The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Ascot Resources Ltd. (TSE:AOT) does carry debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Ascot Resources

How Much Debt Does Ascot Resources Carry?

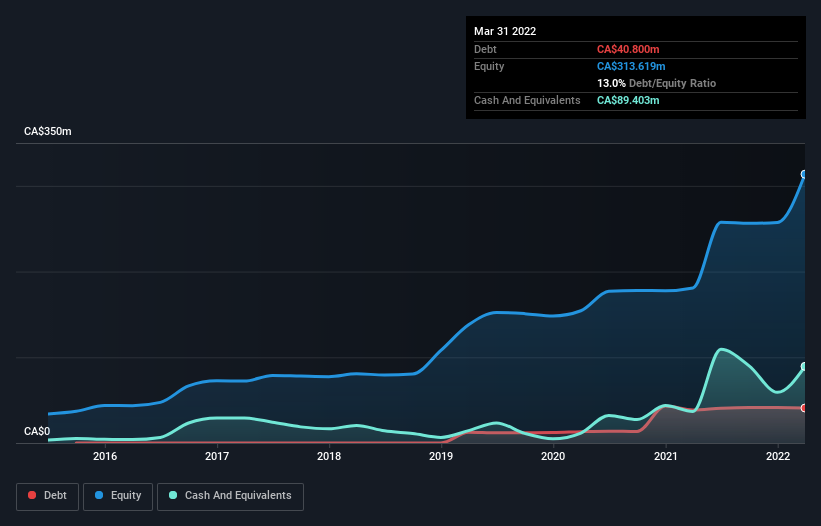

As you can see below, at the end of March 2022, Ascot Resources had CA$40.8m of debt, up from CA$38.6m a year ago. Click the image for more detail. However, its balance sheet shows it holds CA$89.4m in cash, so it actually has CA$48.6m net cash.

A Look At Ascot Resources' Liabilities

According to the last reported balance sheet, Ascot Resources had liabilities of CA$17.9m due within 12 months, and liabilities of CA$63.5m due beyond 12 months. Offsetting these obligations, it had cash of CA$89.4m as well as receivables valued at CA$1.32m due within 12 months. So it actually has CA$9.30m more liquid assets than total liabilities.

This short term liquidity is a sign that Ascot Resources could probably pay off its debt with ease, as its balance sheet is far from stretched. Simply put, the fact that Ascot Resources has more cash than debt is arguably a good indication that it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Ascot Resources's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Given its lack of meaningful operating revenue, investors are probably hoping that Ascot Resources finds some valuable resources, before it runs out of money.

So How Risky Is Ascot Resources?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And in the last year Ascot Resources had an earnings before interest and tax (EBIT) loss, truth be told. And over the same period it saw negative free cash outflow of CA$89m and booked a CA$7.0m accounting loss. With only CA$48.6m on the balance sheet, it would appear that its going to need to raise capital again soon. Even though its balance sheet seems sufficiently liquid, debt always makes us a little nervous if a company doesn't produce free cash flow regularly. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Be aware that Ascot Resources is showing 4 warning signs in our investment analysis , and 2 of those can't be ignored...

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:AOT

Ascot Resources

Engages in the exploration, evaluation, and development of mineral properties in the United States and Canada.

High growth potential and fair value.