Advertisement

- Canada

- /

- Metals and Mining

- /

- TSX:EDR

Assessing Endeavour Silver (TSX:EDR)’s Valuation After Its $300 Million Convertible Bond Raise

Simply Wall St

Reviewed by Simply Wall St

Endeavour Silver (TSX:EDR) just locked in a $300 million convertible bond raise, a financing move that reshapes its balance sheet while steering fresh capital toward the long horizon of the Pitarrilla project in Mexico.

See our latest analysis for Endeavour Silver.

That bond deal landed after a huge run, with Endeavour Silver posting a roughly 52% 3 month share price return and around 125% year to date share price return, alongside a powerful 3 year total shareholder return near 177%. All of this suggests that momentum is firmly building.

If this kind of funding move has you thinking about where else growth stories might emerge, it could be worth exploring fast growing stocks with high insider ownership.

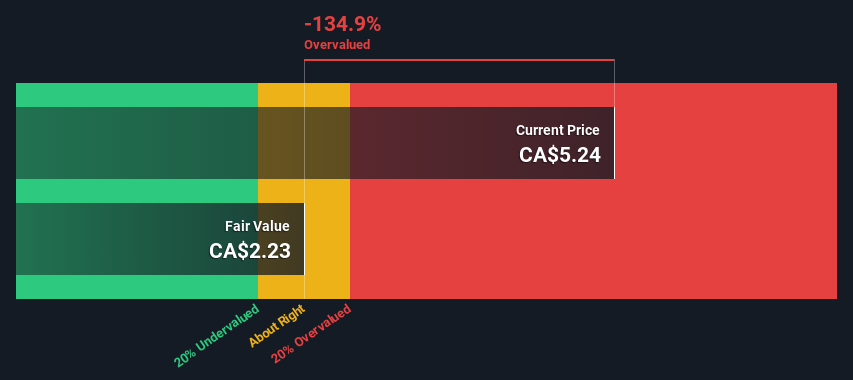

But after that kind of surge and a fresh CA$300 million war chest, is Endeavour Silver still trading at a discount to its intrinsic value, or has the market already priced in the next leg of growth?

Most Popular Narrative Narrative: 14.6% Undervalued

With Endeavour Silver last closing at CA$12.92 against a fair value estimate of $15.13, the most followed narrative points to meaningful upside from here.

The analysts have a consensus price target of CA$9.167 for Endeavour Silver based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$10.0, and the most bearish reporting a price target of just CA$7.5.

Curious how a loss making miner gets a premium future multiple and a higher fair value than the street target? The narrative leans on explosive revenue growth, a sharp swing into healthy margins and a valuation profile more often seen in fast growing cyclicals. Want to see which future earnings power and discount rate assumptions make that math work?

Result: Fair Value of $15.13 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent commissioning issues at Terronera, or delays and cost overruns at Kolpa and Pitarrilla, could quickly undermine those bullish earnings and valuation assumptions.

Find out about the key risks to this Endeavour Silver narrative.

Another Lens On Value

Our DCF model is far less generous than the bullish narrative, suggesting Endeavour Silver is trading well above its estimated fair value today, not below it. If cash flows disappoint or projects slip, could the share price have more downside risk than recent momentum implies?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Endeavour Silver for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 925 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Endeavour Silver Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a custom view in just minutes: Do it your way.

A great starting point for your Endeavour Silver research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If you stop with just one company, you risk missing out on stronger opportunities the Simply Wall Street Screener uncovers across sectors, themes, and strategies.

- Capture early momentum by reviewing these 3576 penny stocks with strong financials that pair tiny share prices with surprisingly resilient fundamentals and room for meaningful upside.

- Position your portfolio for the next productivity boom by scanning these 24 AI penny stocks built around real-world artificial intelligence applications rather than hype.

- Lock in value opportunities by targeting these 925 undervalued stocks based on cash flows where current prices sit meaningfully below estimated cash flow potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Endeavour Silver might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:EDR

Endeavour Silver

A silver mining company, engages in the acquisition, exploration, development, extraction, processing, refining, and reclamation of mineral properties in Mexico, Chile, Peru, and the United States.

Exceptional growth potential with very low risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

18 followersusers have followed this narrative

5 commentsusers have commented on this narrative

5 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1919.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5200.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Applied Digital ·

Staggered by dilution; positions for growth

Fair Value:US$35.4520.9% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.5% undervalued

949 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.1% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative