Advertisement

- Canada

- /

- Specialty Stores

- /

- TSX:KITS

TSX Growth Companies With High Insider Ownership For March 2025

Simply Wall St

Reviewed by Simply Wall St

As the Canadian market navigates a period of economic adjustment, with inflationary pressures easing and interest rates poised for potential cuts by the Bank of Canada, investors are keenly observing opportunities that align with these shifting dynamics. In this context, growth companies with high insider ownership present an intriguing prospect, as they often demonstrate strong alignment between management and shareholder interests—an appealing attribute amid evolving market conditions.

Top 10 Growth Companies With High Insider Ownership In Canada

| Name | Insider Ownership | Earnings Growth |

| Propel Holdings (TSX:PRL) | 36.5% | 35.8% |

| Robex Resources (TSXV:RBX) | 25.6% | 141.5% |

| Allied Gold (TSX:AAUC) | 17.7% | 85.1% |

| West Red Lake Gold Mines (TSXV:WRLG) | 13.5% | 76.8% |

| Vox Royalty (TSX:VOXR) | 12% | 83.3% |

| NTG Clarity Networks (TSXV:NCI) | 38.2% | 27.6% |

| goeasy (TSX:GSY) | 21.6% | 15.4% |

| Aritzia (TSX:ATZ) | 17.6% | 41.1% |

| Enterprise Group (TSX:E) | 32.2% | 26% |

| Burcon NutraScience (TSX:BU) | 16.4% | 152.2% |

Let's take a closer look at a couple of our picks from the screened companies.

Ivanhoe Mines (TSX:IVN)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Ivanhoe Mines Ltd., along with its subsidiaries, is involved in the mining, development, and exploration of minerals and precious metals in Africa, with a market capitalization of CA$20.22 billion.

Operations: The company's revenue segment includes Kipushi Properties, which generated $40.82 million.

Insider Ownership: 12.4%

Ivanhoe Mines is positioned for significant growth, with earnings projected to increase at a rate of 35.5% annually, outpacing the Canadian market. The company's revenue is expected to grow by 40.3% per year, driven by robust production updates from its Kamoa-Kakula Copper Complex and Kipushi zinc mine in the DRC. Recent executive changes enhance leadership capabilities, while strategic initiatives like Project 95 aim to boost copper production efficiency and capacity further solidifying its growth trajectory.

- Click to explore a detailed breakdown of our findings in Ivanhoe Mines' earnings growth report.

- Our expertly prepared valuation report Ivanhoe Mines implies its share price may be lower than expected.

