Advertisement

- Canada

- /

- Metals and Mining

- /

- TSX:VZLA

Valuing Vizsla Silver (TSX:VZLA) After Panuco Feasibility Win, New Financing and Silver’s Recent Strength

Simply Wall St

Reviewed by Simply Wall St

Vizsla Silver (TSX:VZLA) just checked several big boxes at once by combining positive feasibility results at its Panuco project with a sizeable convertible notes financing, all against a rising silver price backdrop.

See our latest analysis for Vizsla Silver.

The upbeat feasibility study and fresh convertible notes financing have landed just as silver gained momentum, helping drive a 28.25% 1 month share price return and a powerful 169.53% year to date share price rally. The 3 year total shareholder return of 363.09% suggests longer term momentum has been building rather than fading.

If this kind of move in Vizsla has caught your eye, it could be worth scanning other precious metals names and discovering fast growing stocks with high insider ownership.

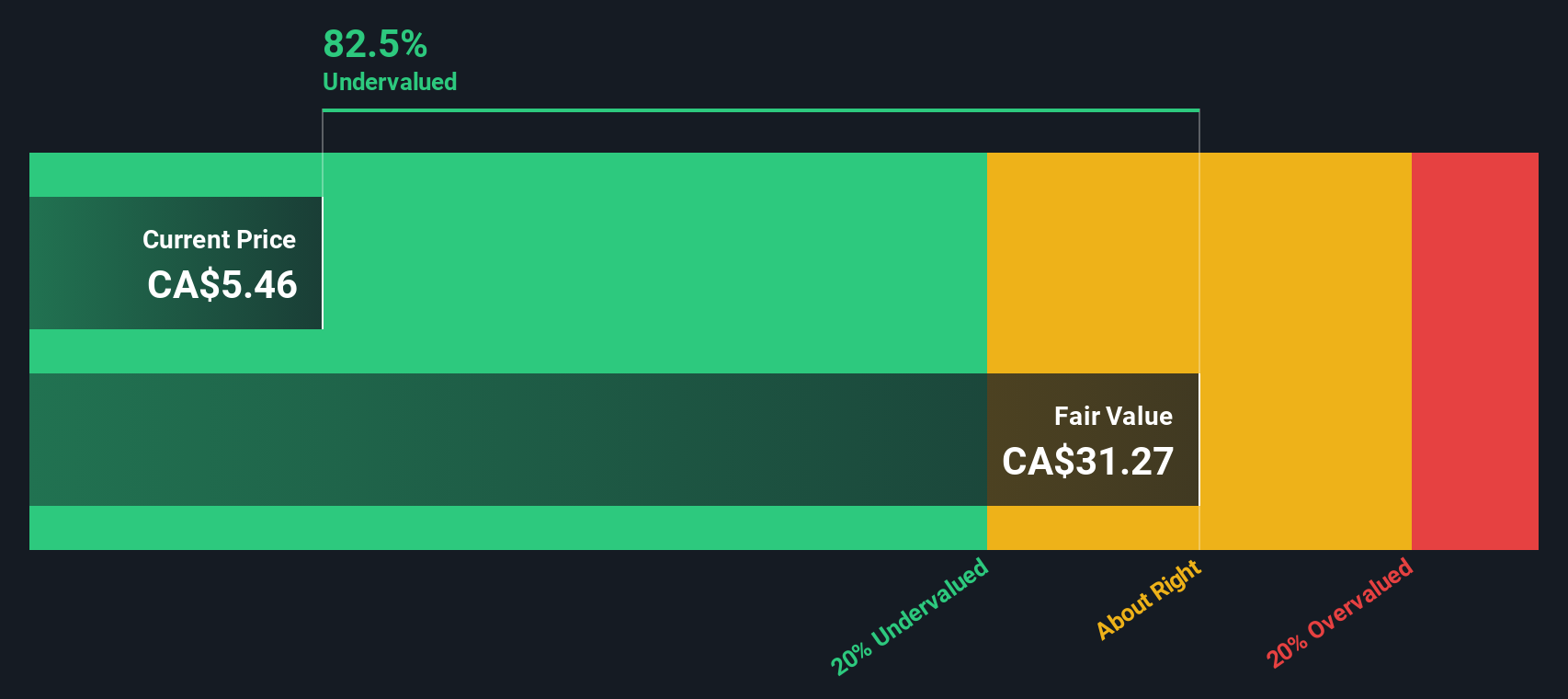

Despite the surge, Vizsla still trades at a discount to analyst targets and has yet to generate revenue, raising a key question for investors: is this a mispriced growth story, or has the market already baked in future upside?

Price-to-Book of 3.9x: Is it justified?

Vizsla Silver trades on a price-to-book ratio of 3.9 times, which screens as expensive versus the broader Canadian metals and mining space but more modest relative to its closest peers.

The price-to-book ratio compares the company’s market value with the net assets on its balance sheet, a common yardstick for pre revenue or early stage resource developers where earnings are not yet a reliable guide. For Vizsla, investors are effectively paying a premium over the industry average for each dollar of book value, implying that the market is assigning extra value to its Panuco project and future growth potential.

Against the Canadian metals and mining industry average of 2.7 times book value, Vizsla’s 3.9 times multiple looks punchy, suggesting optimism about future cash flows that are not yet visible in current financials. However, compared with a peer group trading around 5.3 times book, Vizsla looks relatively restrained, hinting that some of the upside implied by analyst targets and our fair value estimate may not yet be fully reflected in the share price.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-book of 3.9x (ABOUT RIGHT)

However, financing risk and execution challenges at Panuco, combined with ongoing losses and zero current revenue, could quickly test today’s optimistic valuation.

Find out about the key risks to this Vizsla Silver narrative.

Another View on Value

While 3.9 times book feels fair against peers, our DCF model paints a far more aggressive picture, flagging Vizsla as trading about 72% below its CA$24.87 fair value estimate. Is the market underestimating Panuco’s long term cash generation, or is the model too optimistic?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Vizsla Silver for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 907 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Vizsla Silver Narrative

If you see things differently or want to dig into the numbers yourself, you can build a personalized view in just minutes: Do it your way.

A great starting point for your Vizsla Silver research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, give yourself an edge by scanning a few high potential stock ideas that most investors are ignoring but could transform your returns.

- Capture early stage growth potential with these 3571 penny stocks with strong financials that already show strong underlying financials instead of just hope and hype.

- Target tomorrow’s innovators by reviewing these 26 AI penny stocks that are building real products around artificial intelligence, not just riding the buzzwords.

- Strengthen your income stream by focusing on these 15 dividend stocks with yields > 3% that combine solid yields with businesses designed to keep paying through market cycles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:VZLA

Vizsla Silver

Engages in the acquisition, exploration, and development of mineral resource properties in Canada and Mexico.

Excellent balance sheet and good value.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

43 followersusers have followed this narrative

6 commentsusers have commented on this narrative

15 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

SC

scm on Text ·

TXT will see revenue grow 26% with a profit margin boost of almost 40%

Fair Value:zł8049.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

955 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.6% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative