Advertisement

- China

- /

- Electronic Equipment and Components

- /

- SHSE:603186

High Growth Tech And 2 Other Stocks With Promising Expansion

Simply Wall St

Reviewed by Simply Wall St

In the current market landscape, major U.S. stock indexes have shown mixed results, with the S&P 500 and Nasdaq reaching record highs while small-cap stocks like those in the Russell 2000 saw a decline after a period of outperformance. Amid these dynamics, growth stocks have notably outpaced value stocks, particularly in sectors such as consumer discretionary and information technology, which are crucial for investors seeking opportunities in high-growth tech companies. In evaluating promising expansion opportunities within this sector, it is important to consider factors such as innovation potential and adaptability to evolving market conditions.

Top 10 High Growth Tech Companies

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| Material Group | 20.45% | 24.01% | ★★★★★★ |

| Seojin SystemLtd | 35.41% | 39.86% | ★★★★★★ |

| Yggdrazil Group | 30.20% | 87.10% | ★★★★★★ |

| eWeLLLtd | 27.24% | 28.74% | ★★★★★★ |

| Mental Health TechnologiesLtd | 24.68% | 97.53% | ★★★★★★ |

| Medley | 25.57% | 31.67% | ★★★★★★ |

| CD Projekt | 24.93% | 27.00% | ★★★★★★ |

| Fine M-TecLTD | 36.52% | 131.08% | ★★★★★★ |

| Elliptic Laboratories | 70.09% | 111.37% | ★★★★★★ |

| JNTC | 29.48% | 104.37% | ★★★★★★ |

Click here to see the full list of 1292 stocks from our High Growth Tech and AI Stocks screener.

Here's a peek at a few of the choices from the screener.

NOTE (OM:NOTE)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: NOTE AB (publ) is a company that offers electronics manufacturing services across Sweden, Finland, the United Kingdom, Bulgaria, Estonia, China, and other international markets with a market capitalization of approximately SEK3.94 billion.

Operations: NOTE AB (publ) generates revenue primarily from electronics manufacturing services, with significant contributions from Western Europe (SEK3.02 billion) and the Rest of the World (SEK988.44 million).

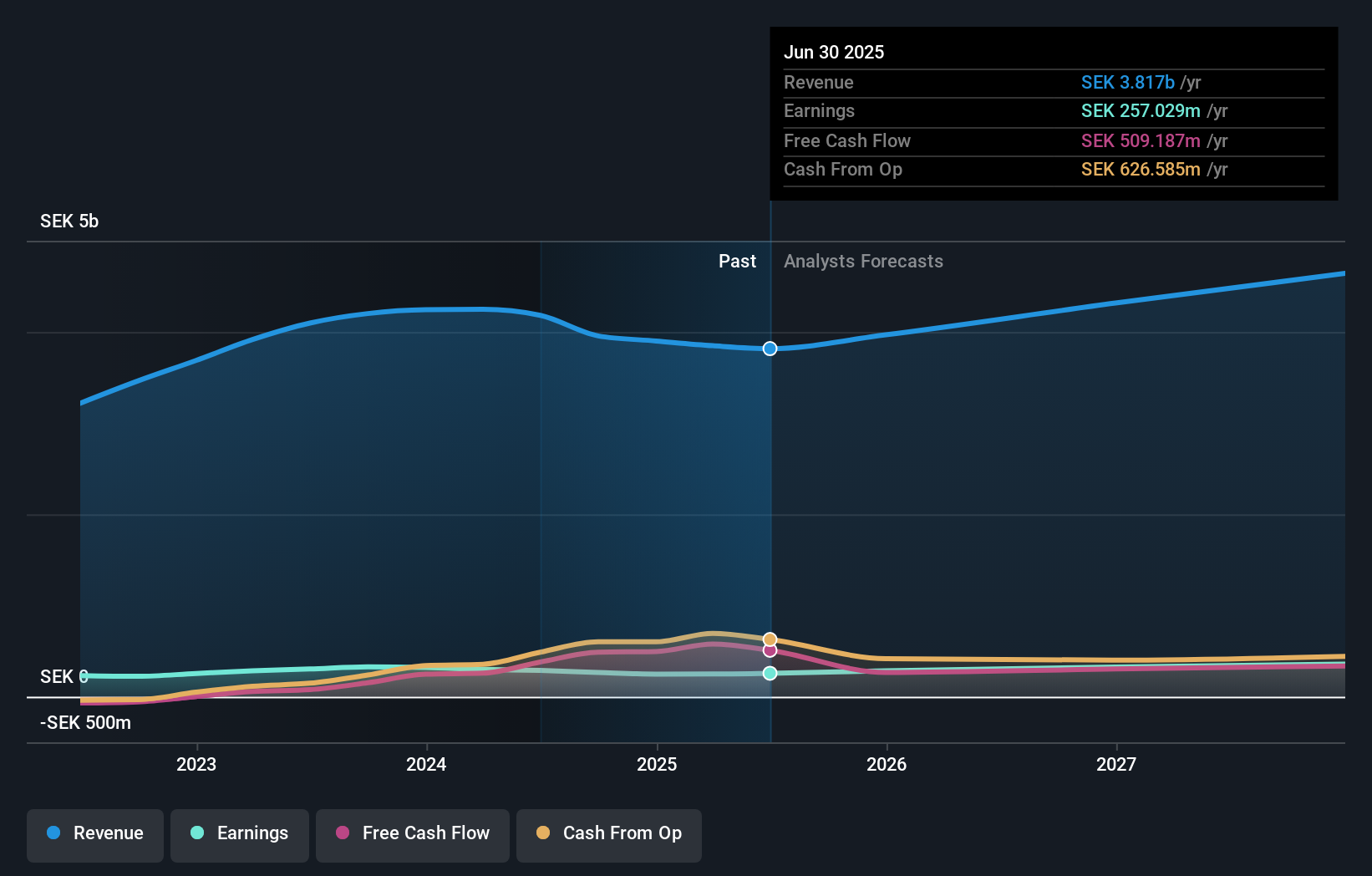

NOTE AB, amidst a challenging fiscal environment as evidenced by a decline in quarterly sales to SEK 809 million from SEK 1,034 million year-over-year and net income dropping to SEK 43 million from SEK 65 million, still positions itself for potential growth with forecasted annual revenue and earnings increases of 11.6% and 20.0%, respectively. This projected growth outpaces the broader Swedish market's expected gains significantly. The company's commitment to innovation is underscored by its strategic allocation towards R&D expenses, ensuring it remains competitive within the tech sector despite recent setbacks in financial performance. As it navigates through these fiscal challenges, NOTE’s ability to sustain investment in development could be crucial for leveraging emerging technological trends and enhancing its market position.

- Take a closer look at NOTE's potential here in our health report.

Understand NOTE's track record by examining our Past report.

Zhejiang Wazam New MaterialsLTD (SHSE:603186)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Zhejiang Wazam New Materials Co., LTD. specializes in the design, development, production, and sale of copper clad laminates, adhesive sheets, composite materials, and membrane materials with a market capitalization of CN¥3.98 billion.

Operations: Zhejiang Wazam New Materials Co., LTD. focuses on producing and selling copper clad laminates, adhesive sheets, composite materials, and membrane materials. The company operates with a market capitalization of CN¥3.98 billion.

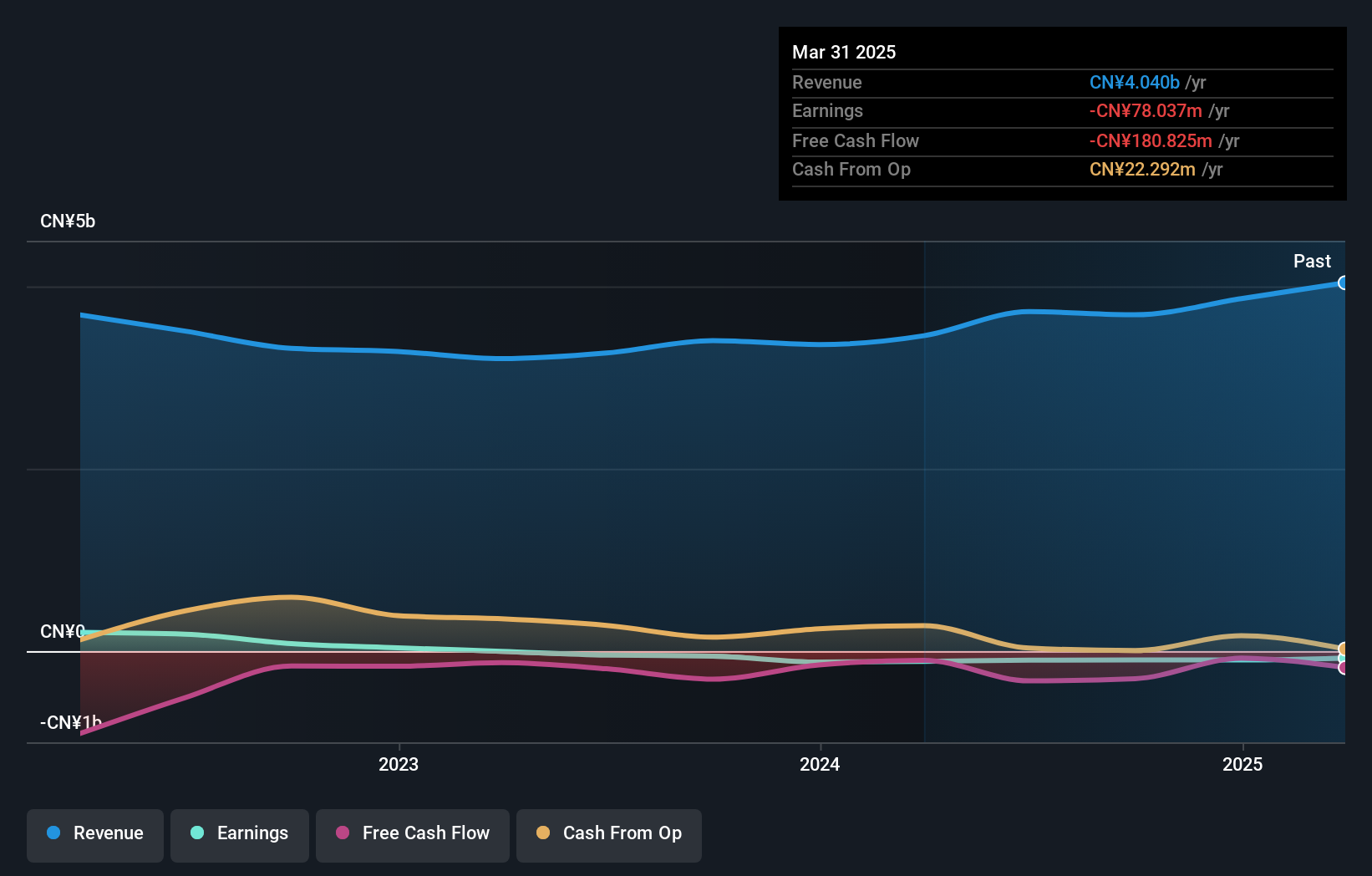

Zhejiang Wazam New Materials Co., LTD. has demonstrated resilience and potential in a challenging market, with its recent earnings report showing a significant reduction in net loss to CNY 6.65 million from CNY 30.52 million year-over-year, alongside an increase in sales to CNY 2,823.75 million from CNY 2,497.17 million. This financial recovery is underpinned by robust revenue growth expectations of 25.9% annually, outpacing the broader Chinese market's forecast of 13.7%. Moreover, the company's strategic focus on R&D investments is set to propel future innovations and competitiveness within the high-tech materials sector; these expenditures are crucial as they navigate through fiscal challenges while aiming for profitability with projected earnings growth of an impressive 188%.

Vitalhub (TSX:VHI)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Vitalhub Corp. develops technology solutions for health and human service providers across various countries, including Canada, the United States, the United Kingdom, Australia, and Western Asia, with a market cap of CA$586.66 million.

Operations: Vitalhub Corp. generates revenue primarily from its healthcare software segment, which amounts to CA$61.61 million. The company operates across multiple international markets, focusing on technology solutions for health and human service providers.

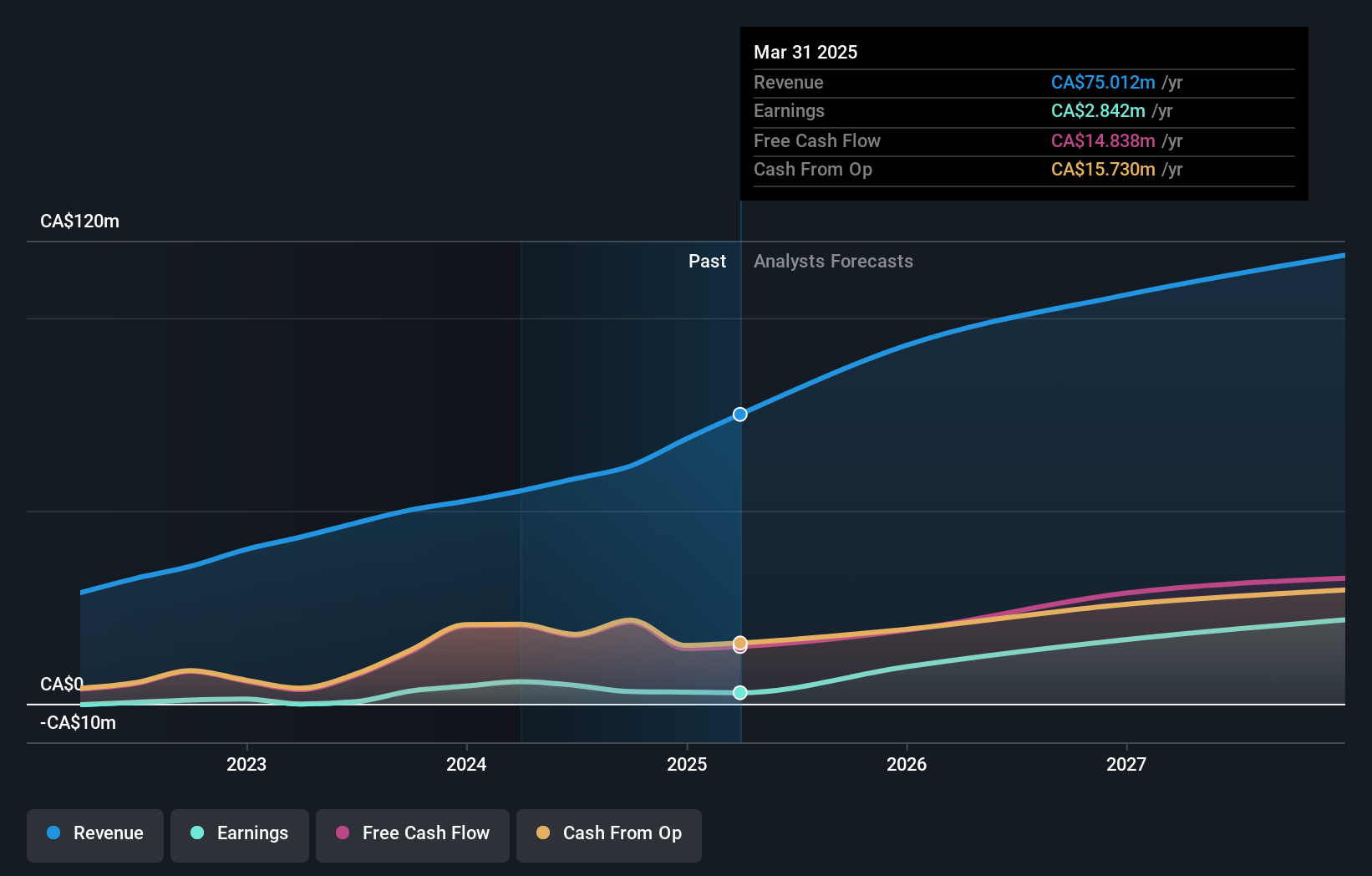

Vitalhub stands out in the tech landscape with a projected revenue growth of 19.8% annually, surpassing the Canadian market's average of 7.6%. This growth is underpinned by strategic expansions like their recent credit facility increase to $65 million and robust client implementations such as the SHREWD platform for Winnipeg Regional Health Authority. Furthermore, despite a challenging past with a one-off loss of CA$3.8M, Vitalhub's focus on innovative healthcare solutions forecasts an impressive earnings surge by 111.9% annually, showcasing its potential resilience and adaptability in the evolving tech sector.

- Delve into the full analysis health report here for a deeper understanding of Vitalhub.

Assess Vitalhub's past performance with our detailed historical performance reports.

Turning Ideas Into Actions

- Click through to start exploring the rest of the 1289 High Growth Tech and AI Stocks now.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Wazam New MaterialsLTD might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:603186

Zhejiang Wazam New MaterialsLTD

Engages in the research, development, design, production, and sale of copper clad plates, composite materials, and membrane materials.

Slightly overvalued very low.

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|59.1% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|17.5% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|2.4% undervalued

RO

Community Contributor