Advertisement

Flow Beverage Corp. (TSE:FLOW) Just Released Its Second-Quarter Results And Analysts Are Updating Their Estimates

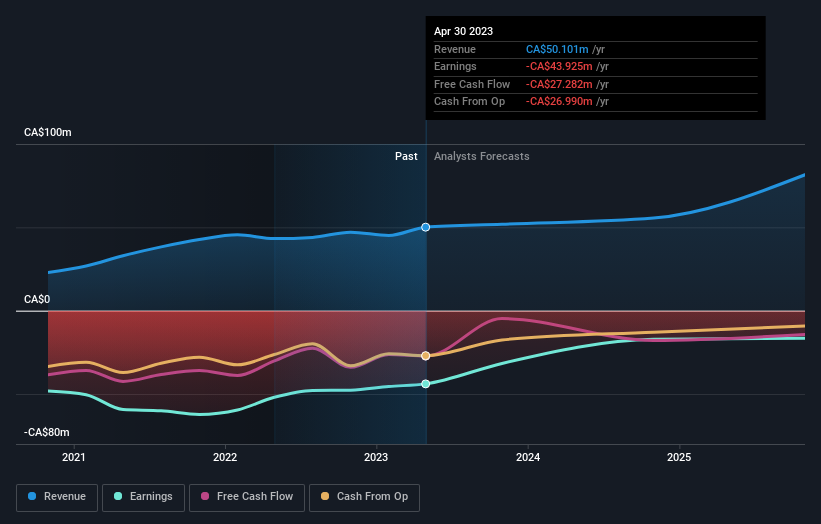

There's been a notable change in appetite for Flow Beverage Corp. (TSE:FLOW) shares in the week since its second-quarter report, with the stock down 13% to CA$0.48. Revenues of CA$14m crushed expectations, although expenses increased commensurately, with statutory losses hitting CA$0.18 per share, -20% above what the analysts expected. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

Check out our latest analysis for Flow Beverage

After the latest results, the three analysts covering Flow Beverage are now predicting revenues of CA$51.9m in 2023. If met, this would reflect a satisfactory 3.5% improvement in revenue compared to the last 12 months. The loss per share is expected to greatly reduce in the near future, narrowing 25% to CA$0.59. Before this earnings announcement, the analysts had been modelling revenues of CA$46.8m and losses of CA$0.53 per share in 2023. So there's been quite a change-up of views after the recent consensus updates, with the analysts significantly increasing their revenue forecasts while also expecting losses per share to increase. It looks like the top line growth will not be achieved without incremental costs.

There was no major change to the consensus price target of CA$2.08, with growing revenues seemingly enough to offset the concern of growing losses. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values Flow Beverage at CA$2.50 per share, while the most bearish prices it at CA$1.25. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We would highlight that Flow Beverage's revenue growth is expected to slow, with the forecast 7.2% annualised growth rate until the end of 2023 being well below the historical 16% growth over the last year. Compare this to the 14 other companies in this industry with analyst coverage, which are forecast to grow their revenue at 5.8% per year. Factoring in the forecast slowdown in growth, it looks like Flow Beverage is forecast to grow at about the same rate as the wider industry.

The Bottom Line

The most important thing to take away is that the analysts increased their loss per share estimates for next year. There was also an upgrade to revenue estimates, although as we saw earlier, forecast growth is only expected to be about the same as the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At Simply Wall St, we have a full range of analyst estimates for Flow Beverage going out to 2025, and you can see them free on our platform here..

Plus, you should also learn about the 5 warning signs we've spotted with Flow Beverage (including 1 which is concerning) .

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:FLOW

Flow Beverage

Engages in the developing, marketing, selling, and distributing natural alkaline spring water-based beverages under the Flow brand name in Canada and the United States.The company’s spring water available in organic and natural flavours, such as blackberry+hibiscus, strawberry+rose, cucumber+mint, watermelon, grapefruit, cucumber, peach+blueberry, blood orange, meyer lemon, strawberry+kiwi, ginger+lemon, and pomegranate, as well as vitamin-infused water comprising elderberry, citrus, and cherry.

Slightly overvalued with imperfect balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor