Nutrien (TSX:NTR) is navigating a dynamic environment marked by both opportunities and challenges. Recent highlights include a robust financial performance with a 17% growth in retail adjusted EBITDA, juxtaposed against a challenging operating environment in Brazil and a decrease in potash segment EBITDA. In the discussion that follows, we will delve into Nutrien's core advantages, critical issues, growth strategies, and external threats to provide a comprehensive overview of the company's current business situation.

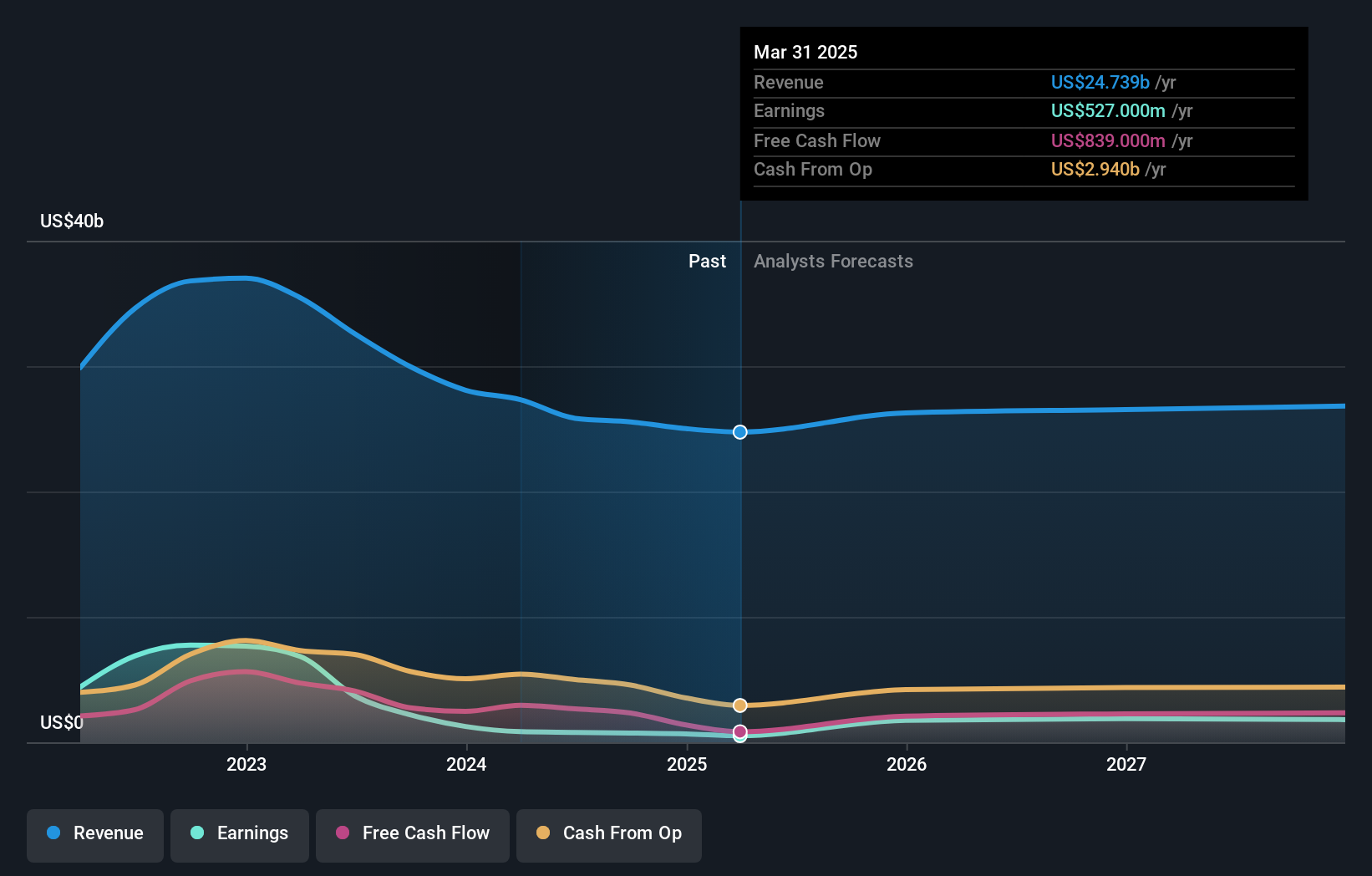

TSX:NTR Earnings and Revenue Growth as at Sep 2024

Advertisement

Strengths: Core Advantages Driving Sustained Success For Nutrien

Nutrien has demonstrated robust financial performance, with adjusted EBITDA reaching $3.3 billion in the first half of 2024, driven by increased crop input margins and strong global potash demand. The company has also achieved significant production efficiency, lowering its controllable cash cost of production to $53 per tonne. Nutrien's retail segment has shown impressive growth, with retail adjusted EBITDA totaling $1.2 billion, up 17% from the prior year. The strategic focus on enhancing earnings quality and cash flow, as articulated by CEO Ken Seitz, underscores the company's commitment to serving growers in core markets. Additionally, Nutrien is currently trading 38.4% below its estimated fair value of CA$105.46, indicating it may be undervalued compared to its peers.

Weaknesses: Critical Issues Affecting Nutrien's Performance and Areas For Growth

Despite its strengths, Nutrien faces several challenges. The operating environment in Brazil remains difficult, impacting the company's overall performance. Potash segment EBITDA decreased to $1 billion in the first half of 2024 due to lower benchmark prices. Additionally, the full-year adjusted EBITDA guidance for the retail segment was lowered to $1.5 billion to $1.7 billion, primarily due to a moderate recovery in Brazilian retail earnings. The company also incurred losses on foreign currency derivatives in Brazil. Nutrien's Price-To-Earnings Ratio (30x) is higher than the North American Chemicals industry average (27x), suggesting it is expensive compared to its industry peers.

Opportunities: Potential Strategies for Leveraging Growth and Competitive Advantage

Nutrien has several opportunities to enhance its market position. The expected increase in Brazilian soybean area by 1% to 3% and projected fertilizer demand of approximately 46 million tonnes in 2024 present significant growth prospects. The company's investment in mine automation projects in potash and low-cost brownfield expansions in nitrogen is likely to boost operational efficiency. Nutrien is also targeting a more than 10% annual growth rate in proprietary products gross margin, which could enhance profitability. Strong customer engagement on summer fill programs in the third quarter indicates a positive outlook for future sales.

Threats: Key Risks and Challenges That Could Impact Nutrien's Success

Nutrien faces several external threats that could impact its growth. The shift to generic crop protection products and commodity fertilizers has led to longer in-country inventory clearance times, increasing competitive pressures. Softening agricultural commodity prices have affected grower sentiment, potentially impacting future sales. Regulatory and operational risks, particularly in Brazil, have posed challenges, including issues related to segregation of duties and governance controls. Additionally, weather-related disruptions, such as wet weather in May, have impacted application schedules and shifted demand into the third quarter.

Conclusion

Nutrien's strong financial performance, driven by increased crop input margins and efficient production, positions the company well for sustained success. However, challenges in the Brazilian market and a higher-than-average Price-To-Earnings Ratio indicate potential areas for improvement. Opportunities such as the anticipated growth in Brazilian soybean acreage and investments in mine automation could further enhance profitability. Despite external threats like competitive pressures and regulatory risks, Nutrien's current trading price, which is 38.4% below its estimated fair value of CA$105.46, suggests a favorable outlook for future performance, with a target price less than 20% higher than the current share price.

Key Takeaways

Shareholder in Nutrien? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Valuation is complex, but we're here to simplify it.

Discover if Nutrien might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.