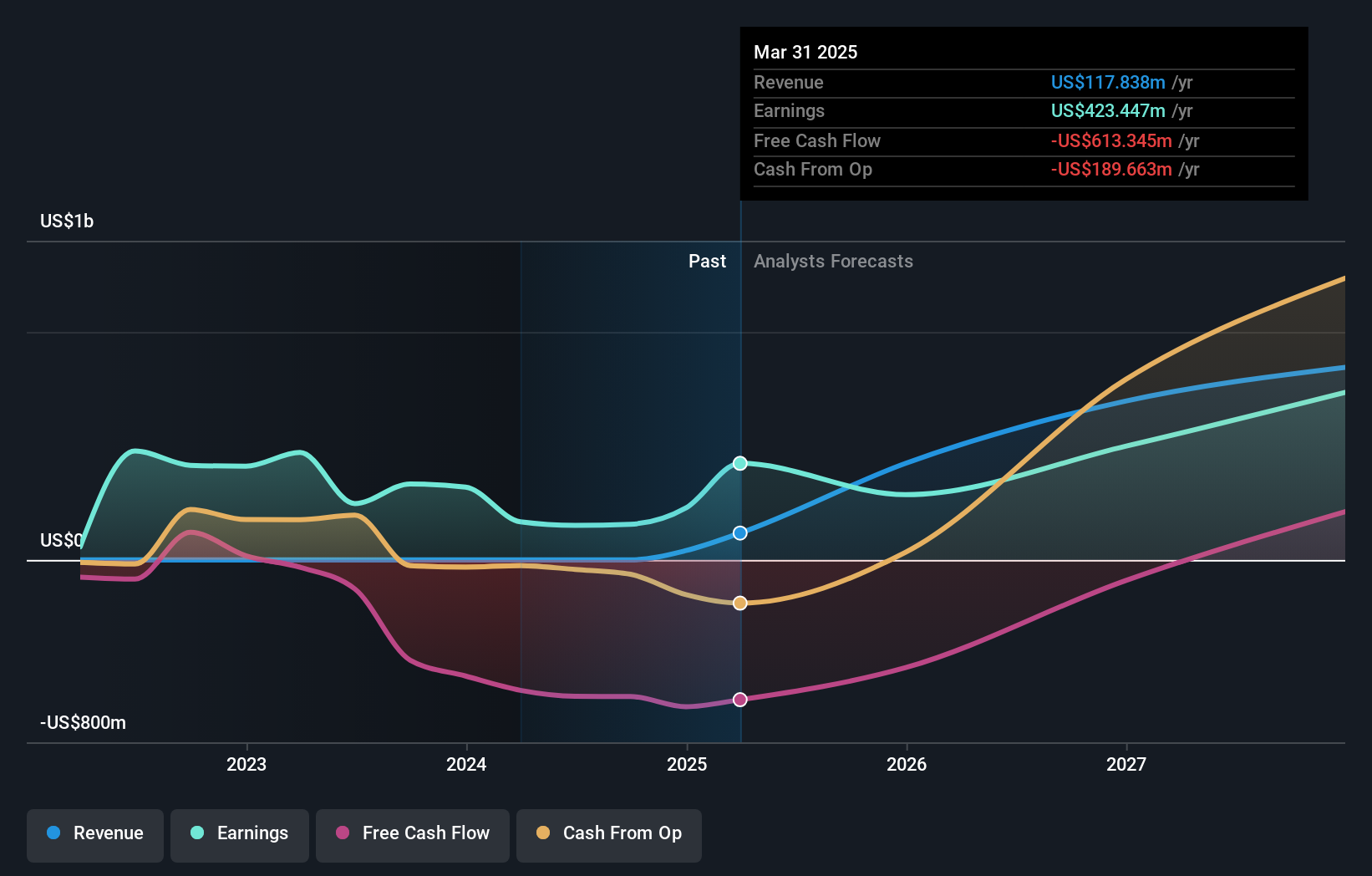

Kits Eyecare (TSX:KITS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Kits Eyecare Ltd. operates a digital eyecare platform in the United States and Canada, with a market cap of CA$374.19 million.

Operations: The company generates revenue primarily through the sale of eyewear products, amounting to CA$159.34 million.

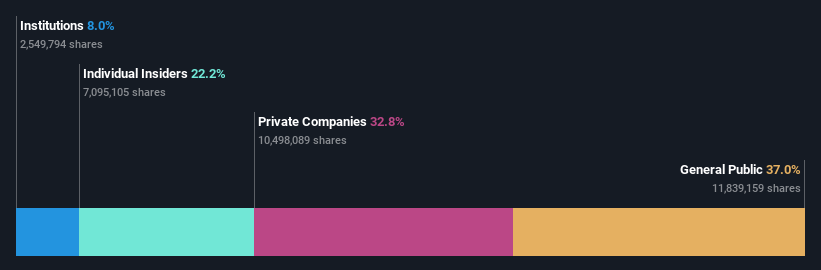

Insider Ownership: 22.2%

Kits Eyecare is poised for growth with earnings expected to rise significantly, outpacing the Canadian market. While trading below fair value and analyst price targets, it faces low insider buying activity. Recent product innovations include a streamlined U.S. vision insurance process, enhancing customer experience and potentially driving revenue growth beyond the forecasted 17.6% annually. The company reported CAD 159.34 million in sales for 2024, marking profitability with CAD 3.12 million net income compared to a prior loss.

- Unlock comprehensive insights into our analysis of Kits Eyecare stock in this growth report.

- Our valuation report here indicates Kits Eyecare may be undervalued.

Vitalhub (TSX:VHI)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Vitalhub Corp. develops technology solutions for health and human service providers across multiple regions, including Canada, the US, the UK, Australia, and Western Asia, with a market cap of CA$485.63 million.

Operations: The company's revenue primarily comes from its healthcare software segment, which generated CA$61.61 million.

Insider Ownership: 14.6%

Vitalhub's earnings are projected to grow significantly at 71.4% annually, surpassing the Canadian market's 15%. Despite recent shareholder dilution from a CAD 30 million equity offering, it trades at a substantial discount to fair value and below analyst price targets, suggesting potential upside. Revenue growth is expected at 19.1% annually, outpacing the broader market but below the high-growth threshold of 20%. No recent insider trading activity was reported.

- Get an in-depth perspective on Vitalhub's performance by reading our analyst estimates report here.

- In light of our recent valuation report, it seems possible that Vitalhub is trading behind its estimated value.

Where To Now?

- Gain an insight into the universe of 35 Fast Growing TSX Companies With High Insider Ownership by clicking here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Kits Eyecare might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:KITS

Kits Eyecare

Operates a digital eyecare platform in the United States and Canada.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor