- Canada

- /

- Metals and Mining

- /

- TSX:MND

Exploring 3 Undiscovered Gems in Canada's Stock Market

Reviewed by Simply Wall St

As Canada navigates a shifting political landscape and economic uncertainties, the stock market reflects these dynamics with increased volatility and opportunities for diversification. In this environment, identifying promising small-cap stocks can be particularly rewarding, as they often offer unique growth potential amidst broader market fluctuations.

Top 10 Undiscovered Gems With Strong Fundamentals In Canada

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Reconnaissance Energy Africa | NA | 9.16% | 15.11% | ★★★★★★ |

| Minsud Resources | NA | nan | -29.01% | ★★★★★★ |

| Amerigo Resources | 14.04% | 7.04% | 11.73% | ★★★★★☆ |

| Maxim Power | 25.01% | 12.79% | 17.14% | ★★★★★☆ |

| Mako Mining | 10.21% | 38.44% | 58.78% | ★★★★★☆ |

| Grown Rogue International | 24.92% | 19.37% | 188.55% | ★★★★★☆ |

| Corby Spirit and Wine | 65.79% | 7.46% | -5.76% | ★★★★☆☆ |

| Petrus Resources | 19.44% | 17.20% | 46.03% | ★★★★☆☆ |

| Genesis Land Development | 47.40% | 28.61% | 52.30% | ★★★★☆☆ |

| DIRTT Environmental Solutions | 58.73% | -5.34% | -5.43% | ★★★★☆☆ |

Let's review some notable picks from our screened stocks.

Medical Facilities (TSX:DR)

Simply Wall St Value Rating: ★★★★★☆

Overview: Medical Facilities Corporation, with a market cap of CA$365.62 million, owns and operates specialty hospitals and ambulatory surgery centers in the United States through its subsidiaries.

Operations: The company generates revenue primarily from its healthcare facilities and services, amounting to $441.27 million.

Medical Facilities, a smaller player in the healthcare sector, has shown impressive earnings growth of 265.2% over the past year, significantly outpacing the industry average of 11.8%. The company's debt to equity ratio has improved from 105.7% to a more manageable 48.9% over five years, signaling better financial health. Recent results highlighted a net income of US$7.25 million for Q3 compared to a net loss last year, with basic earnings per share rising from US$0.01 to US$0.3 year-over-year. Additionally, Medical Facilities is trading at about 90% below its estimated fair value and remains free cash flow positive despite substantial insider selling recently observed.

