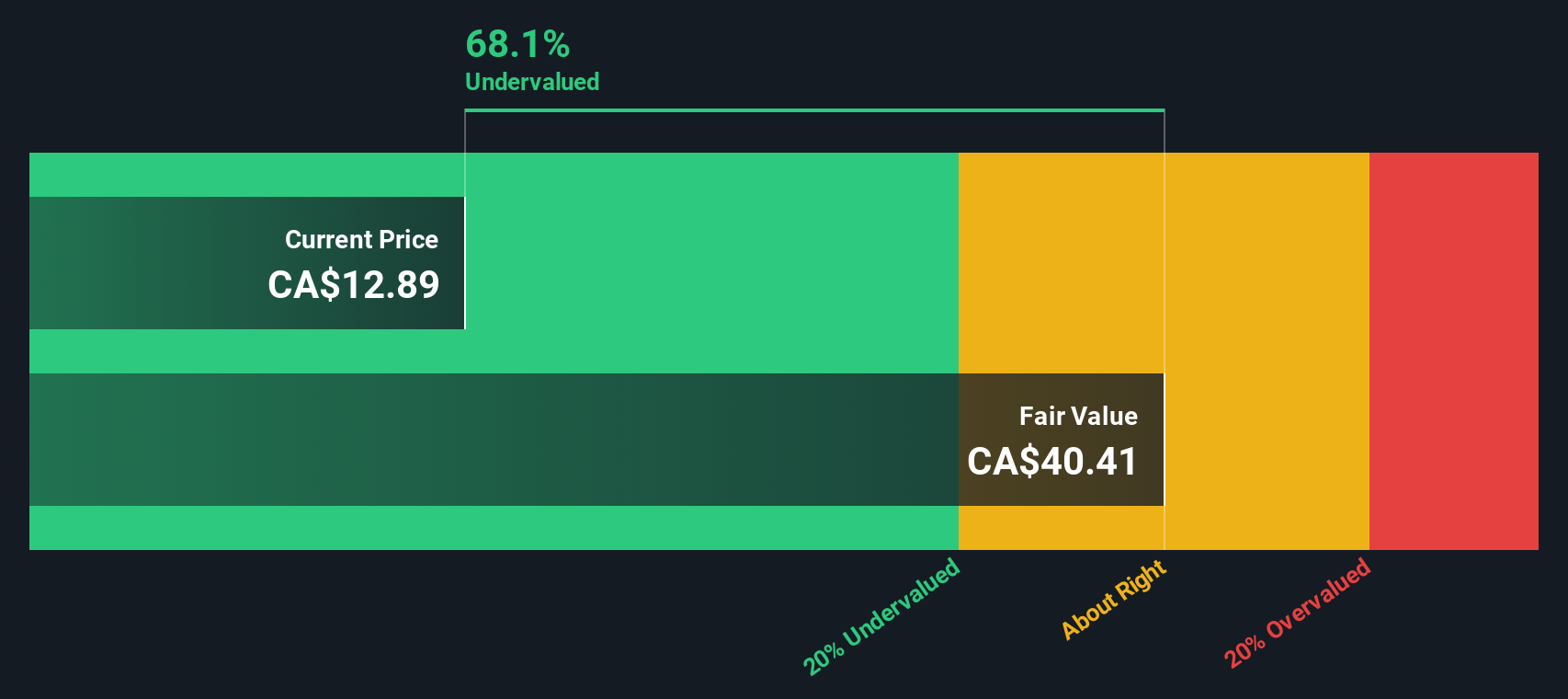

| Freehold Royalties | 14.1x | 6.5x | 49.37% | ★★★★☆☆ |

Let's uncover some gems from our specialized screener.

Freehold Royalties (TSX:FRU)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Freehold Royalties is a Canadian company focused on oil and gas exploration and production, with operations generating CA$323.04 million in revenue.

Operations: The company generates revenue primarily from oil and gas exploration and production, with a recent quarterly revenue of CA$323.04 million. It has seen fluctuations in its net income margin, reaching 46.41% in the latest period. The gross profit margin has shown stability around 96.91%. Operating expenses are a significant portion of costs, including depreciation and amortization expenses which have been notable over time.

PE: 14.1x

Freehold Royalties, a Canadian energy company, showcases insider confidence with recent share purchases. Their financials display solid growth; net income for Q2 2024 reached C$39.3 million, up from C$24.26 million the previous year. The company maintains consistent dividends of C$0.09 per share, affirming stability despite reliance on external borrowing for funding. Presentations at industry conferences highlight their proactive engagement in the energy sector's dynamics, suggesting potential avenues for future growth amidst market challenges.

- Navigate through the intricacies of Freehold Royalties with our comprehensive valuation report here.

Explore historical data to track Freehold Royalties' performance over time in our Past section.

Headwater Exploration (TSX:HWX)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Headwater Exploration is engaged in the exploration, development, and production of petroleum and natural gas with a market capitalization of CA$1.43 billion.

Operations: Headwater Exploration's primary revenue stream is from the exploration, development, and production of petroleum and natural gas, with recent quarterly revenue reaching CA$484.24 million. The company has demonstrated a gross profit margin trend peaking at 81.73% in 2018 before fluctuating to around 76.21% in the latest period. Operating expenses, including general and administrative costs, play a significant role in financial outcomes alongside non-operating expenses such as depreciation and amortization (D&A).

PE: 8.6x

Headwater Exploration, a Canadian energy firm, showcases potential as an undervalued stock. Recent earnings highlight a surge in sales to C$164.28 million for Q2 2024 from C$118.97 million the previous year, alongside increased net income of C$53.87 million from C$30.95 million. Insider confidence is evident with recent share purchases, indicating faith in future growth despite forecasted earnings decline by 10.9% annually over three years due to reliance on external borrowing for funding.

NorthWest Healthcare Properties Real Estate Investment Trust (TSX:NWH.UN)

Simply Wall St Value Rating: ★★★★☆☆

Overview: NorthWest Healthcare Properties Real Estate Investment Trust operates as a real estate investment trust focused on owning and managing healthcare properties, with a market capitalization of approximately CA$2.72 billion.

Operations: NorthWest Healthcare Properties Real Estate Investment Trust generates revenue primarily from the healthcare real estate sector, with a recent revenue figure of CA$523.85 million. The company's cost structure includes a cost of goods sold (COGS) amounting to CA$116.25 million and operating expenses of CA$55.60 million, leading to a gross profit margin of 77.81%. Non-operating expenses have significantly impacted net income, resulting in a negative net income margin over recent periods.

PE: -3.3x

NorthWest Healthcare Properties REIT, a Canadian healthcare-focused real estate investment trust, has been active in extending and renewing leases, notably securing a 10-year renewal at São Paulo's Sabará Hospital. The REIT's recent lease activities have extended its Brazil portfolio's WALE to 18.2 years. Despite reporting net losses of C$122 million for Q2 2024, the company continues to distribute C$0.03 per unit monthly dividends, indicating steady cash flow management amidst leadership transitions with CEO Craig Mitchell retiring mid-2025.

- Dive into the specifics of NorthWest Healthcare Properties Real Estate Investment Trust here with our thorough valuation report.

Learn about NorthWest Healthcare Properties Real Estate Investment Trust's historical performance.

Taking Advantage

- Click here to access our complete index of 25 Undervalued TSX Small Caps With Insider Buying.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:FRU

Freehold Royalties

Acquires and manages royalty interests in the crude oil, natural gas, natural gas liquids, and potash properties in Canada and the United States.

Proven track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.1% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.2% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor