Results: OrganiGram Holdings Inc. Delivered A Surprise Loss And Now Analysts Have New Forecasts

It's been a good week for OrganiGram Holdings Inc. (TSE:OGI) shareholders, because the company has just released its latest full-year results, and the shares gained 3.1% to CA$3.61. Revenues fell 6.3% short of expectations, at CA$80m. Earnings correspondingly dipped, with OrganiGram Holdings reporting a loss of CA$0.068 per share, whereas analysts had previously modelled a profit in this period. Following the result, analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We thought readers would find it interesting to see analysts' latest post-earnings forecasts for next year.

View our latest analysis for OrganiGram Holdings

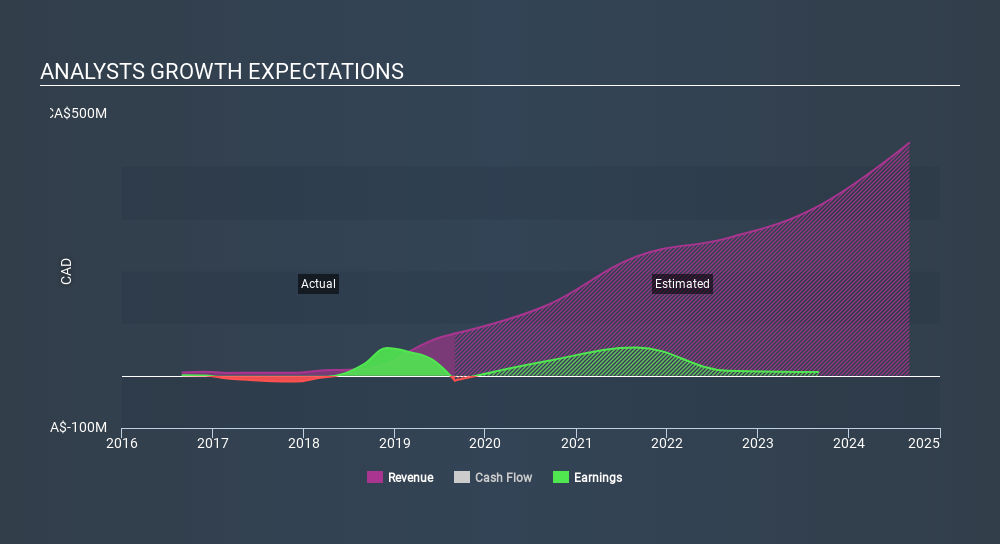

Taking into account the latest results, the latest consensus from OrganiGram Holdings's 15 analysts is for revenues of CA$133.6m in 2020, which would reflect a major 66% improvement in sales compared to the last 12 months. OrganiGram Holdings is also expected to turn profitable, with earnings of CA$0.092 per share. In the lead-up to this report, analysts had been modelling revenues of CA$159.7m and earnings per share (EPS) of CA$0.19 in 2020. It looks like analyst sentiment has declined substantially in the aftermath of these results, with a substantial drop in revenue estimates and a large cut to consensus earnings per share numbers as well.

The consensus price target fell 8.9% to CA$7.63, with the weaker earnings outlook clearly leading analyst valuation estimates. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. There are some variant perceptions on OrganiGram Holdings, with the most bullish analyst valuing it at CA$13.30 and the most bearish at CA$3.75 per share. We would probably assign less value to the analyst forecasts in this situation, because such a wide range of estimates could imply that the future of this business is difficult to value accurately. As a result it might not be possible to derive much meaning from the consensus price target, which is after all just an average of this wide range of estimates.

It can also be useful to step back and take a broader view of how analyst forecasts compare to OrganiGram Holdings's performance in recent years. We can infer from the latest estimates that analysts are expecting a continuation of OrganiGram Holdings's historical trends, as next year's forecast 66% revenue growth is roughly in line with 78% annual revenue growth over the past five years. Compare this with the wider market, which analyst estimates (in aggregate) suggest will see revenues grow 54% next year. It's clear that while OrganiGram Holdings's revenue growth is expected to continue on its current trajectory, it's only expected to grow in line with the market itself.

The Bottom Line

The most important thing to take away is that analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Analysts also downgraded their revenue estimates, although as we saw earlier, forecast growth is only expected to be about the same as the wider market. The consensus price target fell measurably, with analysts seemingly not reassured by the latest results, leading to a lower estimate of OrganiGram Holdings's future valuation.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple OrganiGram Holdings analysts - going out to 2024, and you can see them free on our platform here.

You can also view our analysis of OrganiGram Holdings's balance sheet, and whether we think OrganiGram Holdings is carrying too much debt, for free on our platform here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About TSX:OGI

Organigram Holdings

Engages in the production and sale of cannabis and cannabis-derived products in Canada.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Community Narratives