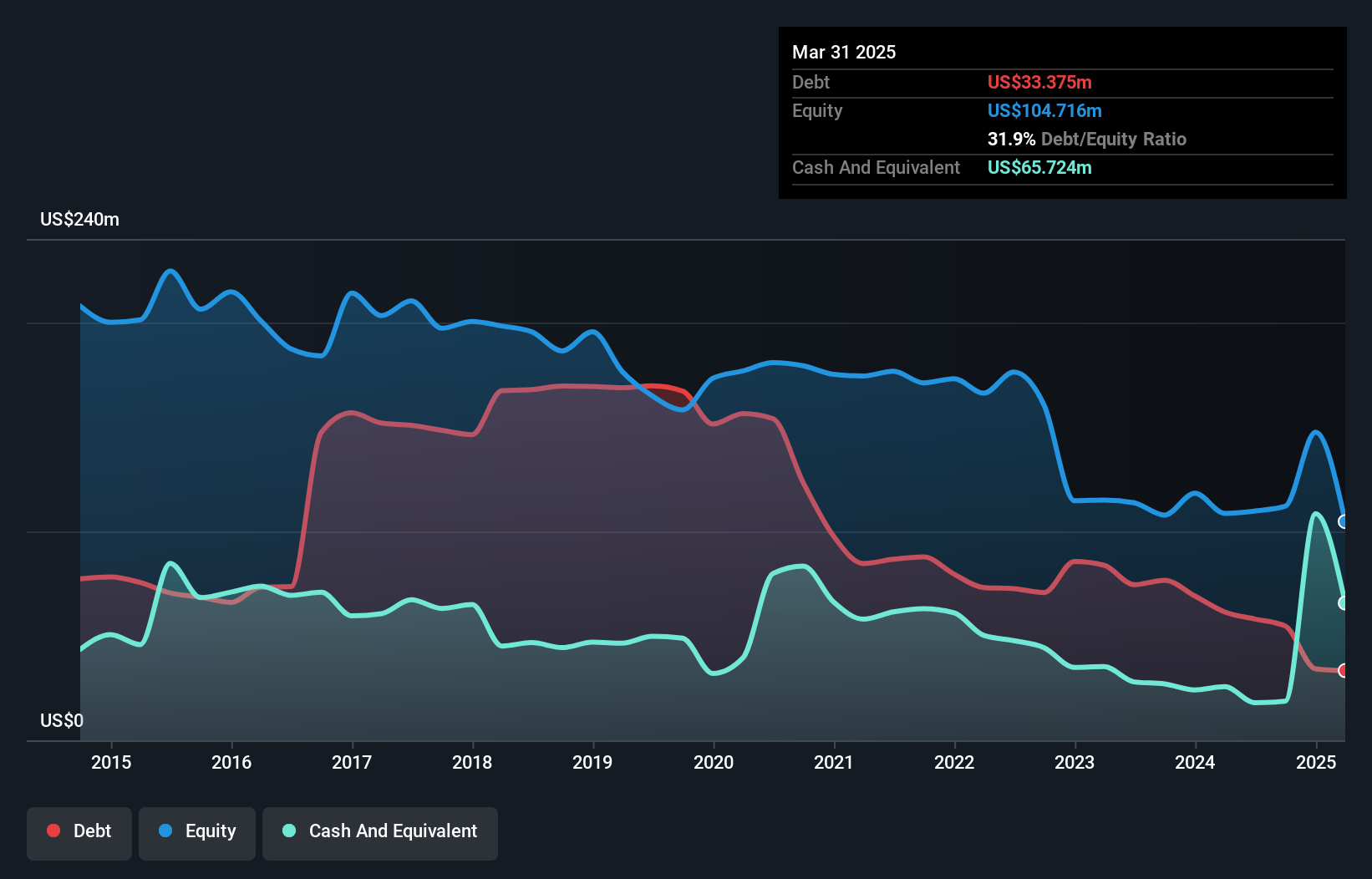

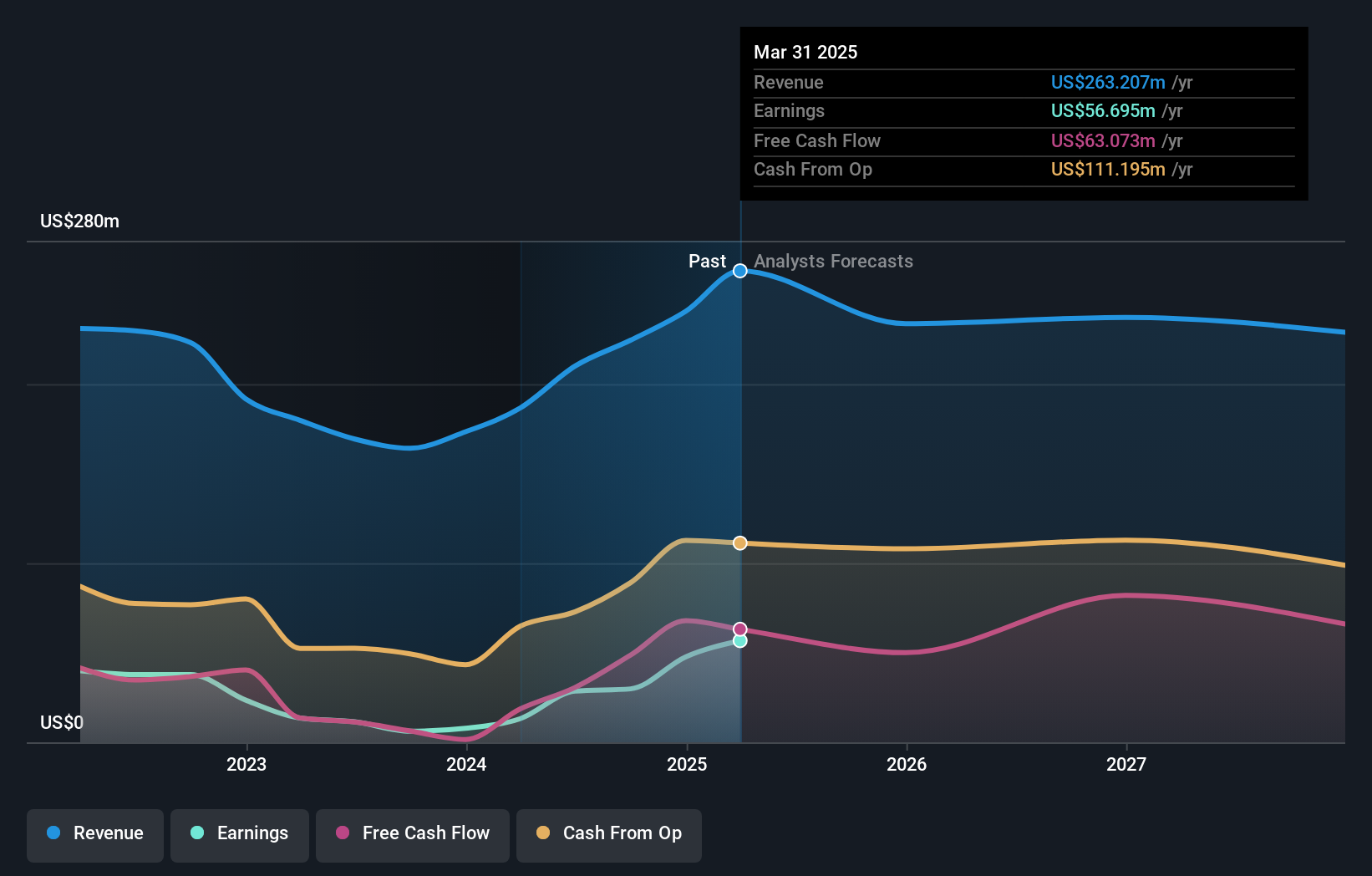

Mandalay Resources (TSX:MND)

Simply Wall St Value Rating: ★★★★★★

Overview: Mandalay Resources Corporation is involved in the acquisition, exploration, extraction, processing, and reclamation of mineral properties across Canada, Australia, Sweden, and Chile with a market cap of CA$397.24 million.

Operations: Mandalay Resources generates revenue primarily from its Metals & Mining segment, focusing on gold and other precious metals, with reported revenues of $224.44 million. The company's financial performance can be analyzed through its net profit margin trends over recent periods.

Mandalay Resources, with its promising exploration updates at the Björkdal operation, has shown impressive growth. The company reported a net income of US$27.1 million for the first nine months of 2024, a significant increase from US$5.15 million in the prior year period. Earnings per share rose to US$0.29 from US$0.06, demonstrating robust performance amidst industry challenges. With earnings growing by 381% over the past year and trading at 54% below estimated fair value, Mandalay is positioned attractively compared to peers. Additionally, their debt-to-equity ratio improved significantly from 56% to just 2%.

- Click here to discover the nuances of Mandalay Resources with our detailed analytical health report.

Assess Mandalay Resources' past performance with our detailed historical performance reports.

TWC Enterprises (TSX:TWC)

Simply Wall St Value Rating: ★★★★★★

Overview: TWC Enterprises Limited owns, operates, and manages golf clubs under the ClubLink One Membership More Golf brand in Canada and the United States, with a market cap of approximately CA$433.72 million.

Operations: TWC Enterprises generates revenue primarily from its Canadian Golf Club Operations, contributing CA$153.38 million, and US Golf Club Operations at CA$23.76 million.

TWC Enterprises seems to be a promising player in the hospitality sector, with earnings growth of 127.9% over the past year, outpacing the industry average of 1.8%. The company's debt-to-equity ratio has significantly improved from 31.5% to 6.2% in five years, showcasing strong financial management. Despite a one-off gain of CA$33.9 million impacting recent results, TWC trades at an attractive valuation—88.2% below its estimated fair value—suggesting potential for investors seeking undervalued opportunities. Recent share repurchases totaling CA$3.52 million indicate strategic capital allocation and confidence in future prospects within this small-cap space.

- Delve into the full analysis health report here for a deeper understanding of TWC Enterprises.

Evaluate TWC Enterprises' historical performance by accessing our past performance report.

Turning Ideas Into Actions

- Take a closer look at our TSX Undiscovered Gems With Strong Fundamentals list of 47 companies by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:MND

Mandalay Resources

Engages in the acquisition, exploration, extraction, processing, and reclamation of mineral properties in Canada, Australia, Sweden, and Chile.

Flawless balance sheet and undervalued.

Market Insights

Community Narratives