Advertisement

- Canada

- /

- Medical Equipment

- /

- TSXV:EVMT

Here's Why We're Not Too Worried About Salona Global Medical Device's (CVE:SGMD) Cash Burn Situation

We can readily understand why investors are attracted to unprofitable companies. Indeed, Salona Global Medical Device (CVE:SGMD) stock is up 541% in the last year, providing strong gains for shareholders. Nonetheless, only a fool would ignore the risk that a loss making company burns through its cash too quickly.

So notwithstanding the buoyant share price, we think it's well worth asking whether Salona Global Medical Device's cash burn is too risky. For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. First, we'll determine its cash runway by comparing its cash burn with its cash reserves.

See our latest analysis for Salona Global Medical Device

How Long Is Salona Global Medical Device's Cash Runway?

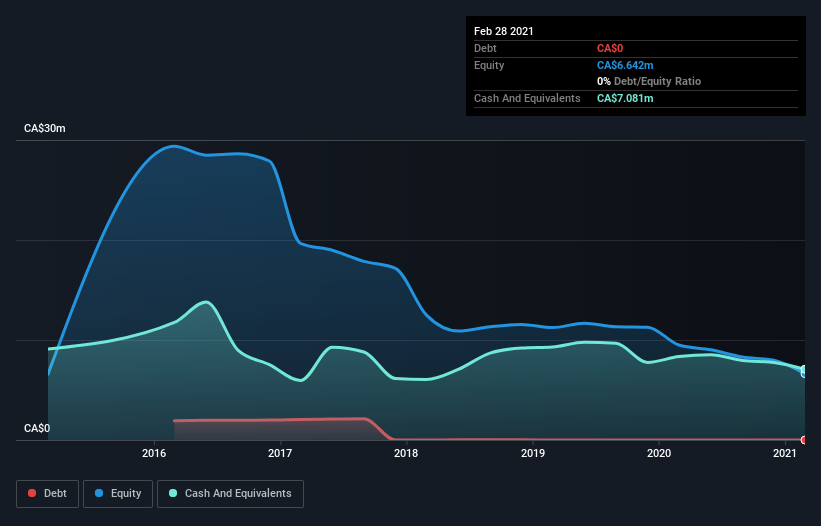

A company's cash runway is calculated by dividing its cash hoard by its cash burn. As at February 2021, Salona Global Medical Device had cash of CA$7.1m and no debt. Looking at the last year, the company burnt through CA$975k. That means it had a cash runway of about 7.3 years as of February 2021. Even though this is but one measure of the company's cash burn, the thought of such a long cash runway warms our bellies in a comforting way. The image below shows how its cash balance has been changing over the last few years.

How Is Salona Global Medical Device's Cash Burn Changing Over Time?

In our view, Salona Global Medical Device doesn't yet produce significant amounts of operating revenue, since it reported just CA$50k in the last twelve months. As a result, we think it's a bit early to focus on the revenue growth, so we'll limit ourselves to looking at how the cash burn is changing over time. Its cash burn positively exploded in the last year, up 393%. We certainly hope for shareholders' sake that the money is well spent, because that kind of expenditure increase always makes us nervous. Admittedly, we're a bit cautious of Salona Global Medical Device due to its lack of significant operating revenues. So we'd generally prefer stocks from this list of stocks that have analysts forecasting growth.

How Hard Would It Be For Salona Global Medical Device To Raise More Cash For Growth?

While Salona Global Medical Device does have a solid cash runway, its cash burn trajectory may have some shareholders thinking ahead to when the company may need to raise more cash. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. Many companies end up issuing new shares to fund future growth. By looking at a company's cash burn relative to its market capitalisation, we gain insight on how much shareholders would be diluted if the company needed to raise enough cash to cover another year's cash burn.

Salona Global Medical Device has a market capitalisation of CA$45m and burnt through CA$975k last year, which is 2.2% of the company's market value. So it could almost certainly just borrow a little to fund another year's growth, or else easily raise the cash by issuing a few shares.

Is Salona Global Medical Device's Cash Burn A Worry?

It may already be apparent to you that we're relatively comfortable with the way Salona Global Medical Device is burning through its cash. In particular, we think its cash runway stands out as evidence that the company is well on top of its spending. While we must concede that its increasing cash burn is a bit worrying, the other factors mentioned in this article provide great comfort when it comes to the cash burn. After taking into account the various metrics mentioned in this report, we're pretty comfortable with how the company is spending its cash, as it seems on track to meet its needs over the medium term. Taking a deeper dive, we've spotted 3 warning signs for Salona Global Medical Device you should be aware of, and 1 of them doesn't sit too well with us.

Of course Salona Global Medical Device may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Evome Medical Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSXV:EVMT

Evome Medical Technologies

Develops, manufactures, and distributes medical devices and products in the Americas and internationally.

Good value slight.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor